Adoption is rising and satisfaction is high among Australian neobanking users. But primary banking relationships remain firmly with incumbents, leaving conversion – not growth – as the real challenge.

Two patterns define Australia's neobanking market: adoption trails global peers, and while customer satisfaction is high, conversion to primary banking relationships is low.

Customers are engaging with neobank – in fact they often prefer the experience – but they're hesitant to rely on them as their main financial institution.

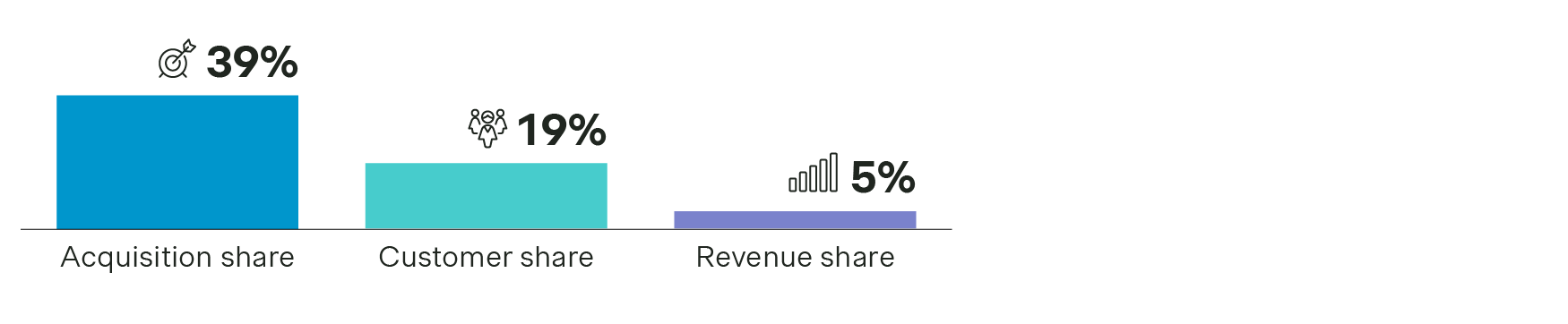

Simon-Kucher's Global Neobanking Study 2026, covering more than 300 neobanks across 16 markets, highlights the broader context. Globally, neobanks now capture 39% of new banking relationships worldwide, hold 19% of all accounts, and generate roughly 5% of global retail banking revenue.

Australia is part of this story, but it is not following the same path. Understanding that difference matters if you're running a bank, building one, or deciding where to compete.

Australia's neobank growth is not converting

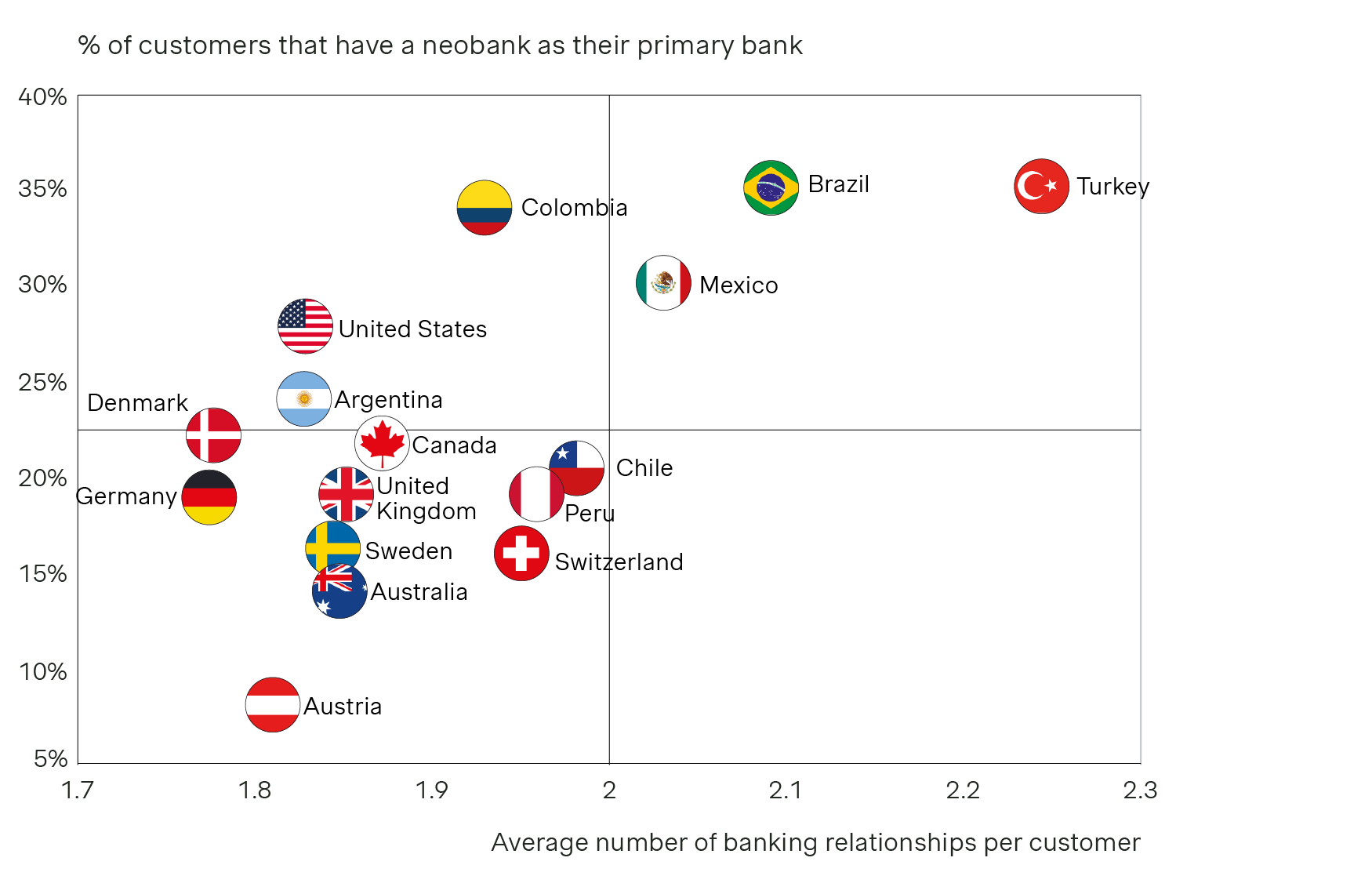

Roughly 60% of Australian consumers report having used a neobank, against 70-80% in comparable markets. More importantly, less than 15% consider a neobank their primary bank – below the global average of 21% and significantly behind Brazil, Colombia, and Turkey, where that figure reaches 30-38%.

Overall, three numbers frame the Australian position:

- Around 60% neobank adoption rate (vs 70-80% globally)

- 14% primary bank conversion rate (vs 21% globally, 35%+ in leading markets)

- Over 60% of consumers anchored to a national bank as their primary institution.

Large national banks still capture close to half of all new banking relationships. When switching does occur, it largely occurs within incumbents.

And yet the underlying demand is stronger than current conversion numbers suggest. 35% of Australian consumers expect a neobank to become their primary bank within the next three years, with a further 32% indicating that is somewhat likely. This is not a market sitting still: primary banking relationships are increasingly in play, but on a timeline shaped by trust and economic considerations than by product preference alone.

Australian neobanks also outperform the Big Four (Commonwealth Bank, Westpac, NAB, and ANZ) on customer satisfaction. The gap, therefore, is structural and behavioral – and it has specific, causes.

The Big Four effect is real and persistent

The Big Four major banks collectively hold institutional trust built over generations, which sets the baseline for what consumers expect from a primary banking institution and how much evidence they require before departing from one.

These incumbents hold structural advantages that are hard to replicate:

- Deep, long-standing customer relationships with integrated credit histories

- Payroll-linked banking and home loan portfolios that anchor customers for decades

- National ATM networks and branch infrastructure which certain customer segments continue to value

Neobanks can outperform on digital experience and pricing transparency, however, they are not yet competing on the same depth of relationship. As a result, primary banking remains concentrated. Customers may experiment with new providers, but their core financial relationship typically stays within the incumbent system.

What makes this dynamic worth watching closely is the acquisition trend. Neobanks now account for 33% of accounts opened in the last 12 months in Australia. This is against 49% for large banks and 19% for regional banks – a meaningful share of new banking relationships as it is the pool from which future primary bank switching will come.

What's actually blocking the banking switch

The study identifies three key barriers that are more pronounced in Australia than in most peer markets.

Stability and trust concerns

Australian consumers are more likely than their global peers to cite doubts about neobank financial stability as a reason not to switch and most recently the closure of a few digital banks (e.g. Xinja, Volt). In a market where incumbents have maintained strong reputations for generations, institutional trust is built differently and not easily transferred.

Cash and ATM access

Limited ATM infrastructure from neobanks is a more significant friction point in Australia than in many other markets where digital-only banking has become the practical default. While this is not a dealbreaker for secondary accounts, it is a barrier when considering a primary banking relationship.

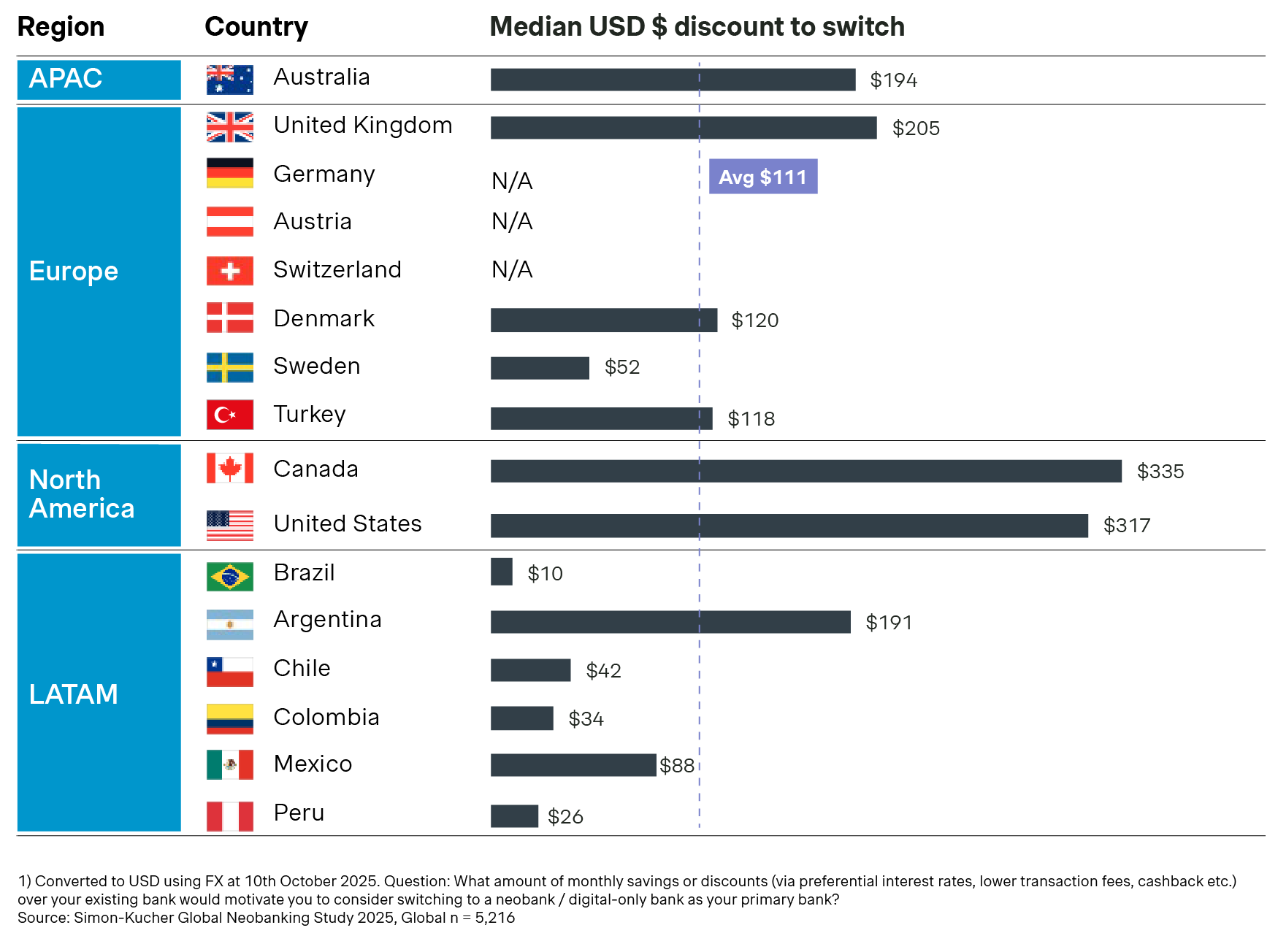

High economic threshold for switching

Australian consumers require a materially higher financial incentive to switch banks. Around half indicate they would need more than AUD 300 per month in benefits – through better savings rates, lower fees, or cashback – to consider moving their primary bank. Globally, the average switching threshold sits around USD 111 per month.

Where Australian neobanks are gaining ground – and where they are not

Neobank product usage in Australia is lower across most categories (lending, current accounts, deposits) compared to other markets. The exception is alternative investments, particularly cryptocurrency, where Australian adoption is closer to global peers. This suggests neobanks are finding a foothold in investment and wealth-adjacent products before they've cracked the core current account relationship.

That's not unusual at this stage. Customers are turning to neobanks for newer, higher-engagement categories, and digital banks are winning where innovation and speed matter most. The question is whether Australian incumbents will respond fast enough to protect those product areas, or whether they'll cede ground gradually.

The digital channel preference data adds urgency to that question. 69% of Australian consumers now say digital is their preferred banking channel, second only to Latin America at 75.7%, and ahead of most European markets. A market where nearly seven in ten consumers prefer digital interaction is not structurally resistant to neobanking. It is a market where the conditions for accelerated adoption are already in place.

The next phase of neobanking in Australia

Our global study frames the Australian position plainly: steady growth, incremental disruption. Australia is not Brazil, where neobanks are reshaping the competitive landscape at speed. The forward-looking data suggests the pace of change is closer than the current conversion rate implies.

Customer satisfaction is a genuine asset for neobanks, but it is not yet a commercial one. Converting that advantage requires competing on financial value: rates, fees, and rewards that consistently meet or even exceed the switching threshold Australian consumers have set.

It's clear that the trajectory in Australia will be defined less by global momentum and more by how quickly trust, infrastructure, and economic value align to support core bank migration.

To discuss what these dynamics mean for your organization, get in touch.

Explore all the insights from our global neobanking analysis

You can also read our US and UK market analyses.