The affluent market has become the new competitive growth priority in wealth management. Institutions that treat it as a scaled-down version of private banking will struggle. Those that redesign their operating model around lifetime value, hybrid delivery, and WealthTech-enabled scale will define the next wave of growth.

Competition for the wealthiest private banking clients has long been intense. Financial institutions have fought relentlessly over margins, mandates, and long-standing relationships at the top end of the market. Today, the competitive focus is expanding. A new battleground is emerging in the affluent segment, where banks and digital wealth players alike see the next wave of scalable growth.

For many banks, the affluent segment represents an attractive growth opportunity. These clients already hold meaningful assets and show strong potential for future wealth accumulation. Yet capturing this opportunity is not straightforward. Traditional private banking models struggle to scale economically into the affluent space, while retail-style propositions fail to deliver the advisory quality and relevance these clients now expect.

Institutions that outperform understand that the affluent opportunity cannot be captured simply by extending private banking downward or scaling retail upward. It requires a deliberate, end to end approach that defines who to target, how to acquire, what to offer, how to serve, and how to capture value, with scalability and commercial discipline built in from the outset.

A diverse, demanding, and dynamic client base requires multidimensional excellence

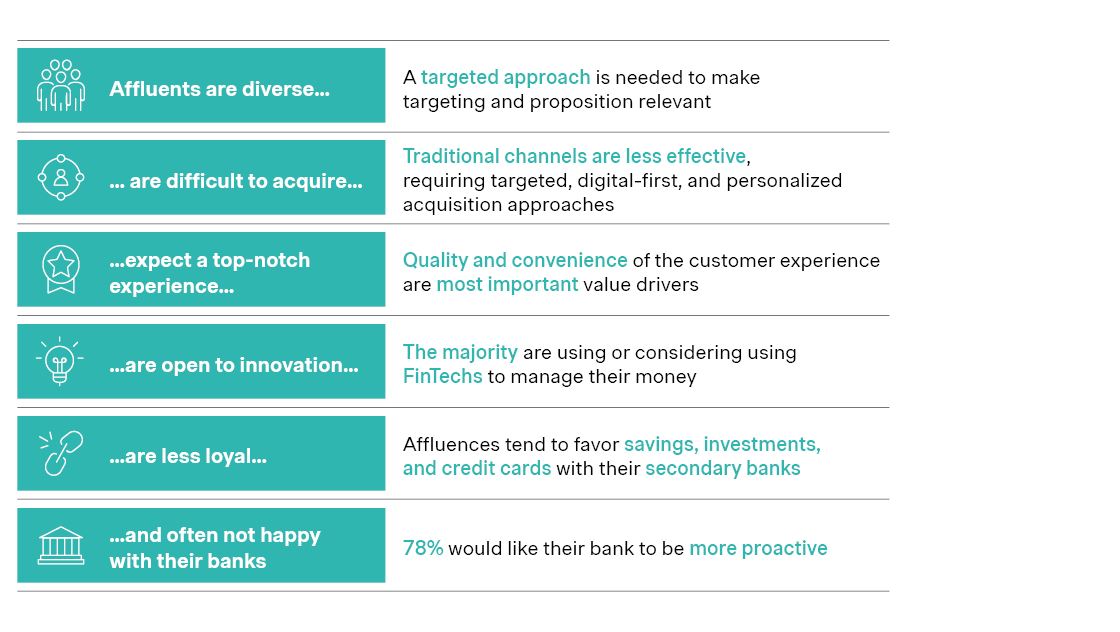

Affluent clients sit between retail and private banking. They expect seamless digital experiences, but still value expert advice at critical decision points. Compared with traditional private banking clients, they are less loyal, more open to innovative and digital wealth solutions, and more selective in where they place their savings, investments, and credit relationships.

Insights from our private banking global market study

Who to target: From broad affluent pools to value-based micro-segments

Most affluent strategies still rely on simple asset thresholds. While necessary, this approach is too blunt to support sustainable growth.

Banks that outperform build a micro-segmentation logic anchored in needs and life stages, not just current assets. Consider three clients within the same wealth band: a self-employed doctor scaling their practice, a lawyer entering peak earning years, and an inheritor at the early stage of a wealth transfer. Their balance sheets may look similar today, but their advice needs and revenue potential differ materially.

In practice, this means combining data and sales insights to distinguish between affluent sub-segments by life stage, profession, liquidity events, and investment behavior. Such granularity determines where banks compete and how they win. It informs which clients to prioritize, where to invest acquisition resources, how to design propositions, and how to deploy advisory capacity. Without this clarity, affluent strategies quickly become expensive and unfocused.

How to acquire: From relationship-driven growth to a scalable acquisition engine

Traditional private banking acquisition relies heavily on referrals and advisor networks. In the affluent segment, this model quickly reaches its limits. Competition for attention is intense, and many potential clients are not actively looking for a new primary banking relationship.

Leading banks are professionalizing acquisitions in two ways. First, they shift from product-led campaigns to relevance-driven, full funnel journeys. Brand visibility is important, but precision – delivering relevant content through the right channels – now drives conversion. Banks use educational content, events, academies, and targeted insights tied to life moments to move prospects from awareness to consideration and conversion. Digital and virtual channels play a key role, allowing banks to attract and qualify affluent prospects before human advisors engage.

High performing institutions do not rely on gut feeling or generic assumptions about what resonates with affluent clients. They systematically test and prioritize channels, messages, and journeys that actually drive engagement and conversion for each target micro segment.

Second, banks are redefining roles and responsibilities. Dedicated acquisition specialists convert qualified leads to meeting appointments, while advisors focus on high-value interactions. This division of labor enables scale without relying on ever increasing advisor headcount. Institutions also train advisors and sales specialists to align with priority micro-segments. One highly successful private bank, for example, operates a dedicated advisory team focused exclusively on doctors and dentists.

What to offer: A scalable premium proposition, not private banking by default

Affluent clients expect a premium experience, but few banks can economically deliver full private banking investment solutions at scale. Traditional retail banking offerings, however, rarely address the complexity and advisory expectations of these high-potential wealth households.

Top tier institutions differentiate by creating a dedicated customer concept, service model, and offering tailored specifically to affluent clients. For example, a leading Nordic bank recently moved its affluent clientele from retail branches into a centralized private banking and wealth management platform.

Successful propositions shift from product centric navigation to holistic wealth planning. Instead of leading with individual products, they frame conversations around goals, life events, and long-term financial outcomes. This reframing helps clients progress from savings to structured investing and from fragmented decisions to coherent portfolios.

Leading banks must also balance personalization with scalability. Fully bespoke advisory models do not scale economically, while standardized, digital-only solutions fail to sustain engagement. Modular portfolio building blocks provide an effective middle ground. Structured core solutions with selective themes and preferences delivers personalization while maintaining operational discipline.

How to serve: A digital-first hybrid offering enabled by WealthTech rather than headcount

Delivering a premium experience to affluent clients – who are digital-first, but not digital-only – cannot rely on advisor capacity alone. Serving this segment requires digital capabilities embedded across the journey and human expertise concentrated where it creates most value. As a result, hybrid service models are becoming standard.

In leading banks, digital capabilities extend well beyond transaction execution. They support client discovery, portfolio insights, proactive alerts, and guided decision-making. Advisors, in turn, rely on tools that surface insights, identify opportunities, and enable proactive outreach grounded in client context.

WealthTech – the integrated stack of modular platforms, API-based architectures, and AI-supported capabilities – underpins this model. It allows banks to scale digital first journeys such as portfolio construction, optimization, and monitoring, while equipping advisors with concrete, data-driven actions where human interaction adds the most value. This shifts the operating model away from administration-heavy, advisor-first delivery toward a more automated, insight-driven service model centered on client outcomes.

How to capture value: From short-term monetization to CLTV driven value models

Many affluent strategies still apply pricing models and margin expectations rooted in traditional private banking. While this approach has historically delivered strong returns at the top end of the market, it is misaligned with the competitive dynamics of the affluent market. Digital wealth players are setting new benchmarks with simpler, more transparent, and often more aggressive pricing structures – frequently bundled with access to human advice.

To compete effectively, banks need to move beyond short-term revenue optimization and adopt a customer lifetime value driven perspective that reflects the long-term potential of affluent clients.

Successful institutions align pricing with their proposition and service models. They pair transparent pricing with selective, value-based monetization across advisory, investment, and broader wealth services. This creates the foundation for sustainable economics, where banks invest ahead of the client’s wealth curve and capture value over time as assets accumulate and relationships deepen.

Implications for senior decision-makers: Turning affluent ambition into scalable growth

The affluent segment represents a significant growth opportunity for banks that successfully scale selected private banking capabilities to a broader, high-potential customer base. However, incremental adjustments to existing models will not be enough.

Sustainable success demands an integrated approach across targeting, acquisition, proposition, and service delivery. WealthTech-enabled operating models enable banks to deliver personalized advice and investment solutions at scale while maintaining efficiency and flexibility.

Banks that treat the affluent segment as a distinct business model rather than a coverage extension will be best positioned to unlock sustainable growth in the next phase of wealth management.