Residual value assumption can make or break lease profitability. AI can help leasing providers identify value shifts earlier and act before risks appear in traditional value sources.

The European leasing market, with annual new business consistently above €400 billion, remains a growth market, but momentum is slowing. New business volumes increased by 2.2% in the first half of 2025, reflecting continued demand for asset-based financing despite a challenging economic environment. However, as growth becomes harder to achieve, profitability increasingly depends not only on originating new business but on pricing risk correctly, particularly residual value risk. The leased-asset market is also expected to account for a growing share of corporate fleet and equipment finance over the coming years, meaning the pricing assumptions embedded in today's contracts will shape balance sheets well into the next decade.

For leasing companies, however, growth alone does not guarantee profitability. Unlike traditional lending, the economics of a lease contract depend not only on funding costs and credit risk, but also on one critical assumption: the future value of the leased asset.

A residual value (RV) forecast that is off by only a few percentage points can materially change the profitability of an entire portfolio. At the scale of the European leasing market, even small, systematic improvements in forecast accuracy translate into a multi-billion-euro opportunity.

When residual values move faster than valuation models

During 2023 and 2024, several European used electric vehicle (EV) markets experienced significant price corrections, driven by aggressive manufacturer price cuts on new vehicles, rapidly evolving battery technology, and a growing supply of used EVs coming off lease. In some cases, residual values fell faster than traditional valuation models had anticipated, leaving lessors exposed at the point of remarketing.

The same dynamic can occur in other asset classes:

- Construction equipment, following a slowdown in infrastructure spending

- Agricultural machinery, after commodity price corrections

- IT equipment, during rapid technology transitions

- Renewable-energy assets, following changes in subsidy or regulatory regimes.

In each case, the underlying challenge is the same: historical depreciation curves are backward-looking, and they often fail to capture sudden shifts in market sentiment.

The question for lessors therefore is: how can residual values be estimated more accurately before the market moves?

Why residual values matter for pricing

Residual value assumptions shape lease pricing through two distinct channels. First, the assumed RV defines the depreciation that the leasing provider must recover over the contract term, setting the cost base on which the monthly payment is calculated. Second, the uncertainty around that assumption is itself a risk that gets priced separately, typically through risk buffers or provisions built into the rate.

Both channels are sensitive to the same underlying problem: depreciation is not linear, and its speed varies significantly by asset class, age, and market conditions. A model that assumes a smooth, average depreciation curve will systematically misprice both the cost base and the risk buffer whenever actual depreciation accelerates or decelerates relative to that average, which is precisely what happened in the used EV market described above.

Consider this example:

- Acquisition cost: €50,000

- Contract term: 36 months

- Residual value assumption: €25,000

If the actual RV at the end of the contract turns out to be €23,000 instead of €25,000 – a gap of 8% – the leasing provider absorbs a €2,000 loss at remarketing on that single vehicle. Across a portfolio of 1,000 broadly comparable vehicles, a uniform shortfall of this size would imply additional losses in the order of €2 million. In practice, the gap will vary by segment, age, and mileage, but the example illustrates how a seemingly small percentage error compounds quickly at portfolio scale.

The same logic runs in reverse. If residual values are systematically underestimated, leasing providers build unnecessary risk buffers into pricing, making offers less competitive and potentially losing profitable business to those with sharper assumptions.

Better RV forecasts therefore create value in two directions:

- Avoiding remarketing losses when values fall faster than expected

- Enabling more competitive pricing where risks are lower than assumed.

How AI can improve residual value forecasting

Traditional residual value models typically rely on a well-established set of inputs: internal remarketing data, historical transaction data, third-party valuation providers, and expert appraisals.

These sources remain essential, although they inherently react with a delay to changing market conditions since they are built on data that is already a market cycle behind.

AI can complement these approaches by continuously analyzing large volumes of structured and unstructured market data, including:

- Online marketplaces and classifieds

- Dealer inventories

- Auction platforms

- Manufacturer pricing announcements

- Macroeconomic indicators

- Regulatory developments

- Industry news and market sentiment.

Rather than replacing valuation experts, AI acts as an early-warning system that surfaces market shifts months before they appear in traditional valuation databases.

Two AI valuation benefits

The value proposition differs by asset type, and is realized in two distinct ways.

- Improving precision: For high-volume assets such as corporate vehicles, where transaction data is already abundant, the benefit is precision: sharper, earlier signals on top of an already well-populated dataset.

- Closing the data gap: This benefit matters most for sparsely traded, more specialized asset classes such as niche construction equipment, agricultural machinery, or specific categories of medical or laboratory equipment. For these assets, internal transaction volumes and third-party valuation coverage are thin, and existing models lean heavily on expert judgement and broad asset-class assumptions. AI can add value even when no identical comparable exists in the market. Instead of requiring an exact match, the model draws on the multidimensional representation space of an LLM to locate assets that are meaningfully comparable in specification, application, and market positioning, then borrows signals from them. This adds a layer of market data precisely where it has historically been scarcest.

A growing number of leasing providers are already piloting overlays of this kind, typically starting with a single high-volume segment such as corporate vehicle fleets before extending the approach to other asset classes.

Illustrative case study: Identifying residual value risk earlier

The following example is based on a representative engagement with a European leasing provider seeking to improve pricing accuracy within its corporate vehicle portfolio. Details have been anonymized.

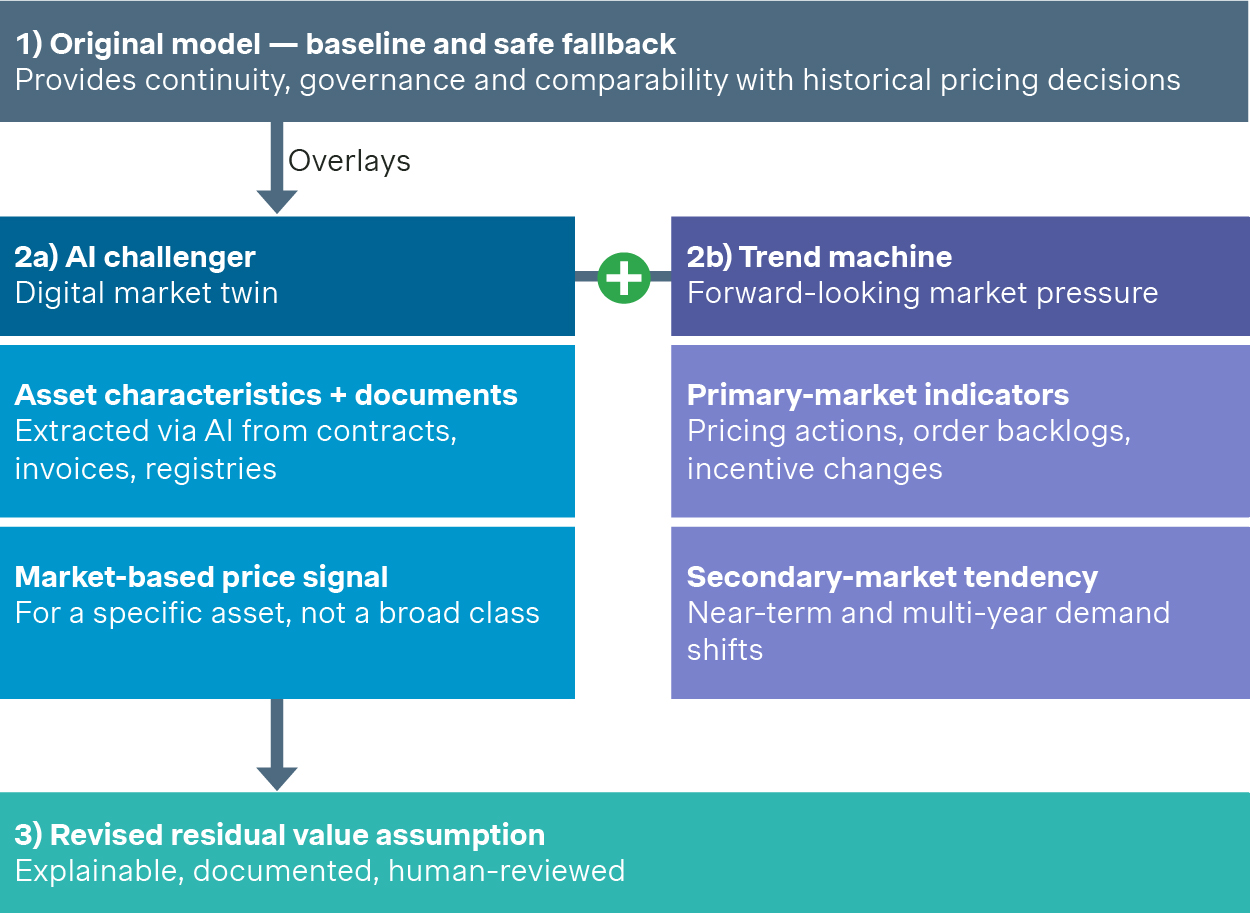

The provider did not replace its existing RV model. Instead it adopted a multi-layer architecture in which the current model remained the anchor, with two AI-driven layers added as overlays.

The architecture had three components.

1 Original model: Baseline and safe fallback

The existing residual value model continued to provide the baseline assumption, ensuring continuity, governance, and comparability with historical pricing decisions.

2a) AI challenger: A digital market twin

The AI challenger built a digital market twin for each asset, based on attributes such as brand, model, age, mileage, powertrain, equipment, and geography. Where these details were not readily available in structured databases, AI was used to extract detailed asset descriptions automatically from contract documents, invoices, and other unstructured sources. Based on this digital twin, the model searched for highly comparable assets in the market and derived a market-based price signal for that specific asset rather than for a broad asset class.

2b) Trend machine: Forward-looking market pressure

The trend machine monitored a curated set of leading indicators in the primary market, including new-vehicle pricing actions, order backlogs, and manufacturer incentive changes, and translated them into likely secondary-market tendencies. Some of these signals move ahead of near-term shifts that would otherwise only become visible in traditional residual value data once the correction has already occurred. Others speak to a longer horizon. Decisions being made in the primary market today, such as a manufacturer's powertrain roadmap or planned production volumes, shape what demand for a given vehicle type will look like several years out. This is directly relevant for contracts with three- to four-year terms being priced today.

3) Revised residual value assumption

Using this approach, the residual value assumption for the affected vehicle segment was revised downward ahead of the broader market correction becoming visible in conventional valuation sources. The adjustment was directionally consistent with the €25,000 to €23,000 example described above, though applied across a larger portfolio. Across that portfolio, the potential economic impact of acting on the signal early was estimated at around €10 million, assuming the effect materialized over a three-year horizon.

Key safeguards and design principles

Key safeguards were built into the solution design from the outset. As the AI output could influence pricing-relevant decisions, regulatory classification under the EU AI Act, model governance, and data confidentiality were addressed upfront.

The resulting setup kept the output explainable, documented, and subject to human review. Data exposure was limited by using asset data only, excluding customer and profitability information, avoiding full-portfolio batch submissions, mixing dummy requests where appropriate, and applying secure deployment, access, and audit controls.

Implications for leasing executives

Residual value forecasting has traditionally been viewed as a specialist risk-management activity. It is now becoming a strategic pricing capability that requires its own operating model, not just a better algorithm.

The closer residual value assumptions reflect actual market conditions, the more accurately lease contracts can be priced. Better forecasts reduce unnecessary risk buffers, improve competitiveness, and help protect profitability when markets move unexpectedly.

AI will not replace valuation experts, market databases, or appraisers. But used as an overlay, as in the architecture described above, it can strengthen them, analyzing a wide range of market signals in near real time and helping detect value shifts earlier than traditional approaches alone.

Building this capability typically requires action on four fronts:

- Build the data pipeline, not just the model: The quality of the digital market twin depends on access to clean asset-level data, including unstructured contract and invoice data.

- Embed the new model into pricing: Improved residual value forecasts only create business value when they influence pricing decisions. Integrate AI-enhanced residual value estimates into pricing tools, approval workflows, and portfolio steering processes.

- Pilot on a contained segment: Start with a single high-volume asset class, such as corporate vehicle fleets, to prove value before scaling across the portfolio.

- Establish model governance early: Define ownership, documentation, and human-review checkpoints from the outset before the AI Act's high-risk obligations become a blocker.

In a market where a change of a few percentage points in residual value can determine the profitability of an entire asset class, earlier insight backed by the right operating model can translate directly into better pricing decisions and stronger margins. To explore what pricing excellence means for your business, and how to turn it into a competitive advantage, contact our specialists.