A new cost shock is underway, signaling a fourth inflation wave since 2020. Oil volatility is back, suppliers are already moving, and consumer price tolerance is gone. Most CPG manufacturers are hesitating – and hesitation is, in 2026, the biggest margin risk. Here is what speed, discipline, and operating model readiness look like in practice.

The fourth inflation wave has started forming, and most CPG companies are not ready for it.

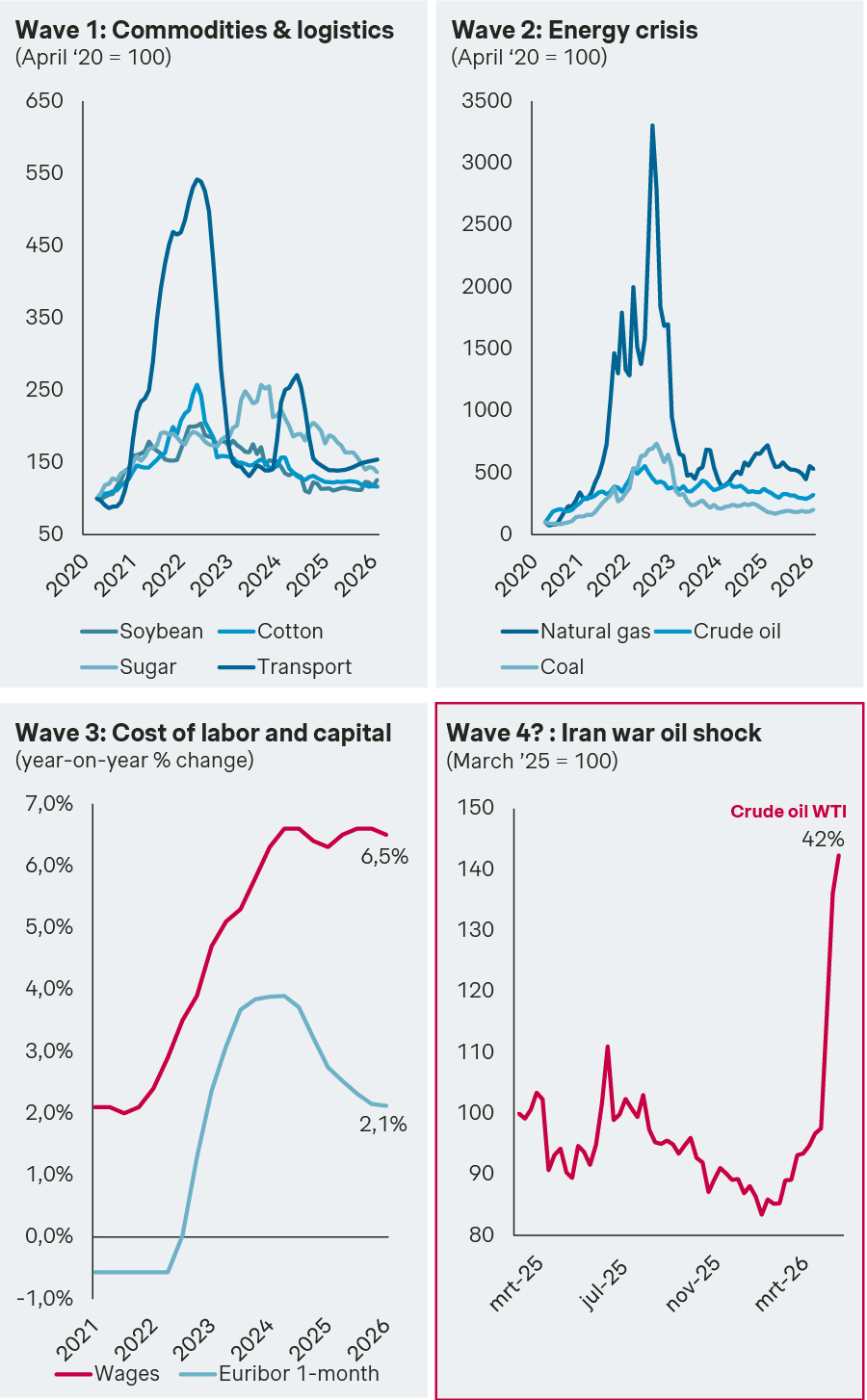

Since 2020, the consumer goods industry has absorbed three successive inflation shocks. Each followed a familiar pattern: suppliers moved first, manufacturers hesitated, retailers resisted, and consumers eventually absorbed. And each time, the companies that waited for clarity lost margin to the companies that moved early.

A fourth inflation wave is forming now, and the backdrop has shifted fast:

- Oil volatility is back: WTI crude has swung between $86 and $113 per barrel in April alone.

- Annual inflation scenarios are live: Financial institutions project a rate of inflation of 7% if the Iran conflict continues, 5% in the better scenario.

- Suppliers are already moving: Raw material companies and selected manufacturers are communicating price increases of 5 to 10 percent – some higher.

Iran war oil shock might ignite the next inflation wave

And the situation downstream? Most end-market CPG manufacturers are hesitating, hoping the pressure proves temporary. This is the most dangerous posture available. Not because the storm will necessarily break. But because hesitation itself, in a volatile cost environment, is how margin disappears.

The strategic arc: where are we in 2026?

The last three years have followed a clear narrative for CPG leadership teams:

- 2023 was about protecting the topline: Revenue stayed up through pricing catch-up; 2022's margin damage was still being absorbed.

- 2024 was about fixing the margin: Companies caught up on pricing realization and repaired what the 2022 shock had eroded.

- 2025 was about optimizing the model: “Fit for Growth” became the dominant agenda. Surveys showed positive revenue and profit outlooks. Stock prices broke records.

Then the environment turned. Tariff turbulence. Geopolitical uncertainty. And now, weeks into an active Middle East crisis, the fourth inflation wave is forming.

2026 is the year the resistance gets tested again: This time in an inflation cycle shaped by geopolitics, not the usual business cycle challenges of a normal planning year. The question is whether the capability built in 2025 is actually ready for volatility or whether the sustainable growth model has produced beautiful dashboards and no decision speed.

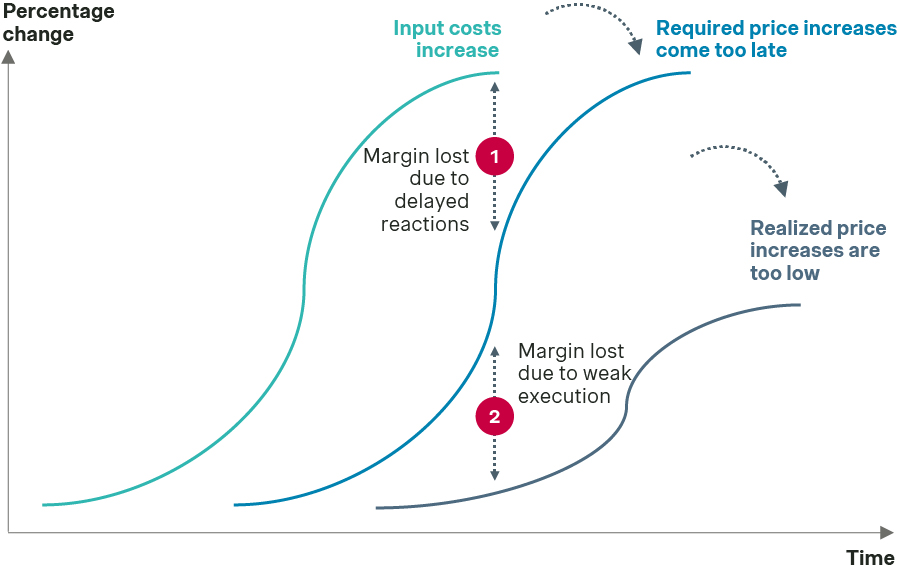

The pattern from previous inflation cycles: too late, too little

The lesson from 2022 was not “inflation is bad.” It was more specific: companies fail in inflation cycles for two compounding reasons. They react too late – waiting for full cost visibility, for competitors to move first. Then they pass through too little – realized increases below what costs justify.

The Fortune 500 numbers from the last cycle tell the story plainly: 2022 vs. 2021 saw revenue up 10.9% but margin down 5.95%: Showcasing the cost shock and pricing lag. The margin damage took nearly two full years to repair. And the customer relationships damaged by the corrective price increases in 2023 are still being managed today.

The growth window – the gap between first hit and peak – is where most value is lost or won. And it is narrower than it looks from the outside.

Why this cycle is structurally harder than 2022

The playbook from 2022 is not enough for 2026. Three structural shifts have made the operating environment meaningfully harder.

Consumer pricing tolerance is gone: 57% of consumers report increasing price sensitivity since early 2025. 59% say they would shift further toward private label if prices rise again. The consumer’s willingness to absorb another round – which carried CPG companies through 2022 – has evaporated.

Private label has moved upmarket: 41% of consumers now frequently buy higher-quality private label, not just entry-level substitutes. Pricing power is under pressure across every segment. Premium positioning no longer protects you from trade-down.

Buying groups have consolidated: International buying groups covered roughly 50% of European FMCG sales in 2022. Today they cover 90%. Country-by-country pricing logic is no longer defensible – differentials must be justified structurally or they will be harmonized down.

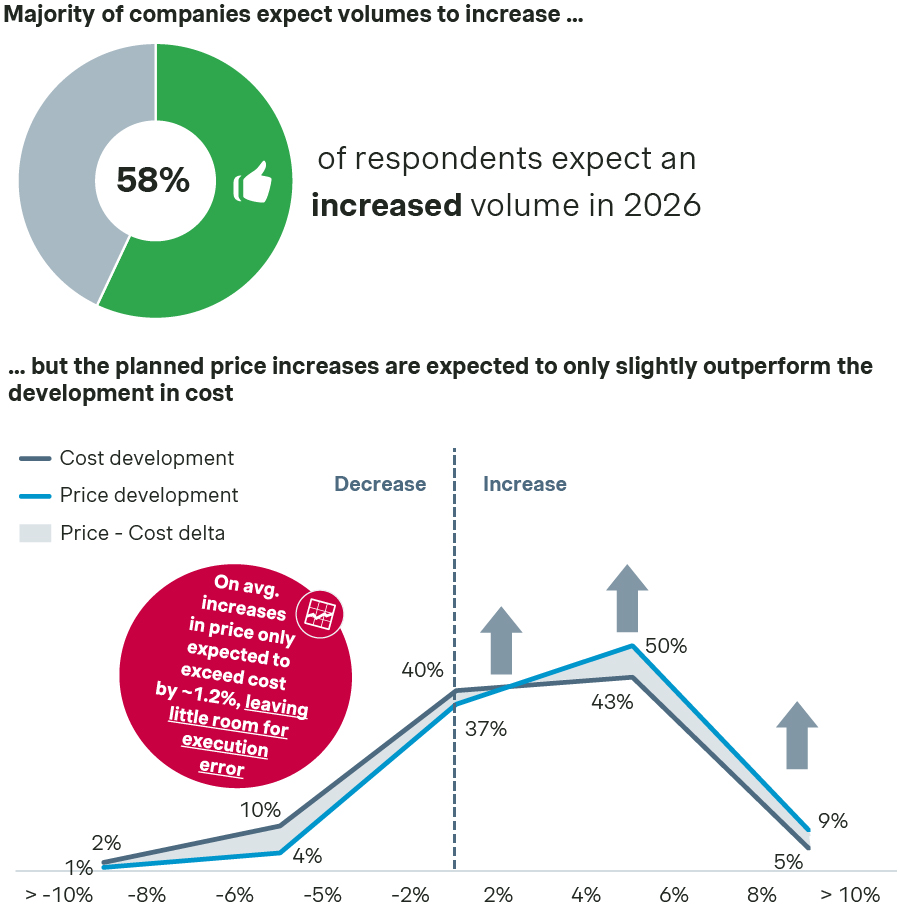

And the headroom is thin. Simon-Kucher’s Commercial Trends Study 2026 shows companies expect price increases to outpace cost increases by only around 1.2 percentage points. Meanwhile, 58% expect volume growth, which is a dangerous assumption given the consumer data above.

The short-term playbook: five actions for the next 90 days

Price increases do not fail in strategy. They fail in execution. In our previous article on CPG pricing cycles, we outlined the broader set of strategic actions available to CPG leaders. Below, we narrow that framework to what matters in the next 90 days – five specific levers where execution, not strategy, determines margin outcome.

- First, install a margin control tower – this week, not next quarter: A single source of truth on cost shocks, margin impact, and pricing actions. Daily or weekly visibility, not monthly. One accountable owner, usually the CFO working directly with commercial leadership. CEO informed at least weekly. Most companies lose money not because costs go up, but because they react two to three months too late.

- Second, move from annual pricing to continuous repricing: Annual price lists are dead in volatile environments. Indexation clauses in new contracts. Reopened existing contracts where cost movements justify the conversation. Shorter validity periods of 30 to 60 days. Targeted surcharges where clearly attributable. The goal is not perfect pricing – it is speed of adjustment.

- Third, segment aggressively – and be willing to walk away: Define clear buckets – full pass-through for low price sensitivity or high differentiation, partial pass-through for competitive but manageable categories, strategic absorption for key accounts. Then identify the low-margin, high-volatility business you cannot afford to keep carrying. Not all volume is worth keeping. This is where strong CEOs differentiate themselves: They choose margin discipline over volume reflex.

- Fourth, align sales incentives with margin, not revenue: Sales teams often delay or dilute price increases because their compensation rewards volume. When the objective shifts from volume at any price to cost recovery, the conversation shifts from discount-focused to argumentation-focused – and the result shifts from revenue growth with margin erosion to genuine margin protection. Change the objective, and you change the conversation.

- Fifth, support the front line: Most organizations don’t lack pricing strategy, they lack consistent execution in the field. Track price realization daily or weekly. Make margin leakage visible by customer and deal. Provide clear messaging, simple guidance on what to say, quick escalation support for key accounts. The front line will execute what you help them execute – and nothing else.

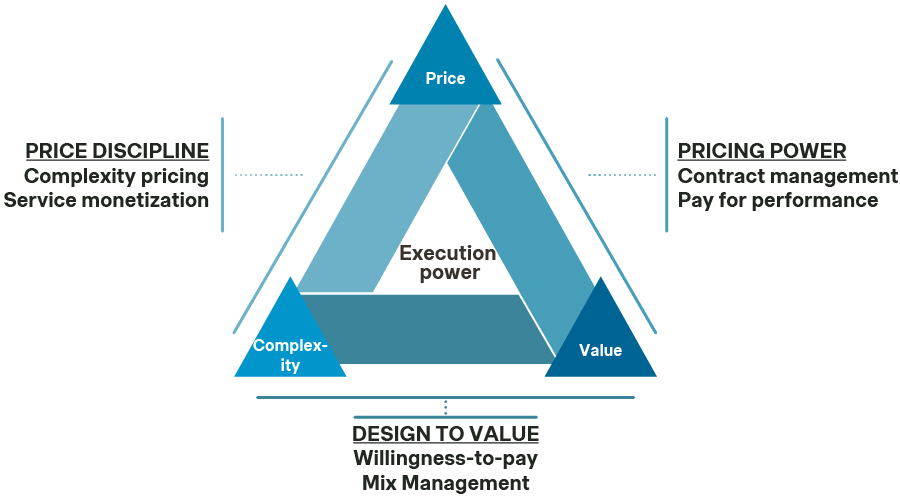

The longer arc: building institutional capability

This new playbook buys time. It does not build durable capability. That requires investment across three dimensions.

Price discipline – complexity pricing and service monetization: The insight that repeatedly surprises leadership teams, but that’s still true: Most CPG companies are too expensive on their simple products and too cheap on their complex ones. The result is an unfavorable mix – customers buy the wrong things, and the margin ranking of the top accounts is misleading. In one engagement, reallocating costs based on actual service complexity rather than revenue completely changed the ranking of the top 10 customers. The accounts believed to be most profitable were not.

Pricing power – contract management and pay-for-performance: In many cases the internal knowledge of your own contracts is often as unclear as your external knowledge of the market. This is something a lot of CEOs underestimate: Thousands of contracts, accumulated concessions, discounts that have become unconditional. Language models and structured contract analytics now make this tractable at scale. The renegotiation opportunity is usually larger than the commercial team estimates, because the team has lived with the current state long enough to stop seeing it.

Design-to-value – willingness-to-pay and mix management: Portfolio decisions must align with what consumers will actually pay for. In volatile markets, conjoint analyses are no longer one-off research exercises. They become continuous instruments for deciding which products to delist when scarce supply forces choices, which formats to push when affordability dominates, and which price points hold consumer value.

Operating model readiness: the hidden lever

All three dimensions depend on something easy to underestimate: operating model readiness. Centralized systems, standardized procedures, clear responsibilities, the digital infrastructure that makes speed and discipline possible. Companies that have standardized ERP configuration and centralized order-to-cash are seeing 20 to 30 percent cost reductions in operating expenses and over 25 percent savings in order management.

The savings matter. But the more important outcome is invisible in the P&L: the organizational readiness to execute a pricing decision at speed when the market demands it. A beautifully designed pricing strategy that takes six weeks to implement across fragmented systems is, operationally, the same as no strategy at all.

What you can and cannot control

You cannot control geopolitics. You cannot control the oil price, or whether the Strait of Hormuz stays open next week. You cannot control whether your competitors panic or hold steady.

You can control, though, how fast you react. Where you pass costs on and where you don’t. Which business you choose to keep and which you walk away from. How disciplined your execution is. How ready your operating model is to translate a decision into action without losing weeks in the handoff.

2026 will reward those who combine execution speed, pricing discipline, and operating model readiness. The winners in this inflation cycle will not be the most aggressive – aggression without discipline in a price-sensitive consumer environment is a fast route to volume loss. They will be the fastest, the most selective, and the most consistent.

The hesitation that feels safe today is the margin risk that will show up in Q3 and Q4. In the end, it comes down to the operating model, translating judgment into action at speed.

Looking to optimize your consumer goods business? As global leaders in CPG consulting and pricing, we bring the strategic insight needed to strengthen profitability and accelerate commercial growth.

Get in touch with one of our Simon-Kucher experts to learn more.