Recent pressure on software valuations – driven in part by investor concerns around AI disruption – has led to more cautious investment behavior and multiple compression across the software industry. The average forward earnings multiple for software companies collapsed from roughly 39x to about 21x in just a few months and the IGV Software Index is already down more than 30 percent from its late-September 2025 peak.

Despite this backdrop, Office of the CFO (OCFO) software remains an attractive area within the broader software landscape, showing greater resiliency compared to the broader SaaS industry. However, capturing its potential requires sharper focus: identifying the right targets demands a nuanced understanding of segment dynamics, and a clear understanding of value creation potential post-acquisition.

OCFO software remains an attractive investment space

The Office of the CFO (OCFO) software market comprises a broad set of solutions supporting core finance processes, including core financial suites (accounting), procure-to-pay, order-to-cash, expense management, CPM and FP&A, close management, tax and treasury, as well as equity management and ESG/compliance.

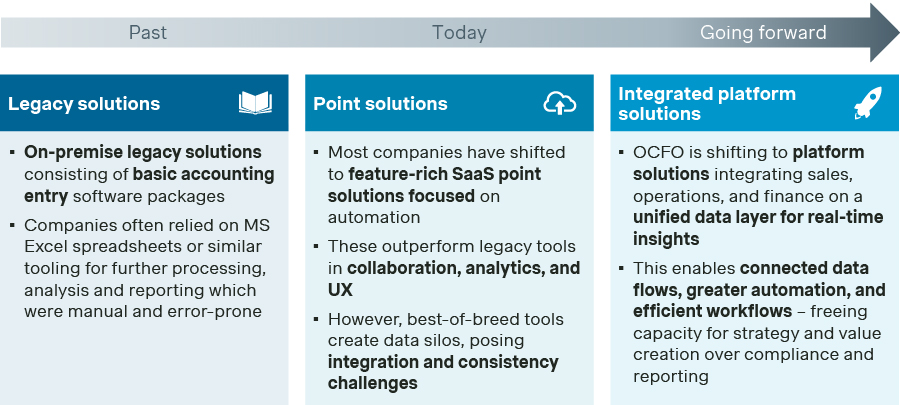

The market is characterized by a mix of specialized point solutions and increasingly integrated platforms, serving micro/small, mid-market, and enterprise customers. As finance teams move away from fragmented legacy systems, demand is shifting toward end-to-end, cloud-based ecosystems that enable more efficient, automated, and data-driven decision-making.

The OCFO software space stands out due to a combination of structural drivers:

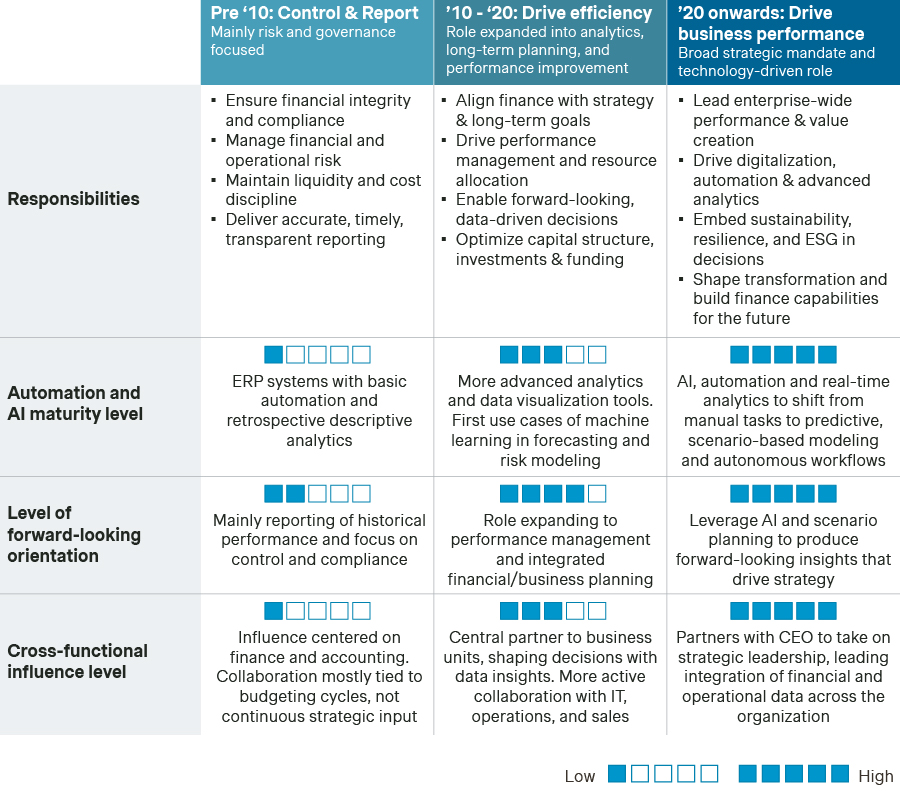

Evolving role of the CFO

The CFO function is expanding beyond financial reporting and compliance toward a more strategic and forward-looking role. This shift increases demand for end-to-end digital workflows, real-time insights, and automation to manage growing complexity and volatility. At the same time, AI, machine learning, and decision intelligence are accelerating the transition toward a more autonomous finance function.

Large and growing addressable market

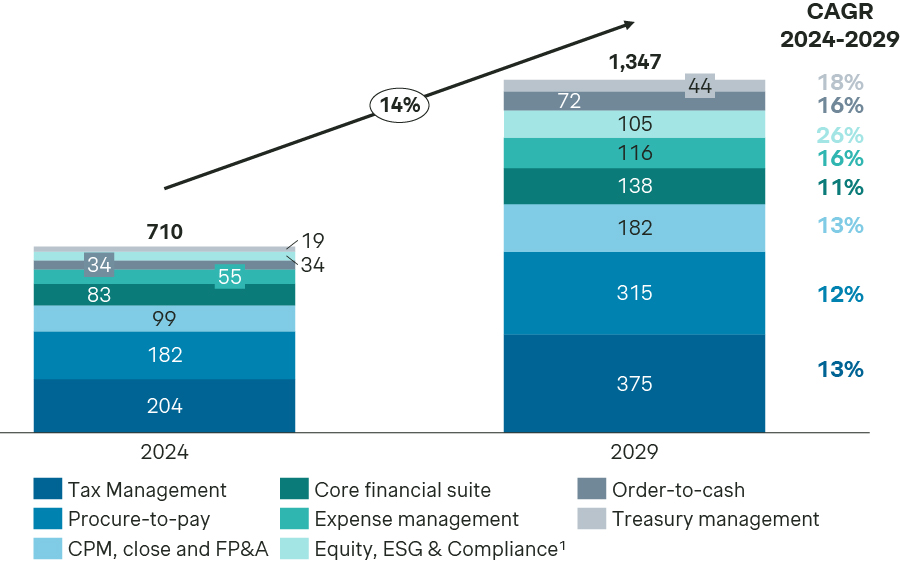

The Dutch OCFO market is already sizeable and continues to grow strongly across multiple subsegments. Areas such as FP&A, tax, spend management, and analytics represent significant growth pools, supported by ongoing digital transformation. At the same time, adoption remains relatively low in several product segments, leaving substantial whitespace across micro/small, mid-market, and enterprise customer segments.

Source: Netherlands OCFO market size estimated by applying NL share of global GDP to Drake Star’s global OCFO market sizing. Base methodology and benchmark by Drake Star; country-level figures are our own estimates.

Sustained demand drivers

Demand for OCFO solutions is underpinned by increasing complexity in finance processes and a continued focus on efficiency and automation. Investment priorities include AI, cloud analytics, and data platforms, with 30-50% of CFOs planning to increase spending. In parallel, regulatory requirements, the need for real-time insights, and evolving workforce expectations are accelerating the shift from manual processes to integrated digital solutions.

Sticky software models

Many OCFO solutions are embedded in mission-critical financial workflows and tightly integrated with core enterprise systems such as ERP, HRIS, and CRM. This deep integration makes the software operationally central and costly to replace, where proprietary and integrated data creates a durable moat and increase switching barriers. As a result, customers tend to exhibit long lifetimes and generate stable, recurring revenue streams.

As leading OCFO providers expand their product suites, they increase the number of use cases and data interdependencies within the platform. This broadening of functionality strengthens network effects and deepens platform reliance, which in turn reinforces customer retention and creates additional cross-sell opportunities.

Fragmented but converging landscape

The market remains fragmented, with many point solutions and regional providers. However, there is a clear shift toward integrated platforms, as customers increasingly prefer unified solutions over fragmented stacks. This dynamic is driving strong consolidation, with platforms expanding into adjacent categories through M&A to build end-to-end ecosystems.

Early-mover advantage

Many micro/small and mid-market companies are still early in their digitalization journey. OCFO software providers that establish early presence – securing data ownership and workflow penetration – are well positioned to become the system of record. Once embedded, displacement becomes unlikely, creating durable competitive advantages.

While these structural drivers underpin the attractiveness of the OCFO software market, benefits are unevenly distributed across segments and players, making disciplined target selection critical.