Recap

Building on the costly, government-backed semiconductor efforts of the 1950s, the 1960s saw the revolutionary introduction of integrated circuits (ICs), moving beyond discrete transistors to more complex, multi-component chips. The decade was defined by the transition to large-scale manufacturing, supported by advances like the planar process, which significantly improved yields. While early ICs remained expensive, pricing strategies evolved, introducing volume discounts and value-based models. Military and aerospace applications drove early adoption, but by the end of the 1960s, the commercial potential of semiconductors—particularly in computing and telecommunications—was becoming clear.

Introduction

In the 1970s, semiconductors shifted from a niche technology reserved for government and specialized computing applications into mainstream electronic components that began transforming daily life. Building on the success of integrated circuits in the 1960s, semiconductor manufacturers saw the commercial market expand dramatically, fueled by the rise of personal computing, advanced telecommunications, and growing consumer demand for electronic products.

With the new era came new pricing challenges. As manufacturing technologies improved and volumes soared, cost-per-transistor continued its steep decline—a trend that made semiconductors more accessible to a broader range of applications. Yet macroeconomic events, changing trade policies, and intensifying global competition shaped a more volatile market. This article explores how semiconductor pricing evolved amidst both the promise of rapid technological gains and the pressures of a changing global economy.

Global market expansion and intensifying competition

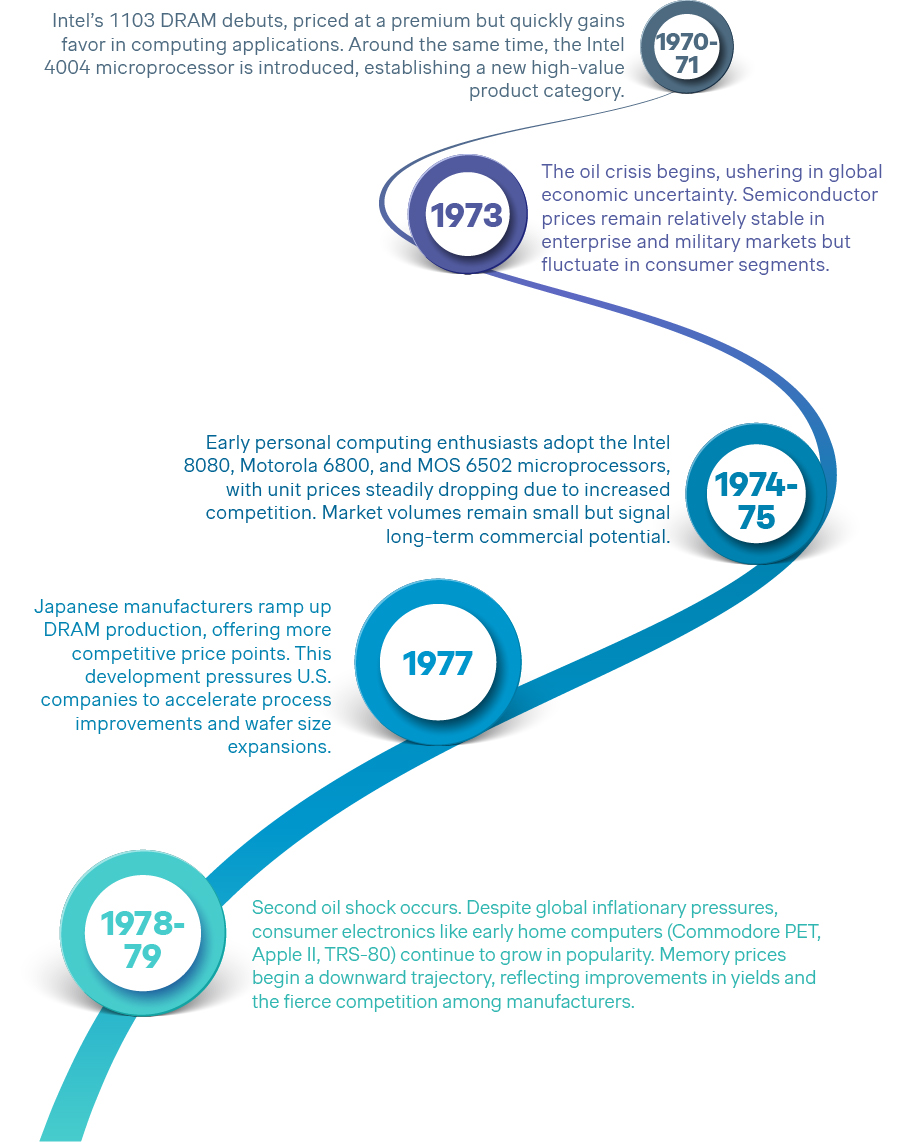

By the early 1970s, the semiconductor industry was no longer confined to a few pioneers in the United States. Japan began to emerge as a formidable player, particularly in the field of memory devices (Dynamic Random-Access Memory, or DRAM). Europe also fostered its own semiconductor ecosystem, with several companies investing in research and production. These global expansions fueled competition and price pressure as multiple regions vied for market share.

Japanese producers

Firms like NEC, Hitachi, and Fujitsu focused on high-volume production of memory chips, undercutting many American counterparts on price. They quickly became known for strong process discipline and manufacturing efficiency, positioning themselves as serious contenders.

American mainstays

U.S. companies—including Intel, Texas Instruments, Motorola, and Fairchild—responded to rising competition by ramping up R&D and expanding production capacity. Memory products such as Intel’s 1103 DRAM (introduced in 1970) gained traction in computing markets, spurring a race to develop higher-density, lower-cost memory devices.

European firms

While trailing behind the U.S. and Japan in terms of scale, European semiconductor manufacturers (e.g., Siemens, Philips) collaborated with national governments to fund R&D projects. This public-private cooperation aimed to keep Europe in the technological race, though pricing in those markets was often higher due to smaller volumes and a focus on specialized products.

Amid intensifying global competition, semiconductor pricing strategies began incorporating sophisticated cost models that considered not just production expense but also currency fluctuations, tariffs, and regional trade policies. Though these factors would escalate further in the 1980s, they were already influencing the market in the 1970s, as cost advantages in one region could quickly erode if currency or trade conditions shifted.

Key technological advancements shaping pricing

The microprocessor revolution

One of the most significant introductions in the 1970s was the commercial microprocessor. Intel’s 4004, released in 1971, packed the core of a central processing unit (CPU) onto a single chip for the first time. This milestone opened the door to an entirely new category of devices—from calculators to industrial controllers to, eventually, personal computers.

Impact on pricing: Early microprocessors were relatively expensive compared to simpler integrated circuits. However, they offered unprecedented value by consolidating complex logic functions into one piece of silicon. Manufacturers could command premium prices at first, but as competitors (e.g., Motorola with the 6800, MOS Technology with the 6502) entered the field, prices trended downward.

Memory density increases

Memory chips, particularly DRAM, saw major capacity jumps through the decade. In 1970, Intel’s 1103 DRAM offered 1 kilobit of storage; by the end of the decade, DRAM chips had grown to 16 or 64 kilobits. This exponential increase in density—mirroring Moore’s Law for logic devices—paved the way for cost-per-bit reduction.

Impact on pricing: As bit density rose, the cost to manufacture each additional bit of memory plummeted, allowing a drastically lower cost structure. Companies that achieved reliable, high-yield production of larger capacity memory devices could offer competitive prices and still maintain healthy margins.

Process node shrinks

Although not as pronounced as in later decades, the 1970s continued the trend of shrinking process nodes (feature sizes). Smaller geometries allowed more transistors to fit on a die, leading to better performance and lower per-unit costs, assuming yields could be maintained. Photolithography techniques advanced, but they also raised capital expenditures for new fabrication equipment.

Impact on pricing: Each successful node shrink typically allowed manufacturers to reduce the die size (and hence material costs) of a given design, but it required significant investment in updated fab technology. Companies with the resources to continuously upgrade their fabs gained a cost advantage, eventually reflecting in product pricing strategies that leveraged economies of scale.

Macroeconomic factors: booms, busts, and shifting trade policies

The oil crises

The 1973 oil crisis and the subsequent 1979 energy shock had global economic repercussions. When oil prices soared, inflation took hold, impacting both consumer demand and the cost structures of technology manufacturers. Electronics production did not slow as dramatically as some traditional sectors, but the uncertainty made pricing less predictable.

Impact on pricing: On one hand, higher inflation and economic turbulence could dampen consumer appetite for discretionary electronics, threatening volumes. On the other, industries such as aerospace, industrial automation, and computing pressed forward, cushioned by government or enterprise budgets. This sector-level divergence affected how semiconductor makers balanced pricing for consumer vs. commercial or defense clients.

Currency fluctuations and trade tensions

As the U.S. dollar’s strength shifted throughout the decade, American semiconductor firms sometimes faced profitability challenges in exports, especially as Japanese yen valuations and European currencies fluctuated. Furthermore, Japan’s industrial strategy promoted large investments in semiconductor capacity, an approach that resulted in surplus production at times—leading to price competition and, in some cases, allegations of dumping.

Impact on pricing: Manufacturers had to account for exchange-rate risk in their pricing, sometimes hedging production or relocating assembly plants to regions with favorable trade conditions. This period foreshadowed more intense U.S.-Japan trade disputes over semiconductors in the 1980s, but the seeds of tension were already planted in the 1970s.

Timeline of notable pricing milestones in the 1970s

Cost structures: from batch to (semi-)automated lines

Throughout the 1970s, semiconductor fabrication became increasingly automated. Although still far from the levels of automation seen in modern fabs, significant reductions in manual handling contributed to better yields and lower costs.

Wafer handling and testing

Automated wafer-handling systems, introduced in the late 1960s, became more reliable in the 1970s. These systems reduced contamination—a critical factor in yield improvement. Meanwhile, automated testing equipment allowed for faster identification of defective dies.

Packaging and assembly

New packaging designs (e.g., plastic dual in-line packages for integrated circuits) simplified assembly. While some aspects of wire bonding and die attachment remained manual, partial automation reduced labor costs and improved consistency.

Scaling manufacturing lines

To meet rising demand, manufacturers built larger fabs, often doubling or tripling capacity. This scaling created economies of scale—particularly as process yields improved—leading to a more pronounced drop in cost per device over time.

These improvements in manufacturing efficiency set the stage for more aggressive pricing. As volumes increased, some companies started to experiment with “learning curve” pricing, intentionally setting lower prices to capture market share, betting that higher volumes would reduce unit costs even further.

Notable pricing models in the 1970s

Premium pricing for emerging products

Microprocessors, in their early years, commanded premium prices because they delivered high value to specialized applications. Likewise, cutting-edge DRAM chips with higher densities than competitors could initially fetch top dollar. Companies that were first to market with advanced chips enjoyed a temporary pricing advantage until rivals caught up.

Commodity pricing for established products

As memory densities matured and multiple suppliers flooded the market, DRAM, SRAM, and certain logic families began to exhibit commodity-like price behaviors. Margins on these products narrowed as competition and volumes soared, leading to frequent price fluctuations based on supply-demand dynamics.

Contract manufacturing and OEM discounts

Major computer and telecommunications OEMs (Original Equipment Manufacturers) secured dedicated capacity and volume-based discounts. For instance, if a large computer firm signed a multi-year contract for a specific microprocessor or memory device, the semiconductor supplier could confidently invest in scaling production, thereby lowering costs and offering preferential pricing. This partnership approach gave both parties predictability in cost and supply.

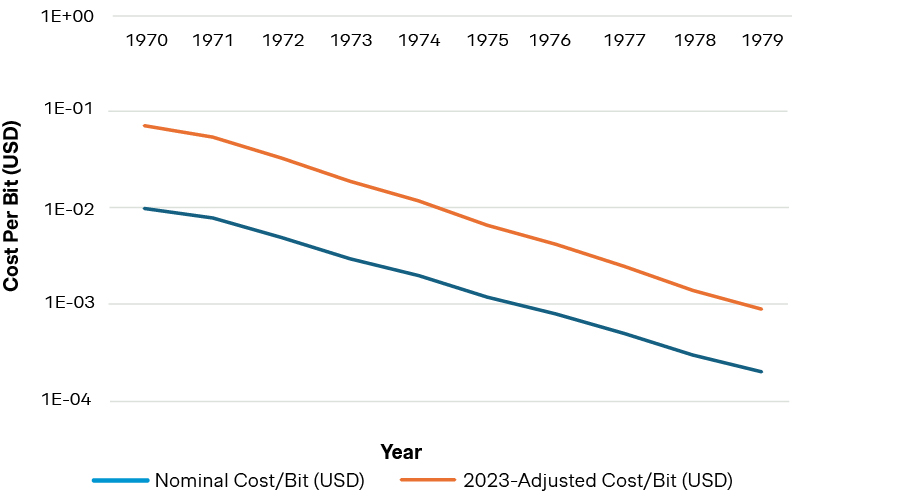

Cost per bit of DRAM (1970–1979)

Figure 1: Different DRAM generations (1K vs. 4K vs. 6K) came to market at different times. The annual data here is a broad average for the "typical" product available in that year, not the newest or the cheapest. Actual contract or volume-discounted prices could deviate significantly from these 'List Prices'

Conclusion: the 1970s—bridging pioneering innovation with widespread adoption

The 1970s stand out as a dynamic period when semiconductors made the leap from specialized applications to mainstream electronics. Propelled by the microprocessor revolution, dramatic improvements in memory density, and broader automation in fabrication, the industry experienced sharp declines in cost-per-transistor. At the same time, macroeconomic upheavals like the oil crises and emerging trade competition—especially from Japan—introduced new uncertainties and pressures.

Pricing strategies evolved in step with these changes. While cutting-edge products such as microprocessors still commanded premium prices, many devices—especially memory chips—began to behave more like commodities. The interplay between technological leaps (yielding cost reductions) and intensifying global rivalry (forcing price competition) laid the foundation for the sophisticated pricing models that would define the next phase of semiconductor growth.

Key lessons

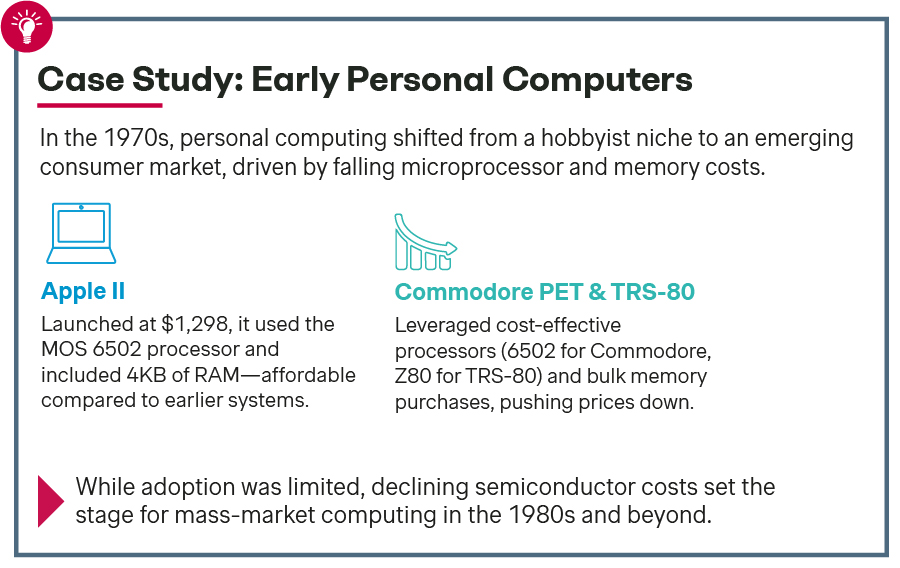

The central takeaway from the 1970s is the power of market forces in driving semiconductors into everyday use. As R&D breakthroughs and large-scale manufacturing lowered costs, previously exclusive technologies found a place in consumer products like calculators, game consoles, and fledgling personal computers. However, this growth also highlighted vulnerabilities to macroeconomic shocks and shifting trade environments. For modern pricing strategists, the 1970s underline the importance of both scaling efficiently and diversifying markets—ensuring that demand is balanced across sectors that are not uniformly exposed to economic downturns.

In the next installment of this series, we will explore the 1980s—a decade marked by further technological refinements, the rise of new device categories, and increasingly competitive global trade dynamics that would forever reshape how semiconductor products were priced and marketed.