Diesel volatility is putting growing pressure on logistics margins. When fuel surcharge mechanisms fall behind market reality, even profitable contracts can come under strain. Our experts analyze how better fuel floater design can strengthen cost recovery and support more resilient pricing.

Geopolitical shocks

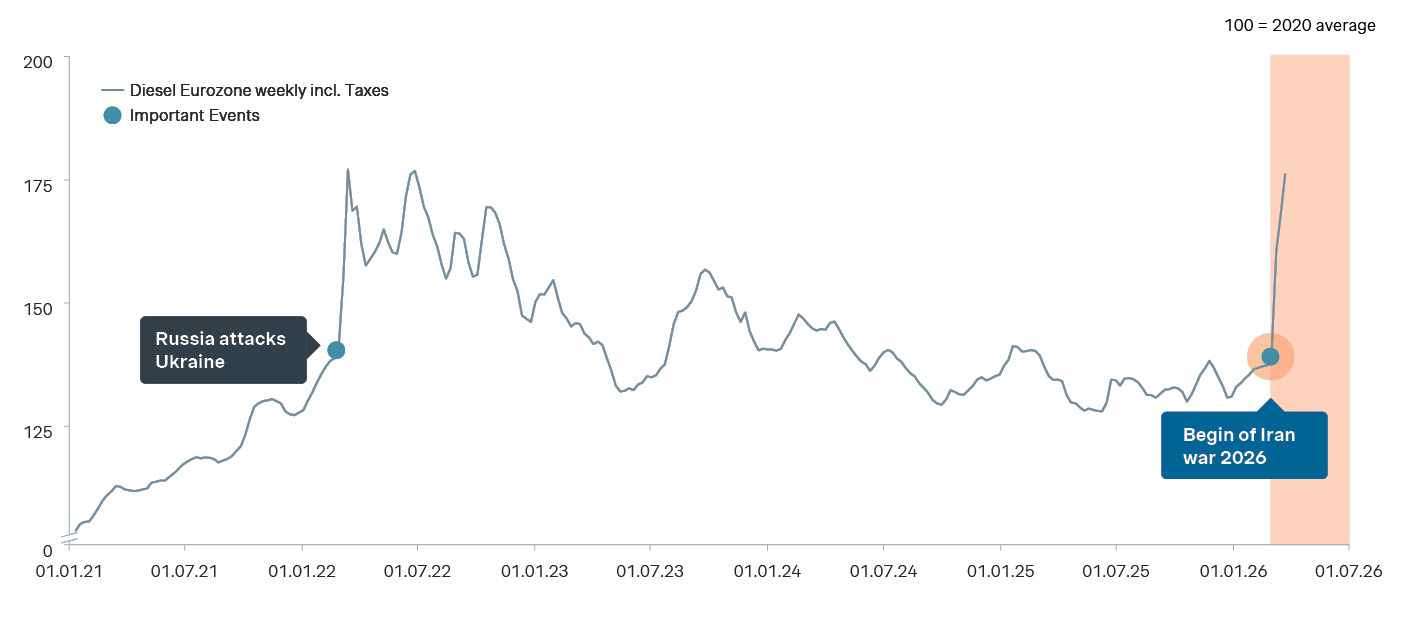

In early 2026, the escalation around Iran shifted the Strait of Hormuz from a distant geopolitical risk into an immediate commercial reality for logistics providers. What had previously been monitored primarily as a supply-side threat now translates directly into higher fuel costs, disrupted flows, and repricing pressure across global logistics networks.

This dynamic is not unprecedented. European Commission showed how quickly geopolitical shocks like the invasion of Ukraine in 2022 can translate into structurally higher energy and transport costs across Europe.

Eurozone Diesel Price Development Since 2021 (Indexed Price Level, 100 = 01.01.2021)

The margin impact of rising diesel cost

Diesel price inflation is not merely an input-cost issue. In road freight, it has immediate earnings implications because for most logistics companies, fuel represents a large share of the cost base while margins remain structurally narrow.

On average, fuel accounts for around 25% of total operating costs in road freight, while operating margins of roughly 5% are generally considered the standard in the sector. At the same time, the European market data from early 2026 show how quickly this cost base can deteriorate: the average diesel price in Europe rose by about 34% within 12 weeks, from 19 January to 13 April 2026.

Under these conditions, the margin impact is immediate. If a logistics provider operates with a 5% margin, has a 25% fuel cost share, and cannot pass through a diesel price increase of roughly 35%, total costs rise by about 7.5%, which pushes the margin from +5.0% to roughly -3.3%. In practical terms, a business that had been profitable would move directly into loss within a very short period.

The core problem shifts from volatility to asymmetry between cost movement and price adaptation. Where that asymmetry persists, diesel inflation ceases to be a pass-through item and becomes an earnings transfer from the logistics provider to the customer.

Why current diesel commercial models are often inadequate

It is precisely at this point that the weakness of many existing floater models becomes visible. In periods of limited diesel-price movement, even imperfect mechanisms may appear sufficient, because the gap between actual fuel cost and contractual recovery remains relatively small. However, once volatility increases, these deviations become economically material, and the limits of the model are exposed.

In practice, the shortcomings recur in a familiar pattern: fixed surcharges no longer reflect actual market development; quarterly or even monthly adjustment intervals are too slow relative to price movements; and the calculation logic often correlates imperfectly with the provider’s real cost trajectory. Under such conditions, the floater remains contractually present but becomes economically ineffective.

The consequence is straightforward. A floater that is static, delayed, or weakly calibrated does not stabilize margin. It merely delays the recognition of under-recovery. Many legacy mechanisms were designed for a lower-volatility environment and are no longer fit for current market conditions.

The ten design questions

If diesel inflation cannot be absorbed operationally and current surcharge models no longer track the cost base adequately, the relevant commercial lever is the redesign of the fuel floater itself. The floater should not be treated as a secondary clause appended to the transport agreement. It is a core pricing mechanism that determines how fuel risk is measured, allocated, and recovered over time.

The redesign task can be structured around ten questions:

1. Overall objective: Is it possible to make a profit from the mark-up? Or is it solely intended to cover the costs? This decision has a fundamental impact on design.

2. Adjustment frequency: Should prices be adjusted monthly or quarterly? In volatile markets, quarterly logic can create too much delay and therefore a margin risk. More frequent benchmark-based adjustments reduce lag between cost movement and recovery – but also customers’ cost predictability.

3. Reference period: Which period should be used as the basis for calculation: previous month, first week of the month, or another fixed window? The longer the timeframe and the further back in time, the greater the risk as prices rise.

4. Reference index: Which external benchmark should be used? The index must be transparent, credible, and accepted by both parties. While international indices are the most transparent, they may be irrelevant at a local level, particularly when governments exert political influence.

5. Price basis: To which price element should the floater apply: base freight only, or freight plus surcharges? This point can materially affect earnings and must be clearly defined. Research on freight pricing and surcharge methodologies shows that price construction and surcharge application differ materially across contracts and carrier types.

6. Base value: Should there be one standard base value for all customers, or individual starting points? A uniform base supports standardization but can entail significant migration effort if there are many individual solutions in place.

7. Transparency: Should the model be published openly or only used in customer discussions? Transparency can improve acceptance, but it reduces the possibility of finding individual negotiated solutions.

8. Mechanism: Should the floater be linear, progressive, or degressive? Symmetric or asymmetric? Linear models are simple and transparent. Other models may be applied to better reflect extreme risks (progressive) or low pricing power (degressive). Where possible, an asymmetric approach (faster upward adjustment, delayed downward adjustment) could also be considered.

9. Caps and floors: Should limits be built into the clause? These can make negotiations easier, but they also shift part of the risk back to the carrier. This must be a conscious commercial choice.

10. Rollout to existing customers: How should this new logic be introduced into the current customer base? While immediate consistency is ideal in some cases, staged migration might be necessary if the change is too drastic.

Conclusion

Fuel volatility is no longer an exceptional disturbance that can be handled through ad hoc re-pricing. It has become a recurring feature of the transport market and therefore needs to be addressed through permanent commercial logic rather than temporary negotiation.

This has two practical implications. First, fuel clauses need to be assessed with the same discipline as core rate design, because small weaknesses in calculation logic can accumulate into material earning leakages across a contract portfolio. Second, standardization has become a strategic advantage. Companies that define a clear and robust floater model improve not only cost recovery, but also internal governance, customer communication, and pricing consistency.

The decisive issue, then, is not whether diesel prices will remain volatile. It is whether logistics providers treat fuel risk as a structural pricing question. Those that do will be better positioned to protect margins under changing market conditions. Those that do not remain exposed to recurring profitability shocks.

To discover how you can respond with more effective pricing mechanisms and commercial strategies, connect with our experts today.