US Most Favored Nation policy is typically discussed as a pricing challenge. But its implications extend beyond pure pricing and revenue forecasts. As pricing becomes more interconnected across markets, MFN-related policies may influence how assets are valued, prioritized, and transacted. Here are the implications business development teams and investors should consider.

Most Favored Nation (MFN) and its US international reference pricing (IRP) policies are often discussed through the lens of pricing pressure and revenue risk. These policies also have broader strategic implications for how pipeline assets are evaluated, prioritized, and transacted.

While important details remain uncertain, current proposals and individual White House agreements with pharmaceutical companies suggest that these companies face significantly different commercial constraints. This asymmetry is becoming a key factor in asset evaluation, partnering, and deal structuring.

While much of the discussion around MFN has focused on pricing implications, this article explores what these developments could mean for business development, licensing, and M&A decisions.

US IRP has created significant asymmetry across manufacturers

Historically, US drug prices operated at significantly higher levels and largely independent of ex-US markets. Recent US IRP developments have fundamentally changed this by directly linking US pricing to international benchmarks. Key mechanisms include policy proposals such as GENEROUS, GLOBE, and GUARD, as well as the prospective MFN model (as part of individual White House pricing agreements signed by 17 manufacturers to date).

| Mandatory MFN models | Voluntary agreements | |||

|---|---|---|---|---|

| GLOBE | GUARD | GENEROUS | Individual White House agreements | |

| Affected channels | Medicare Part B | Medicare Part D | Medicaid |

|

| Scope |

|

| Single source and innovator multiple source covered outpatient drugs |

|

| Referenced markets | 19 high-income markets | 8 high-income markets | ||

| Price benchmark |

| Second-lowest GDP (PPP)-adjusted net price | ||

Source: Simon-Kucher insights

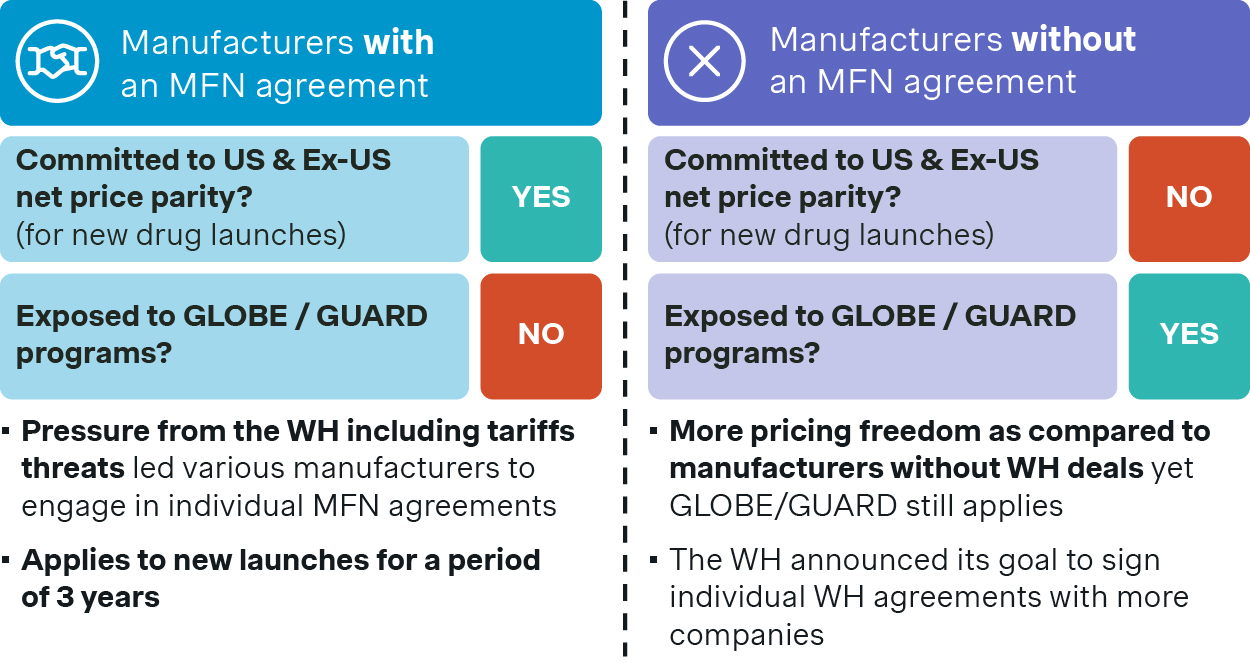

These mechanisms do not impact all companies equally. Manufacturers that have entered into individual White House agreements face significantly broader pricing interdependencies for drugs that have not yet launched, under the prospective MFN model. According to the White House announcement on May 5, 2026, these deals link US net prices to ex-US net prices across all books of business, including the commercial channel as part of the prospective MFN model.

In contrast, companies outside these agreements so far face more limited exposure, primarily through GLOBE and GUARD, which rely on list-price referencing and apply only to a subset of Medicare beneficiaries.

Source: Simon-Kucher insights

This creates meaningful differences in commercial flexibility. Companies without White House agreements may retain greater latitude to:

- Structure geographically differentiated partnerships

- Sequence launches selectively across markets

- Preserve strategic flexibility in ex-US markets

- Navigate pricing negotiations independently by geography

- Adapt commercialization strategies as the policy landscape evolves

Companies not currently subject to White House agreements should carefully consider this asymmetry when evaluating assets expected to launch in the US in the near term. For drugs planned to launch within the next 12–18 months, non-agreement manufacturers currently maintain significantly greater pricing flexibility in the commercial channel compared to companies bound by the prospective MFN model. This temporary advantage could have a material impact on launch sequencing, ex-US pricing strategy, and overall asset valuation. In practice, this may allow non-agreement manufacturers to value certain assets more favorably than manufacturers already bound by White House agreements, potentially changing bidding dynamics.

Asset exposure is becoming a critical valuation factor

The impact of US IRP is also unlikely to be uniform across assets. Exposure depends on both the acquirer and the specific characteristics of the therapy.

Assets with greater commercial channel exposure are particularly attractive for companies without White House agreements. Because GLOBE and GUARD primarily affect Medicare beneficiaries, non-agreement manufacturers can still maintain meaningful pricing flexibility in the much larger commercial segment. Conversely, for manufacturers subject to White House agreements, US IRP may apply across payer channels, including the commercial channel, increasing overall pricing exposure.

Orphan and specialty assets are particularly notable in this context. While future exemptions remain uncertain, orphan drugs have historically received differentiated treatment across multiple policy frameworks and may therefore face lower exposure to future MFN-related policies. These therapies also tend to exhibit narrower international pricing dispersion and lower Medicare exposure relative to broader primary care markets, particularly when they primarily serve younger patient populations.

As a result, pricing exposure may become a more important dimension of asset attractiveness than it has been historically. For investors and business development teams, MFN exposure is becoming another dimension of commercial diligence. An asset’s value may increasingly depend not only on its clinical profile and market opportunity, but also on how pricing policies affect commercialization flexibility across geographies and payer channels.

Alongside traditional considerations such as clinical differentiation, peak sales potential, competitive positioning, and probability of success, BD teams and investors may need to assess:

- Eligibility and exposure to US IRP mechanisms

- Asset exposure across different payer channels

- Relative US and ex-US pricing potential

- Reimbursement channel dynamics

- Scenario-based assessment of potential MFN impacts on the US business

These considerations could shape not only how assets are valued, but also which ones are prioritized and by whom.

Geographic strategy gains prominence in dealmaking

US IRP is also likely to elevate the role of commercialization geography in BD strategy. The traditional “US-first” model, with ex-US expansion following through partnerships or sequential launches, may require greater nuance.

As US and ex-US pricing become more interconnected, geographic strategy may play a larger role in transaction planning. This could affect how companies think about:

- Geographic rights structures

- Launch sequencing and market prioritization

- Ex-US partnership strategy

This also increases the importance of contractual pricing mechanisms. Historically, licensors often gave partners broad autonomy over ex-US pricing decisions. With growing spillover risks under MFN/IRP, rights holders are expected to demand stronger safeguards. Transfer prices are one key tool to help secure higher ex-US net prices. Other options include approval or veto rights on major pricing decisions, minimum net price floors, and incentive-aligned royalty structures.

Such governance provisions are expected to add complexity to negotiations. Partners may seek compensation (e.g. adjusted royalties, milestone payments, or shared cost structures) if their pricing flexibility is restricted. As a result, deal structures may increasingly include detailed pricing governance clauses.

Europe, Japan, and China account for approximately one third of global pharmaceutical sales and will remain key drivers of asset economics. However, companies may adopt more dynamic approaches as they balance price potential, launch timing, and potential spillover effects back into the US market.

Geographic considerations are also likely to differ across assets. Highly differentiated therapies addressing significant unmet need may continue to support broad global commercialization strategies and premium pricing across markets, despite US IRP pressures. By contrast, more incremental innovation may face a more complex set of geographic trade-offs if pricing interdependencies continue to expand.

Certain markets may gain renewed attention. Gulf countries (GCC), China, and other emerging launch geographies, for instance, could become more attractive in partnering discussions due to their commercial potential and more limited exposure to current US IRP reference frameworks.

As a result, asset forecasts and BD negotiations may reflect these strategic considerations and will become even more complex moving forward. Geographic rights, co-commercialization structures, and regional flexibility could become more central components of transaction discussions than they have been historically.

Strategic flexibility as a differentiating factor

The ultimate impact of US IRP policy developments remains uncertain. Key questions around implementation scope, referenced pricing methodologies, channel applicability, and future exemptions continue to evolve.

Nevertheless, differences in manufacturer exposure along with the growing interconnection between pricing policy and commercialization strategy are already influencing how assets are valued and prioritized. Payer mix, geographic footprint, reimbursement dynamics, and pricing interdependencies are likely to play an increasingly important role in business development decisions.

In this environment, the ability to preserve strategic flexibility across markets and payer channels may emerge as a key differentiator in pharma and biotech dealmaking.

It is important to note that the US administration has signaled a clear intent to expand the prospective MFN model to more companies, similar to the individual White House agreements signed by 17 manufacturers to date. As a result, additional small- and mid-sized pharmaceutical and biotech companies could enter similar arrangements going forward. While this may narrow current asymmetries over time, near-term differences in commercial flexibility are likely to remain relevant for dealmaking.

As MFN-related policies continue to evolve, companies will need a clearer understanding of how pricing, reimbursement, and commercialization strategies interact across markets. Those who assess these dynamics early will be better positioned to make informed acquisition, licensing, and partnering decisions.

To discuss how evolving MFN policies may affect asset valuation, commercial strategy, or transaction diligence, reach out to our experts today.

With contribution from Zach Gray.