Most Favored Nation policy is now a commercial reality. We examine the possible scenarios of MFN drug pricing.

Since President Trump's executive order on MFN pricing just 12 months ago, the policy has already taken the pharmaceutical industry on a remarkable journey of twists, turns, and escalating consequences.

What began as a policy thought experiment has hardened into a commercial reality that stakeholders can no longer ignore. And while the outlines of MFN are far clearer today than they were a year ago, the road ahead may be even more uncertain than the one behind us. Much like Odysseus on his voyage home, pharmaceutical companies now face a series of hazards and irreversible choices that will determine whether they have navigated wisely or steered toward financial ruin.

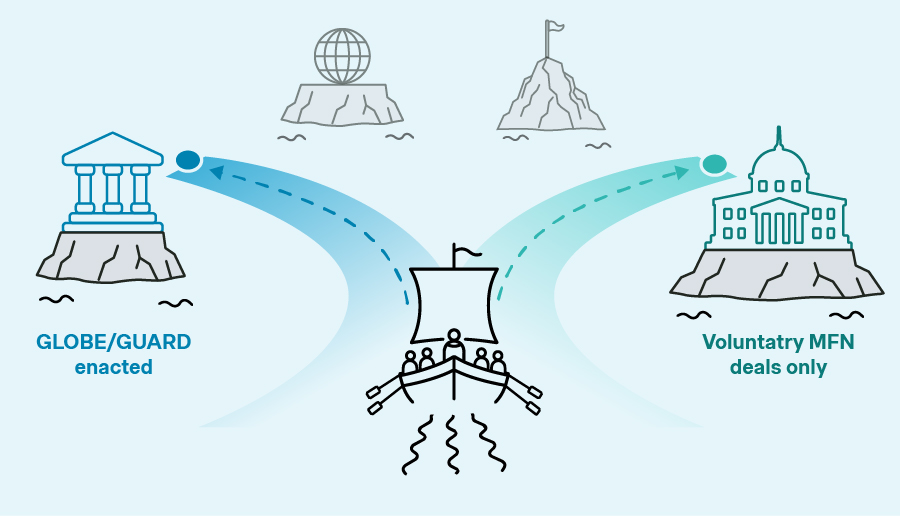

The fate of GLOBE and GUARD

The first major decision point on this next leg of the voyage is the fate of GLOBE and GUARD. As we discussed in our earlier articles, the comment period for both models closed in February after drawing hundreds of submissions from pharmaceutical manufacturers and industry associations, provider groups, patient advocacy organizations, and other interested stakeholders. Centers for Medicare and Medicaid Services (CMS) has not yet signaled its timeline , but if the agency intends to launch GLOBE in the fourth quarter as proposed, final decisions would need to come by summer. That makes the coming months a critical test of whether the impact of MFN is limited to the confidential White House agreements, or begins to harden into a formal demonstration-model architecture with direct operational consequences across Medicare.

Will GLOBE and GUARD models still make sense?

Before one assumes that GLOBE and GUARD are destined to become the next pillars of MFN, it is worth asking first whether they will ever be implemented in anything like their proposed form.

The White House has now reached MFN agreements with manufacturers representing 86% of branded pharmaceuticals in the US. The administration has simultaneously intensified its tariff rhetoric while pressing additional manufacturers to strike their own deals by June 11. If the White House agreements effectively shield participating manufacturers from GLOBE and GUARD, then the practical rationale for the demonstration models begins to erode. Would CMS really press ahead with a program if the overwhelming majority of branded Medicare spending were exempt – and if any remaining share shrank further as more companies signed deals?

Such a system would be operationally awkward and legally precarious – inviting not only first-day challenges to the models themselves, but fresh claims that exempting most of the market while burdening a small remainder is inherently anti-competitive.

It is also worth recalling what President Trump emphasized – and what he did not – when he sent his July 31, 2025 letters to the initial 17 manufacturers. The administration's public priorities were framed around achieving savings in the Medicaid program, lowering some patient costs through direct purchasing, strengthening domestic manufacturing, and realigning launch prices for new medicines across all channels.

That makes it reasonable to ask whether GLOBE and GUARD were, at least in part, instruments of leverage: policy threats designed to bring manufacturers to the table and secure "voluntary" agreements on the White House's preferred terms. If so, then the combination of Center for Medicare and Medicaid Innovation (CMMI) demonstration risk and Section 232 tariff pressure may already have served its central purpose by inducing 17 of the world's largest manufacturers to accept those objectives – at least for the next three years.

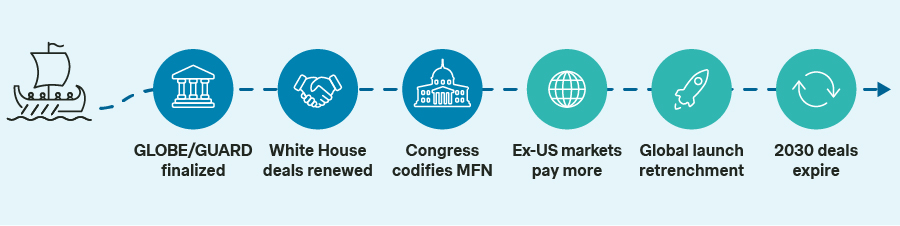

Beyond three years: What happens when the agreements expire?

That brings the voyage to its next major decision point: what happens when the current MFN agreements expire? In Homer's Odyssey, Odysseus descends into the Underworld to learn what lies ahead. Pharmaceutical CEOs need not do anything quite so dramatic, but they do need to think seriously about the many possible futures that could unfold once these three-year arrangements begin to run out.

The politics are too fluid to justify much confidence about the 2026 midterms or the presidential election in 2028, though bipartisan interest in reducing US drug costs persists. The deeper uncertainty lies in the method. Senator Bernie Sanders' recent attempt to "codify" MFN pricing borrowed the surface language of Trump's approach, but the mechanics were meaningfully different: a distinct reference basket, a median-based methodology, and an apparent reliance on list prices without the GDP-PPP adjustment that is a central component of the administration's own framework.

A Democratic majority in 2027 would almost certainly use subpoena power to probe the terms of the agreements signed by the 17 manufacturers. That, in turn, could set off a distinctly Washington drama: would companies comply and expose the details of arrangements they have treated as highly confidential, or would the White House seek to shield them under claims of executive privilege? Either path would push MFN out of the pricing arena and into a new phase of legal and political confrontation.

The global response is becoming more complicated

Outside the United States, the response to Trump's MFN agenda is splitting into competing camps. Some countries, including Israel and South Korea, have moved to strengthen the confidentiality of net pricing agreements, while France has moved to preserve it. These steps affect only GLOBE and GUARD, not underlying willingness to pay, and they do not address the deeper problem the MFN deals create: net price alignment across channels for new therapies under prospective MFN.

The most notable sign of movement in the direction the administration wants is the US-UK trade deal, which included provisions to loosen cost-effectiveness thresholds and increase overall pharmaceutical spending in Britain. But elsewhere the signs have been less encouraging. Germany has moved toward tighter cost controls, while politicians in Switzerland and Australia have made clear they have little interest in moving closer to US price levels.

That matters because the prospect of higher ex-US willingness to pay was the principal carrot the administration offered manufacturers in exchange for signing these "voluntary" agreements. If that willingness to pay does not materially increase, then manufacturers will remain trapped between the two hazards described in our previous article: the Scylla of narrowing launches to protect US prices, or the Charybdis of broader global launches at lower overall price levels.

The expansion risk if GLOBE and GUARD do take hold

Beyond the three-year horizon lies another fork in the path: the future of GLOBE and GUARD, should they be implemented. As currently designed, the demonstration models would have a relatively modest economic effect, since the rebates apply only to 25% of the populations in Medicare Part D and B (FFS). But that limited scope should not be mistaken for limited significance in the future.

If CMS can show that the models reduce spending without harming patient access or outcomes, CMMI would have the authority to expand them across the full Medicare population without new legislation. At that point, the financial consequences would become far more substantial. And it is entirely possible that some of the models' current guardrails – the minimum-spend eligibility thresholds, the narrow set of drug categories, and the relatively static structure of the international reference price – were included less as enduring policy choices than as practical simplifications for the demonstration phase. If GLOBE and GUARD evolve from pilot programs into established CMS policy, many of those constraints could disappear as well.

Navigating what comes next

If the first year of MFN was defined by shock and improvisation, the next several years will be defined by branching futures.

The fate of GLOBE and GUARD, the durability of the White House agreements, the results of the 2026 and 2028 elections, the willingness of ex-US markets to pay more, and the possibility of congressional codification all represent separate turns in the same voyage. None of them, on its own, will determine the final destination. But taken together, they will shape whether MFN becomes a temporary disruption, a durable pillar of US drug policy, or the beginning of a more fundamental reordering of how global pharmaceutical innovation is financed.

That is why the real lesson of this odyssey is not simply that manufacturers must survive the passage between Scylla and Charybdis. It is that they must prepare for many more islands, storms, and forks in the path still to come.