As growth slows and lending risks rise, banks can no longer rely on volume alone. Five pricing excellence capabilities can help improve margins, strengthen risk-adjusted returns, and unlock sustainable profitable growth.

Inflation is back, growth is missing, and the European Central Bank has reached for the rate lever once again. The ECB's decision on June 11 to increase interest rates comes at a difficult moment for the European economy.

According to Eurostat's flash estimate, euro area inflation accelerated to 3.2% in May this year, up from 2.8% in April and significantly above the ECB's 2% target. At the same time, economic growth remains subdued. The ECB's latest macroeconomic projections forecast euro area GDP growth of only 0.9% in 2026, reflecting weak investment activity, geopolitical uncertainty, and cautious business sentiment.

Despite the challenging macroeconomic environment, corporate lending in the euro area has remained resilient. ECB monetary statistics show that outstanding loans to non-financial corporations grew by 3.4% year-on-year in April, indicating that credit demand has not disappeared.

Despite resilient loan growth, banks are becoming increasingly selective. The ECB's latest Bank Lending Survey indicates that credit standards for corporate lending remain tight as institutions respond to heightened economic uncertainty, borrower-specific risks, and lower risk tolerance.

At the same time, supervisory authorities continue to highlight SME portfolios, commercial real estate exposures and geopolitical risks as key areas requiring close monitoring. While asset quality remains broadly stable, many banks continue to maintain conservative provisioning assumptions and heightened scrutiny of new lending decisions. As a result, the challenge is no longer simply generating volume but ensuring that every new loan delivers attractive risk-adjusted returns.

Yet profitability outcomes vary significantly across banks. What drives these differences – and what ultimately positions a bank as profitable?

Based on our project experience, five pricing-maturity factors are decisive:

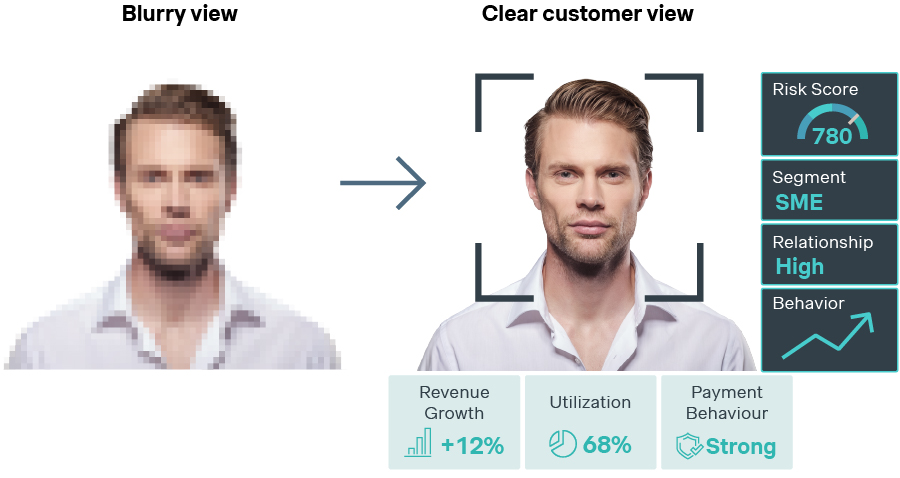

1. Develop a 360° customer understanding

Pricing excellence starts with understanding customers beyond the credit application.

Historical borrowing behavior, repayment performance, relationship depth, product usage, sector dynamics, transaction activity, and sales insights should be integrated into actionable customer segments.

In slower-growth markets, average pricing approaches become increasingly ineffective. Banks that understand customer-specific needs and behaviors can identify where additional value can be created and where pricing flexibility is justified.

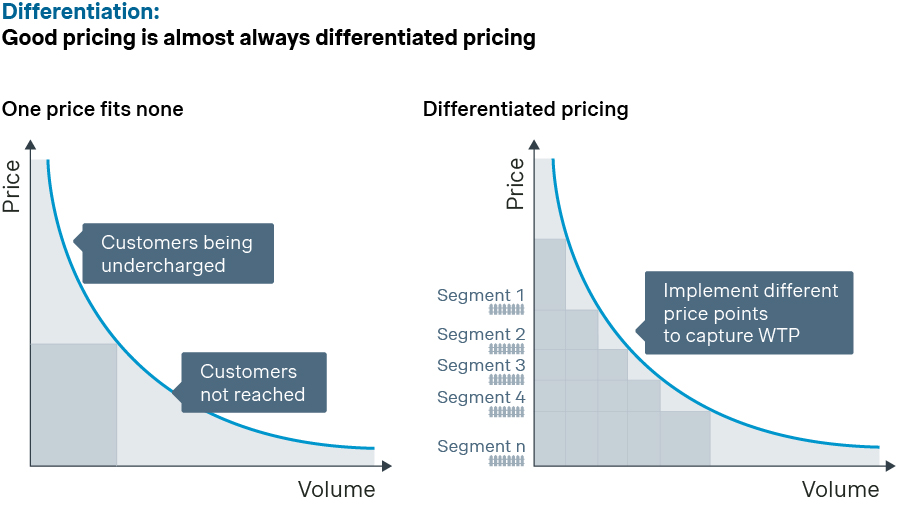

2. Differentiate pricing based on willingness-to-pay

Not all borrowers are equally price sensitive. Large corporates, international clients, and borrowers running competitive tenders typically have greater market transparency, stronger negotiating power, and access to multiple financing sources, resulting in lower achievable margins.

In contrast, many SMEs, relationship-driven clients or borrowers seeking speed, flexibility or tailored solutions are often less price sensitive and place greater value on service, expertise, and certainty of execution.

Willingness-to-pay also varies significantly by collateral structure, transaction complexity, financing purpose, and relationship depth. A fully collateralized refinancing transaction may justify a different pricing approach than an unsecured growth-financing request, even if both borrowers exhibit similar credit quality.

Leading banks therefore move beyond uniform spread grids and apply differentiated pricing corridors by segment, customer, and transaction type. This enables them to remain competitive where price sensitivity is highest while protecting margins where customer value – and willingness-to-pay – is greater.

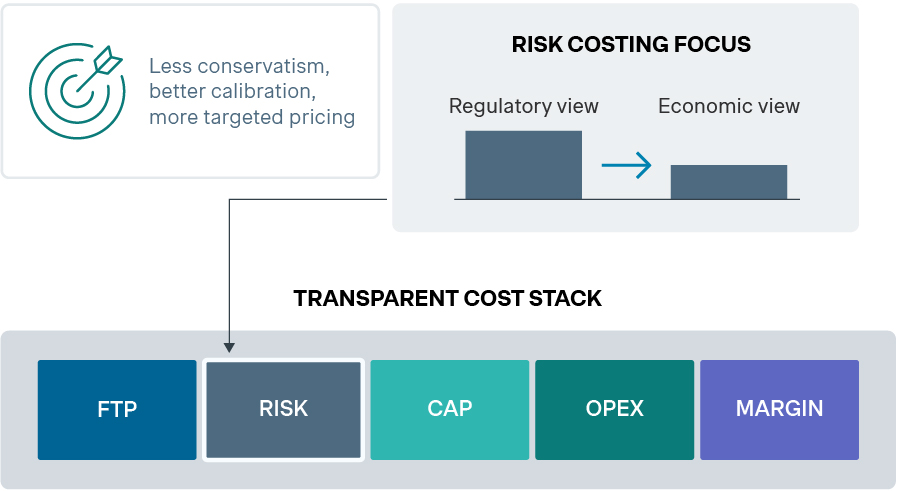

3. Price based on economic profitability

Many lending-pricing frameworks remain anchored in regulatory capital concepts and broad risk buckets. While these approaches are sufficient for compliance and portfolio oversight, they are often too coarse for differentiated commercial steering.

Economic profitability requires a more precise view of the true cost of each transaction, including funding costs, capital costs, operating costs, and risk costs. At the point of pricing, risk cost is necessarily an estimate based on expected-loss models; the actual cost of risk only becomes visible over time through defaults, recoveries, and provisioning outcomes. The closer pricing models come to this economic reality, the more accurate and commercially effective pricing decisions become.

Leading banks therefore increasingly complement regulatory metrics with economic risk models. While many banks already differentiate borrowers reasonably well through ratings and PDs, the greatest improvement potential often lies in LGD modelling and the economic recognition of risk mitigation measures such as collateral, guarantees, and of recovery prospects.

The economic value comes from reducing the gap between ex-ante risk estimates and realised credit losses. In our project experience, improved risk differentiation can create pricing impacts of 10 to 30 basis points for selected transactions and portfolios. Depending on the bank's commercial strategy, this benefit can either be retained as additional margin or selectively reinvested into more competitive pricing for attractive clients.

4. Eliminate pricing leakage

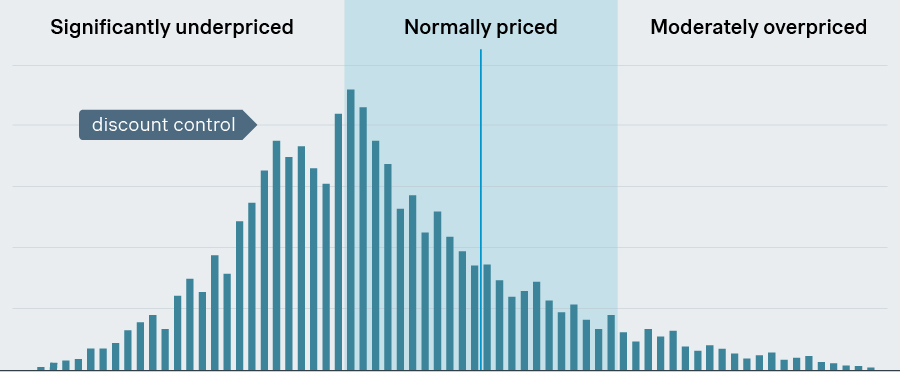

Even sophisticated pricing models create little value if pricing discipline is weak. In many corporate and SME lending portfolios, more than half of all transactions are negotiated away from the recommended price, often by 10-50 basis points.

Margin leakage often occurs through:

- Excessive spread concessions

- Fee waivers

- Unstructured discounting

- Relationship-based exceptions

- Inconsistent approval processes

The most successful banks establish clear governance frameworks, transparent approval workflows, and performance monitoring mechanisms that ensure negotiated pricing remains aligned with profitability objectives.

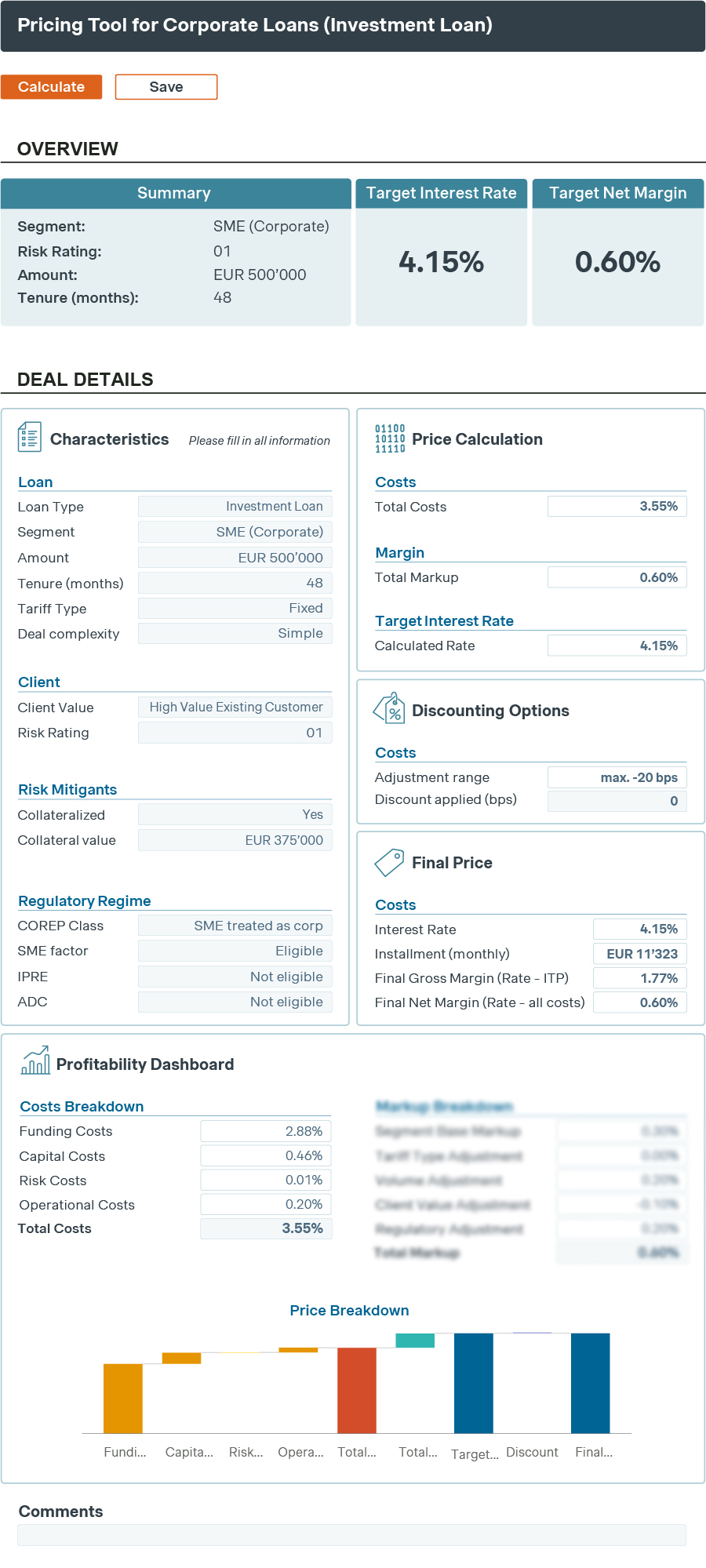

5. Turn pricing into a front-office tool

Many banks still rely on simplified pricing recommendations – if they provide systematic guidance at all. Performance analysis often takes weeks, price simulations are difficult, and centrally approved pricing changes are slow to implement across the sales organization.

Modern pricing tools help translate pricing strategy into daily decision-making. They provide differentiated price recommendations by customer, segment, and transaction type, including clear discount ranges, approval logic, and peer-pricing benchmarks. This gives relationship managers practical guidance during negotiations while creating transparency on margin impact, exceptions, and pricing leakage across the portfolio.

Conclusion: Unlocking profitable growth

The ECB's latest rate increase confirms that European banks will continue operating in a challenging environment characterized by persistent inflation, cautious borrowers, and slower economic growth.

In such markets, profitable growth rarely comes from higher volumes alone. It comes from better pricing decisions.

Banks that strengthen customer segmentation, understand willingness-to-pay, incorporate economic profitability into pricing decisions, enforce pricing discipline, and leverage smart Pricing Tools can significantly improve portfolio performance even in difficult market conditions.

At Simon-Kucher, our experience across corporate and SME lending portfolios shows that pricing excellence programs typically deliver 5% to 10% profit improvement, depending on portfolio characteristics, existing pricing maturity, and execution capabilities. In a market where growth is increasingly difficult to achieve, pricing remains one of the fastest and most sustainable levers available to improve profitability.

To explore what pricing excellence means for your business, and how to turn it into a competitive advantage, contact our specialists.