Recap

Semiconductors transitioned from high-cost, government-funded projects in the 1950s to the mainstream adoption of integrated circuits in the 1960s. The 1970s accelerated this momentum, driven by the rise of personal computing, memory chips, and telecommunications. Global competition intensified as Japan emerged as a major player, challenging U.S. dominance in semiconductor manufacturing. Pricing became more complex due to macroeconomic events like inflation, trade policies, and energy crises. While manufacturing costs declined with better yields and economies of scale, the decade also saw early trade disputes and the beginning of semiconductor price wars.

Introduction

The 1980s formed a remarkable bridge between the foundational shifts of the 1970s and the explosive innovations of the 1990s. Semiconductors, once primarily the domain of large-scale computing and specialized industrial applications, were fast becoming ubiquitous components in personal computers, consumer electronics, telecommunications, and automotive systems. At the same time, global competition reached new heights, fueling both fierce price wars and major strides in process technology.

Pricing models in the 1980s grew more complex and strategic. Manufacturers grappled with surging demand but also faced significant volatility: trade friction (particularly between the United States and Japan) escalated, currency fluctuations made planning difficult, and production overcapacity at times led to steep price drops. Despite these challenges, the enduring trend of declining cost-per-transistor continued—yet this decade also demonstrated that technology leadership alone was not enough to guarantee profitability without astute pricing and market strategies.

In this fourth installment of our historical series, we examine how semiconductor pricing models evolved in response to new market dynamics, government interventions, and major technological milestones. Understanding this era illuminates many of the foundational practices that still influence modern-day semiconductor pricing and global supply chains.

Shaping forces of the 1980s semiconductor market

PC revolution and mass adoption

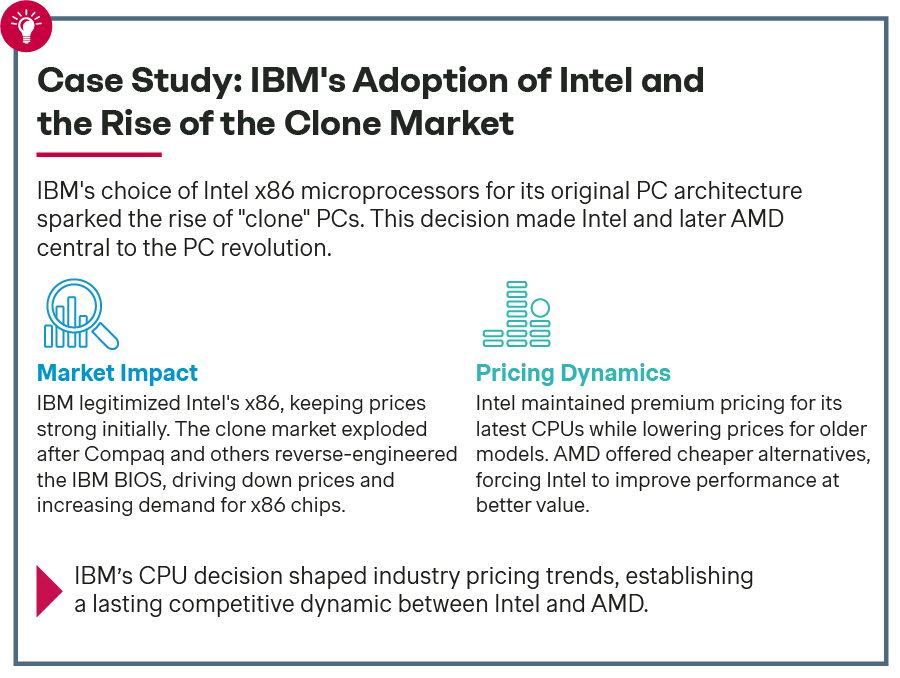

By the early 1980s, personal computers were moving from a hobbyist curiosity to a household reality. Home and small-business computing boomed, largely thanks to IBM’s PC (introduced in 1981) and subsequent clones that adopted Intel’s x86 architecture. The rapid adoption of these machines had a profound impact on semiconductor demand, especially for microprocessors, memory chips, and supporting logic.

Microprocessor leadership: Intel’s x86 family quickly became the dominant central processing unit (CPU) line for personal computers, creating massive demand for its microprocessors. A combination of volume-driven cost reduction and intellectual property licensing (to companies like AMD) helped shape pricing strategies that would remain relevant for decades.

Memory bottlenecks: As software grew more sophisticated, PCs required increasingly larger amounts of DRAM. Combined with new generations of graphical user interface (GUI)-based operating systems, this translated into brisk volume growth—though not without price swings tied to global capacity expansions.

Growth of telecommunications and industrial automation

Alongside the PC boom, telecommunications expanded with digital switching systems, satellite communications, and the beginnings of mobile telephony. These new markets demanded large volumes of reliable semiconductors for signal processing and network infrastructure. On the factory floor, programmable logic controllers and robotic systems further broadened industrial use cases. Demand was growing across multiple sectors simultaneously, intensifying competition among semiconductor producers.

Entry of emerging markets

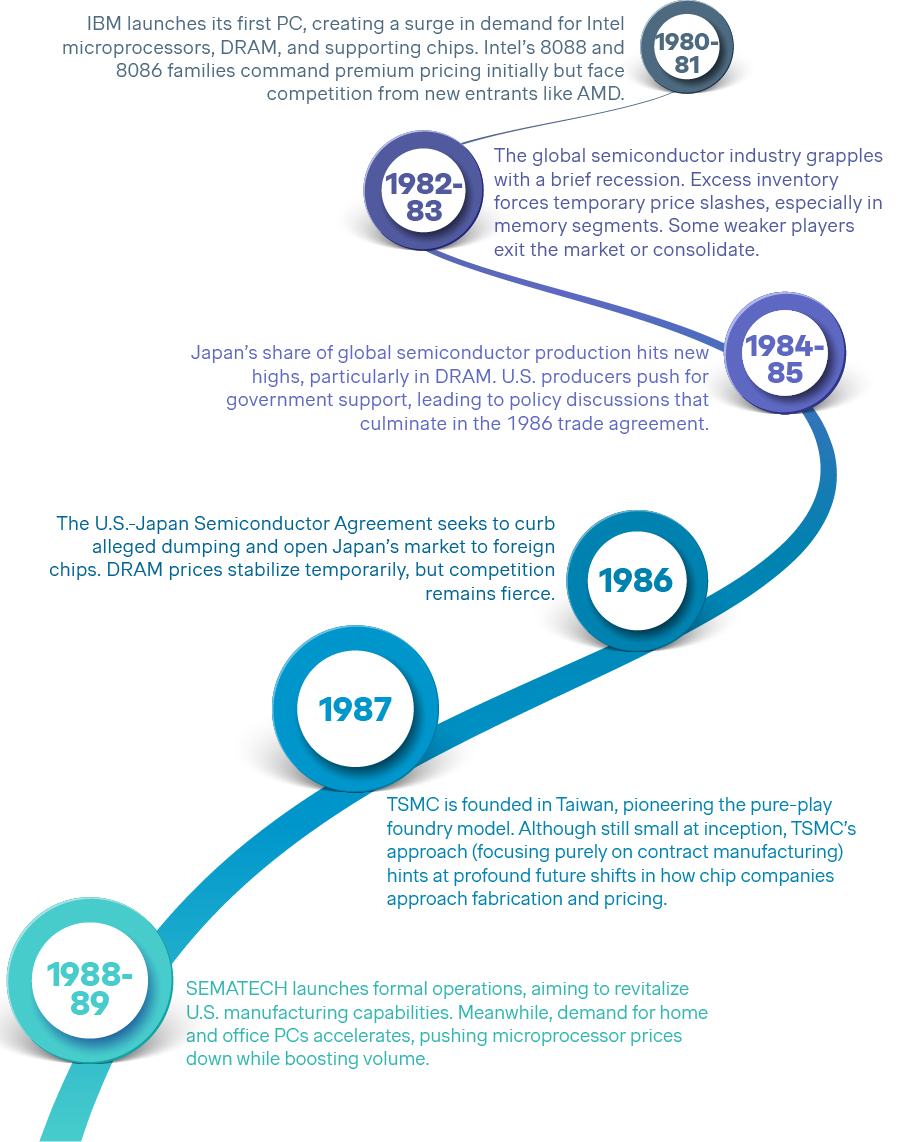

While the U.S. and Japan dominated global production, other regions—particularly South Korea and Taiwan—began investing heavily in semiconductor manufacturing. Samsung in South Korea, for example, laid the groundwork for what would become one of the world’s leading memory and logic suppliers, while in Taiwan the founding of TSMC (Taiwan Semiconductor Manufacturing Company) in 1987 introduced the concept of a pure-play foundry model. Although these entrants were still ramping up in the 1980s, they foreshadowed a more geographically distributed industry.

Major industry events and their pricing repercussions

U.S.-Japan trade tensions

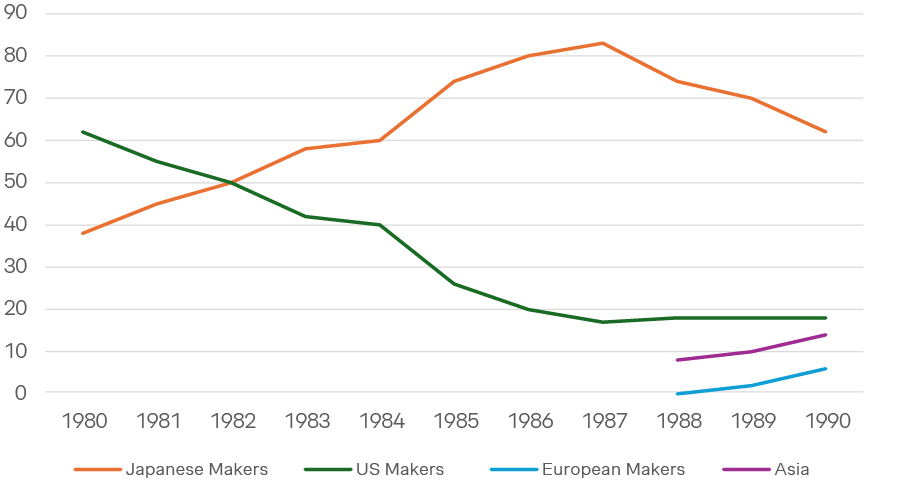

During the mid-1980s, the United States accused Japanese semiconductor companies of dumping memory products (particularly DRAM) at below-cost prices in the U.S. market. American producers struggled to compete on cost and, in some cases, found themselves pushed out of high-volume segments.

Impact on pricing: Following negotiations, the two countries signed the 1986 U.S.-Japan Semiconductor Agreement, which aimed to address dumping concerns and open up Japan’s market to foreign semiconductors. In practice, it led to some stabilization of prices in certain memory segments, but it also highlighted the increasingly political nature of semiconductor pricing.

Formation of SEMATECH

Concerned about the competitiveness of the U.S. semiconductor industry, key players and the U.S. government joined forces to form SEMATECH (Semiconductor Manufacturing Technology) in 1987. The consortium facilitated collaborative research among U.S. semiconductor companies to improve manufacturing processes and reduce costs.

Impact on pricing: By sharing best practices and pooling resources, SEMATECH aimed to accelerate yield improvements and technology adoption, indirectly influencing pricing by helping U.S. firms remain cost-competitive with Japanese memory producers.

Shifting wafer sizes and process advances

Throughout the 1980s, wafer sizes increased from four inches to six inches (and some early adoption of eight-inch wafers by the very end of the decade). Process geometries shrank from the several-micron range into the sub-micron realm, laying the groundwork for higher densities and faster device performance.

Impact on pricing: Larger wafers and improved yields meant more chips per wafer, driving down per-unit manufacturing costs. However, capital investments for new fabs soared, and this higher financial risk made strategic pricing decisions critical to recover massive R&D and equipment expenses.

Global share of DRAM sales manufacturing (1980-1989)

Timeline of key pricing milestones in the 1980s

Evolving cost structures and yield imperatives

In many respects, the 1980s represented a coming of age for semiconductor manufacturing. While the industry had already embraced partial automation, this decade saw more advanced fab equipment, tighter process controls, and new packaging technologies.

Advanced lithography

Steady improvements in photolithography equipment—such as the transition to deep ultraviolet (DUV) wavelengths—enabled sub-micron geometries by the decade’s close. Although each iteration demanded hefty investments, successful nodes provided a significant cost-per-transistor advantage.

Wafer size and throughput

Moving to larger wafers effectively multiplied the number of dies per run. Still, it required retooling or building new fabs with updated robotics, cleanroom standards, and high-precision wafer-handling systems. Once yields improved, the cost-per-chip advantage justified these investments.

Packaging innovations

DIP (Dual In-line Package) remained common early in the decade, but more advanced packaging options—like plastic leaded chip carriers (PLCCs), pin grid arrays (PGAs), and surface-mount technology (SMT)—gained popularity. Although packaging was a smaller portion of total manufacturing cost than wafer fabrication, incremental changes in this area yielded minor but relevant cost savings.

All these refinements worked in tandem to lower the effective cost of producing semiconductor devices. Yet, they also increased the upfront capital burden, intensifying the imperative to balance prices, volumes, and market share to recoup massive fab investments.

Shifts in pricing models: from cost-plus to strategic differentiation

Value-added differentiation

With rising competition, many companies began differentiating their products through unique features—such as lower power consumption, on-chip cache memory for microprocessors, or specialized coprocessor functions. Instead of relying on a simple cost-plus margin, manufacturers increasingly priced their devices based on the specific performance and reliability advantages they delivered.

Intel and AMD

Intel initially commanded premium prices for x86 CPUs by offering new performance features and leveraging its ties with IBM and other major PC makers. AMD, legally licensed to manufacture x86 chips, often priced its versions more competitively to gain share, challenging Intel to refine both its technology and pricing strategies.

DRAM suppliers

DRAM manufacturers sought to differentiate on reliability, speed grades, or packaging conveniences. Yet, as memory became more commoditized, many found they had to rely on operational excellence and scale to maintain margins.

Commodity vs. specialty markets

By the mid-1980s, segments of the semiconductor market had started to resemble commodity markets—particularly DRAM, where numerous suppliers produced similar products at large volumes. In these commodity-like arenas, price often became the deciding factor once a manufacturer had demonstrated baseline reliability.

By contrast, specialty applications—such as military-grade components or custom ASICs (Application-Specific Integrated Circuits)—remained less price-sensitive. Manufacturers serving these niches could afford to set higher margins, provided they delivered validated performance and long-term reliability.

Conclusion: The 1980s—where semiconductor pricing met geopolitics and scale

The 1980s took the semiconductor sector beyond the era of purely technology-driven cost declines and into a more complex reality. Demand surged as personal computers, telecommunications, and industrial automation expanded rapidly. Meanwhile, new producers—particularly in Asia—stepped onto the global stage, intensifying competition. Macroeconomic forces, from trade wars to national consortia, played critical roles in shaping how prices moved.

On the one hand, the continuous improvement in wafer sizes, lithography, and yield optimization maintained the long-standing tradition of declining cost-per-transistor. On the other hand, trade disputes and allegations of dumping highlighted how semiconductor pricing was no longer just about engineering breakthroughs but also about political and economic leverage. Companies that mastered both the technology roadmap and global market dynamics found themselves best positioned to thrive.

Key lessons

The 1980s underscore the fact that semiconductor pricing cannot be decoupled from its broader environment. While Moore’s Law kept transistor costs on a downward trajectory, the actual end-user pricing hinged just as much on global capacity, macroeconomic trends, and government interventions. The period also reminds us that strategic product differentiation—delivering real value beyond raw technical specs—allowed certain segments (like microprocessors) to maintain healthier margins even in the face of mounting competition.

Looking ahead, the 1990s would bring another wave of transformation: the Internet’s emergence, the further rise of mobile communications, and the era of deep sub-micron manufacturing nodes. As we continue our journey through semiconductor history, these historical insights form the backdrop for understanding how today’s complex, globally networked industry came to be—and how pricing strategies might evolve next.