Most Business Services firms are still selling AI-enabled work through commercial models built for a pre-AI delivery world, primarily by the hour. Yet AI is beginning to expand the commercial toolkit beyond traditional effort-based billing. Simon-Kucher’s Business Services AI Study 2026 explores how the market is evolving, why most firms are creating value faster than they capture it, what the Front Runners are doing differently, and why the firms that adapt their commercial models early are beginning to pull ahead.

Across Business Services, AI is making firms more efficient. Yet for many firms, those gains are not translating into stronger profitability.

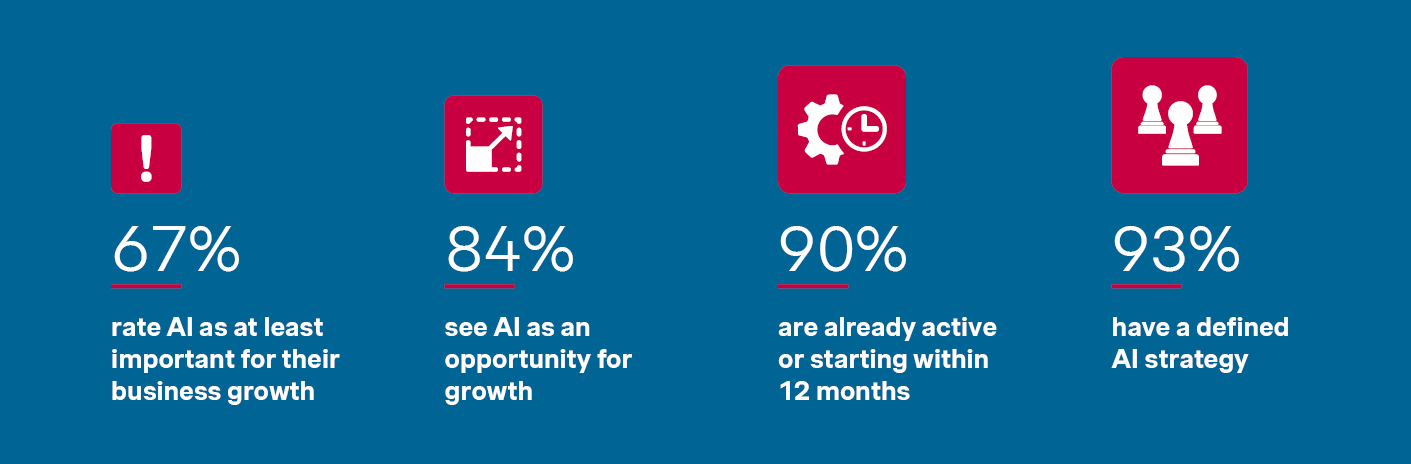

- 90% of Business Services firms are already active with AI – or will be within 12 months

- 93% see AI as a growth opportunity

- 67% already have a formal AI strategy

Adoption is no longer a question.

The commercial debate has barely started.

Across the industry, a structural gap is emerging: AI is improving how work gets delivered faster than firms are adapting how that work gets monetized. Delivery models are becoming more technology-enabled. AI and technology costs are increasingly becoming part of the economics of client delivery. Yet pricing models, go-to-market motions, and sales enablement are evolving more gradually. Most Business Services firms still commercialize AI-enabled work through models built for a pre-AI delivery world, primarily through time-based billing.

This is the era of Services as Software – not because services firms will all become software companies, but because AI is forcing them to expand beyond one dominant commercial logic. And most firms are not ready for it.

This is the era of services as software

This article is the first part of a two-part series. It focuses on the commercial side of the AI shift: how leading firms are rethinking pricing, packaging, and monetization to align with the value AI now creates. Part two will turn to the technical and data foundations that make this commercial transformation possible.

The findings below draw on the Simon-Kucher Business Services AI Study 2026, which surveyed 182 industry leaders between December 2025 and January 2026.

What front runners do differently

Inside the data, one group stands apart. Roughly 18% of respondents qualify as Front Runners – firms with high AI investment, active use of AI as an explicit growth driver, and a clear focus on commercial AI use cases.

These firms are not better at AI in some abstract technical sense. They are better at translating AI into commercial outcomes.

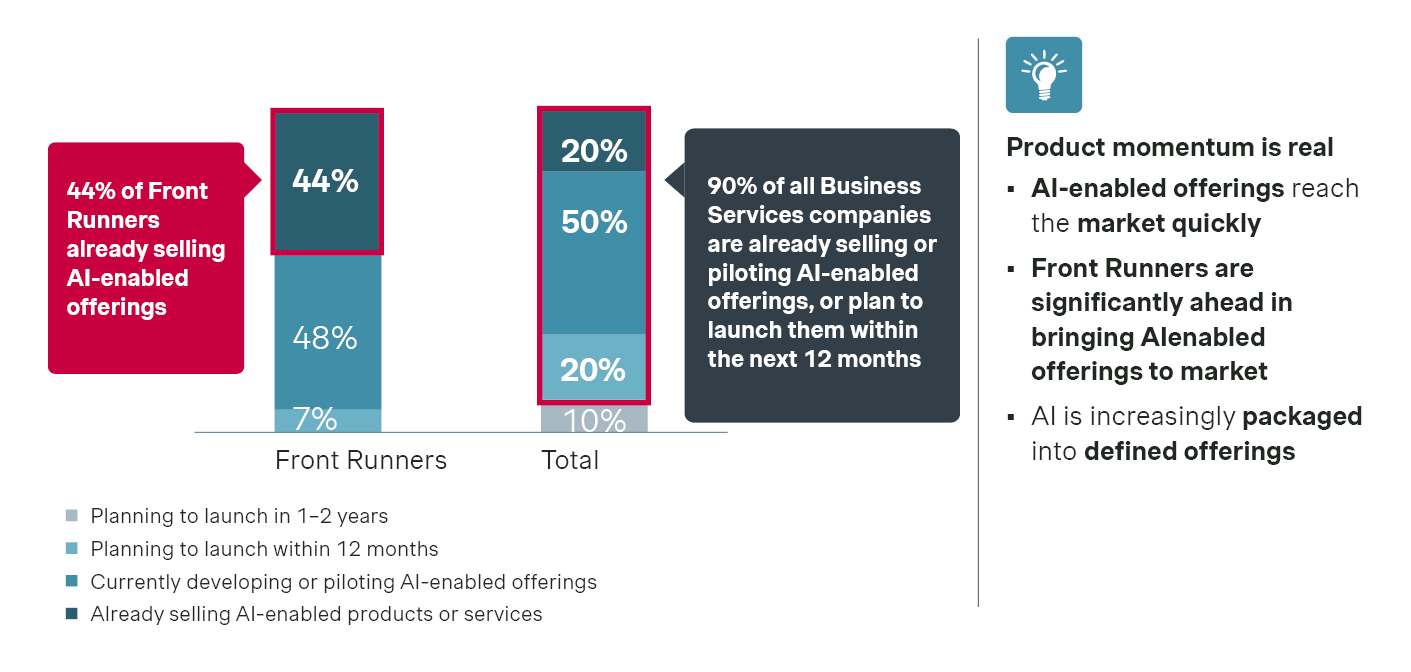

The Front Runner advantage is concrete and measurable. 44% already sell AI-enabled offerings to the market. They are six times more likely to be very confident about achieving their business growth targets. They are expanding the traditional services toolkit with software-like commercial models faster than the rest of the industry.

What Front Runners understand is that AI does not just change how work gets delivered. It changes what clients are ultimately buying.

When work that previously required twenty senior hours can be completed in two, the unit of commercial value is no longer the hour. When AI agents can deliver outcomes that previously required human intervention, the price tag belongs to the outcome, not to the input. This means the billable hour does not disappear, but it loses its monopoly as the default commercial logic.

Front Runners are the firms that have started rebuilding their commercial logic around this reality.

Three structural shifts define what they are doing differently – and they build on each other in a clear sequence. Selectively productizing parts of the service portfolio creates the foundation. That productization makes new pricing logics possible beyond traditional Time & Material billing. And both shifts require – and reinforce – more industrialized delivery underneath them.

Together, these shifts are reshaping how Business Services firms package, price, and deliver value in the Services-as-Software era.

Shift one: from bespoke services to selectively productized offerings

Software companies sell repeatable products. Services firms traditionally sell bespoke engagements. The line between them is beginning to dissolve. Across the broader market, 90% of Business Services firms are either selling, piloting, or planning to launch AI-enabled offerings within 12 months. Among Front Runners, 44% are already selling at scale. Product momentum is real and accelerating.

Yet a closer look reveals an uneven shift. Most firms embed AI inside existing service portfolios rather than building dedicated product plays. AI gets bundled into work that looks like the legacy service, gets priced like the legacy service, and competes like the legacy service – even when the underlying delivery has fundamentally changed. The economics still run through traditional engagement models, and the sales motion still relies on the same expert-led conversations.

Front Runners are breaking this pattern. They separate product economics from service economics. They build dedicated go-to-market motions for AI-enabled offerings. They decide deliberately which AI capabilities should become standalone offerings, which should enhance existing services behind the scenes, and which work best as a combination of both.

Productization creates the conditions for the next shift. Once AI changes what is being sold – from engagement to repeatable output – it also changes what can be priced for, and how.

Shift two: from t&m dominance to a broader pricing toolkit

This is where the gap between value creation and value capture becomes most visible – and where Front Runners are pulling ahead most clearly.

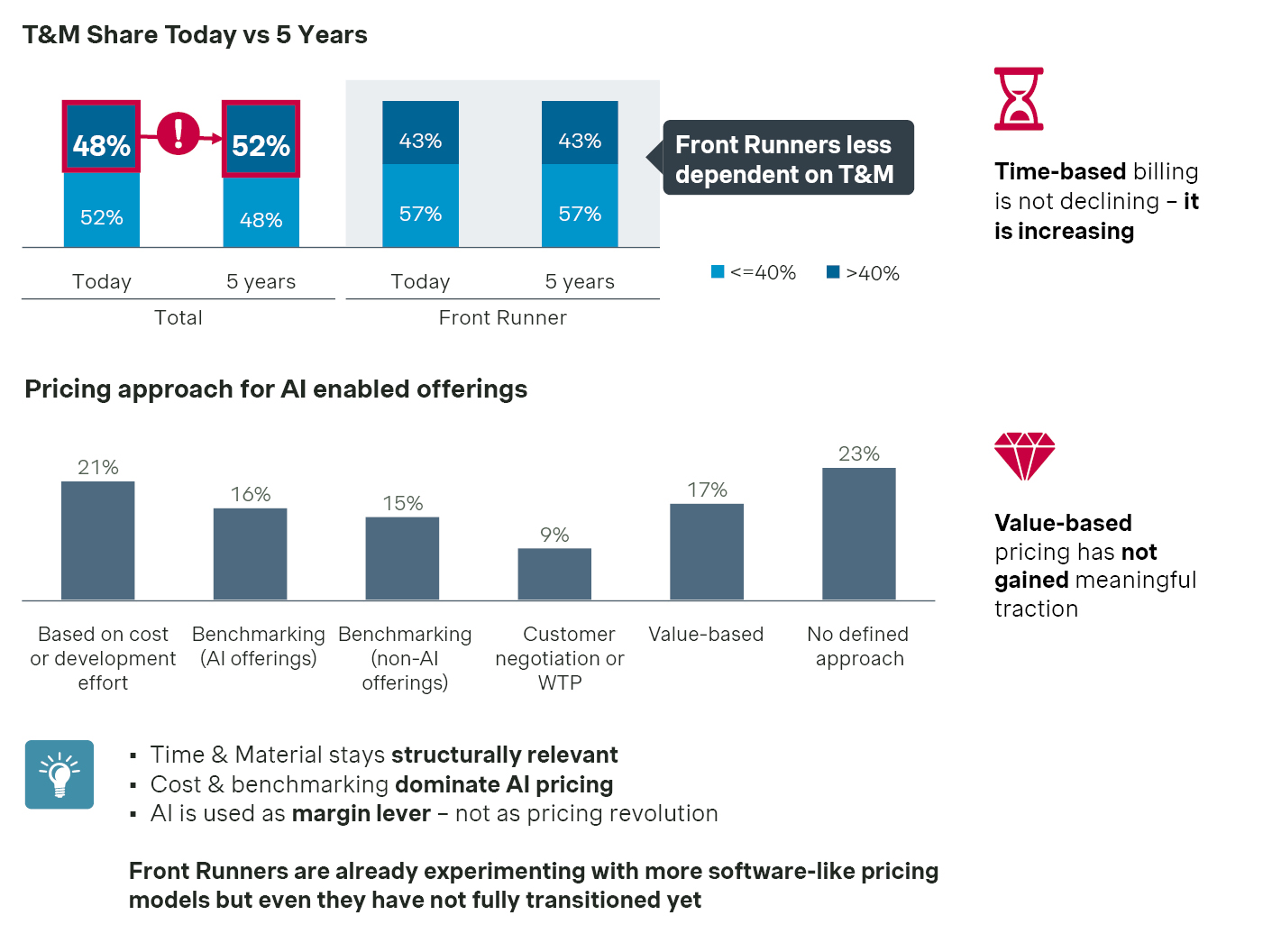

Despite the spread of AI, Time & Material pricing is not significantly declining. Cost-plus models and competitive benchmarking continue to dominate how Business Services firms set prices for AI-enabled work. Value-based pricing has not gained meaningful traction across the broader market.

The reason is structural – and historically familiar. Consider what happened when electronic spreadsheets arrived in the 1970s. Many predicted the end of the accountancy profession. Instead, the industry built a whole new layer of value on top of the new technology, with specialized roles in forecasting, analytics, and decision support.

But the pricing logic of the profession did not change overnight. It took years before firms understood how to charge for the new outputs spreadsheets made possible. The current AI moment in Business Services looks similar. The technology has arrived faster than the commercial architecture around it.

Pricing complexity and insufficient sales enablement are the two largest commercial bottlenecks to scaling AI-enabled offerings, according to the study. Regulatory and integration challenges matter, but they rank lower. The harder challenge is not technical. It is commercial. Most firms have not yet developed the pricing logic, data-driven insights, or client conversations needed to charge for value rather than effort.

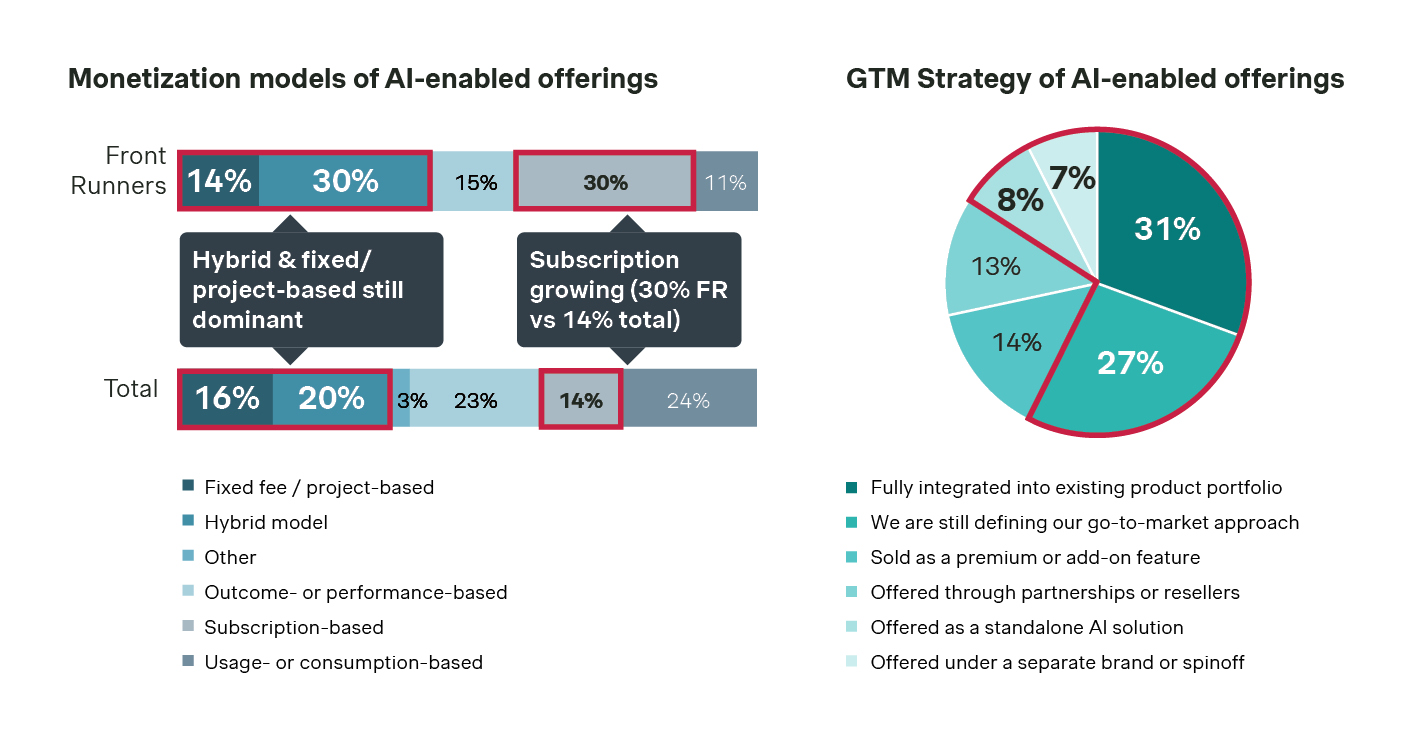

Front Runners are starting to. 30% of them use subscription models for AI-enabled offerings, compared with 14% across the broader market. They are experimenting with hybrid models that combine traditional time-based billing with technology surcharges.

Crucially, they are also introducing new constructs that bridge the old and new logic – the most interesting being the Virtual FTE: an AI-delivered output priced in standardized time increments, the equivalent of an hour of senior analyst work delivered by software. It looks familiar to clients used to T&M billing, but it decouples price from human effort. It is one of the first commercial constructs designed specifically for the Services-as-Software era.

The shift toward value-anchored pricing is emerging first where value is easiest to measure – for example in advisory services, where outcome-based and fixed-output models are gaining real traction. Where AI delivers a clearly defined output – a contract analysis, a tender response, a compliance review – pricing per outcome becomes commercially viable.

Outside these areas, the shift will likely be slower and more selective. The direction is clear, but the right model will differ by service archetype, client context, and measurability of value.

But changing pricing models also creates new operational requirements. Once firms move beyond pure effort-based billing, delivery itself needs to become more measurable, standardized, and scalable.

Shift three: from decentralized to industrialized delivery

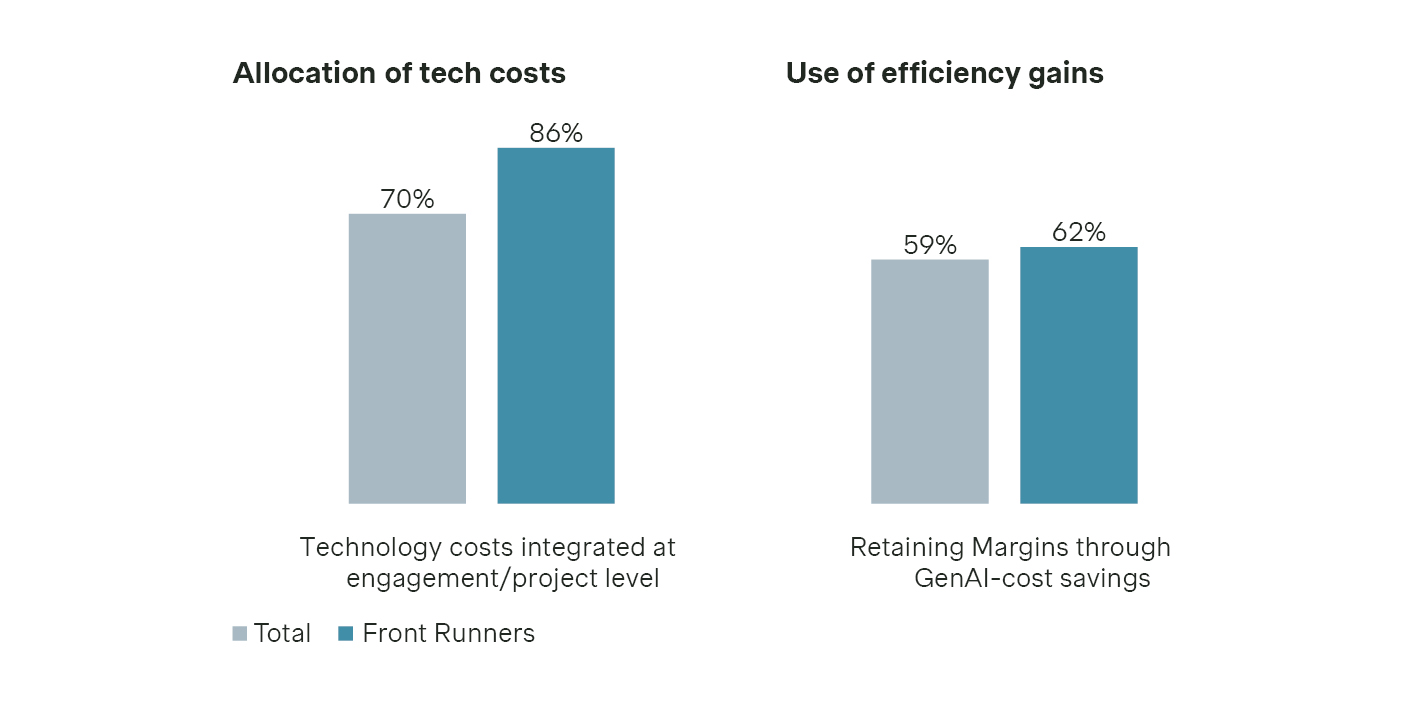

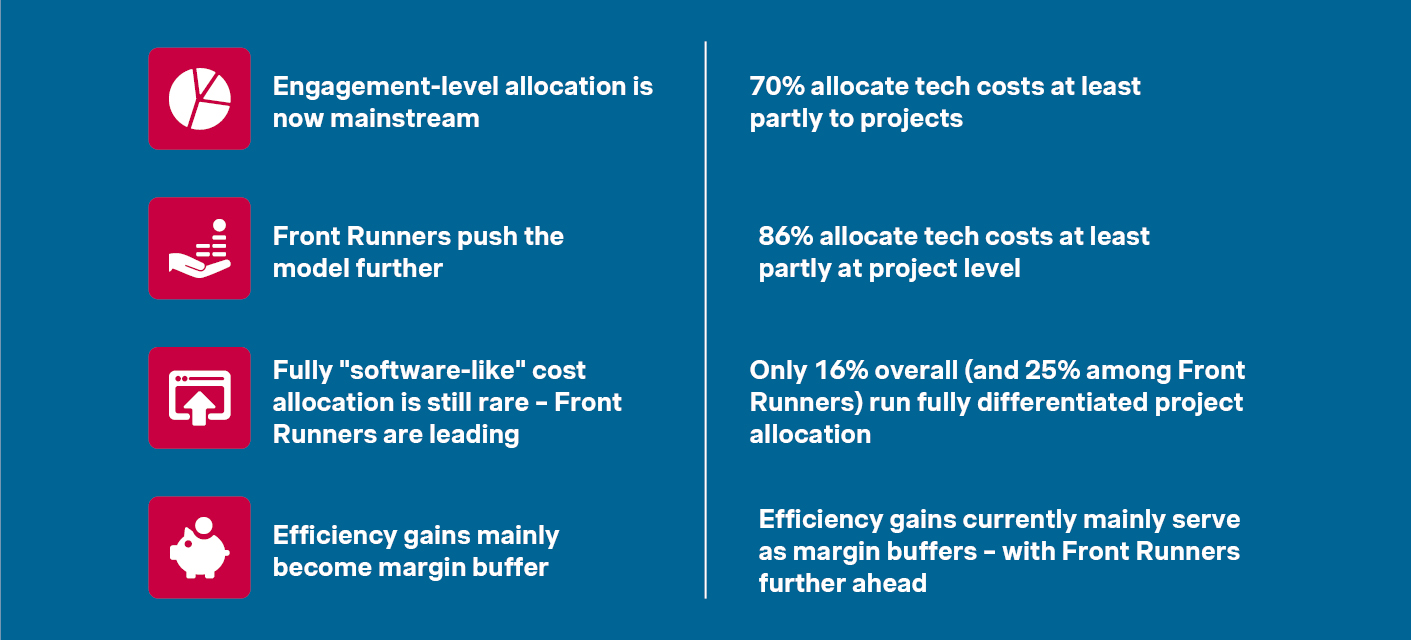

AI is industrializing the delivery of Business Services. The shift becomes visible first in cost allocation: 86% of AI-active firms now allocate technology costs at least partly at the project level. Engagement-level economics are becoming mainstream.

But the shift is incomplete. Only 16% of firms run fully differentiated project-level allocation, where every workflow and every data input is priced into engagement economics with software-like precision. Among Front Runners, that share rises to 25% – still leading the market, but far from a finished transformation.

Most firms have so far used the resulting efficiency gains as a margin buffer rather than a pricing lever. AI reduces delivery time, the savings remain internal, and the client pays the same as before. The firm books the difference as improved profitability. In the short term, this looks like a win.

In the medium term, it is a structural risk. As AI capabilities standardize across the industry, the firms that have not adjusted their pricing to reflect AI-driven productivity will find their margins compressed by competitors who pass some of the gain through to clients – as lower prices, faster delivery, or richer outcomes.

Efficiency gains that stay as margin are not a strategy. They are a deferred reckoning.

Three imperatives for the next 24 months

The three structural shifts described above are not isolated experiments. Together, they point toward a broader transformation of how Business Services firms package, price, and deliver value. For firms that want to move toward the Front Runner group, three capabilities are becoming increasingly important.

Build selectively productized offerings, deliberately

AI-enabled services cannot simply be layered onto existing portfolios without changing how they are positioned and commercialized. Front Runners are making deliberate choices about which capabilities should become standalone offerings, which should remain embedded within broader services, and where hybrid models create the most value. This requires more dedicated product thinking than traditional bespoke services typically demand.

Expand beyond pure effort-based pricing

As offerings become more repeatable and AI changes delivery economics, firms need pricing models that better reflect the value being created. Front Runners are experimenting with subscription models, outcome-based pricing, and constructs such as Virtual FTEs that begin to decouple price from human effort. The goal is not to eliminate Time & Material pricing entirely, but to broaden the commercial toolkit around it.

Industrialize delivery and operational transparency

New commercial models require more scalable and measurable delivery models underneath them. Firms cannot effectively support AI-enabled offerings, subscription pricing, or outcome-based contracts without greater visibility into workflows, technology costs, and delivery economics. Front Runners are therefore investing not only in AI tools but also in the operational infrastructure needed to support more standardized and scalable delivery.

Start now to join the front runners

AI maturity in Business Services is rising fast. Commercial maturity is next on the horizon. The firms that act early are not just catching up – they are building the commercial capabilities, pricing models, and client relationships that will define the next generation of the industry.

AI maturity is rising. Now is the time to build commercial advantage

The next 24 months are the formative period. Front Runners are setting the pace, and the path they are creating is open to anyone willing to start now. The commercial standards of the Services-as-Software era are still being written. The firms that participate early will help shape them.

Part two of this series turns from commercial logic to technical foundation: the data architecture, AI systems, and workflows that make Services-as-Software possible in practice. Commercial transformation ultimately depends on having the right operational and technical infrastructure underneath it.

To discuss how the Services-as-Software shift applies to your firm, reach out to our Simon-Kucher experts.