Clinical Decision Support (CDS) is reshaping diagnostics strategy. As momentum builds, the question for manufacturers is how to invest with discipline, capture growth, and long-lasting value.

Key takeways

Clinical Decision Support (CDS) is quickly becoming a strategic priority for healthcare manufacturers, but successful investment is complex.

Barriers mirror those seen in other digital health innovations, including integration challenges, unclear ROI, and stakeholder misalignment.

Manufacturers acting decisively on CDS stand to gain competitive advantage and reinforce long-term portfolio value.

A structured decision framework helps clarify whether to build, buy, partner, or walk away from an investment approach.

Why Clinical Decision Support has become a strategic priority for manufacturers

Persistent budget pressures, repeated reimbursement cuts, and a growing shortage of skilled staff are squeezing resources. At the same time, demand for faster, more accurate, and more integrated diagnostic services continues to rise. The result is a widening gap between operational capacity and clinical demand. How can labs and providers sustain quality and speed as the divide grows?

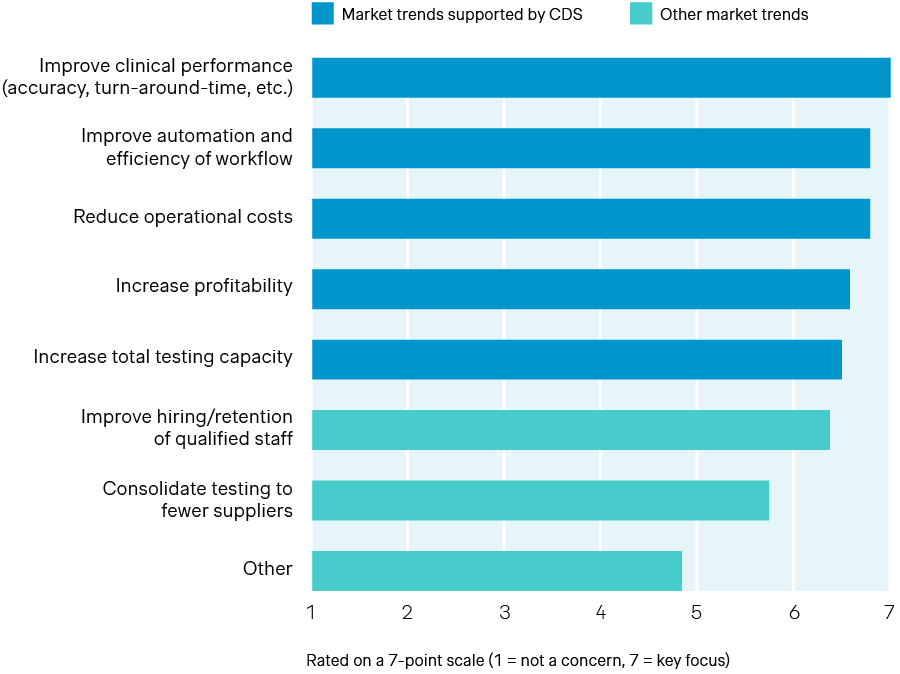

Our global survey of lab directors and leading manufacturers highlights both the urgency of these pressures and the growing appetite for solutions that can help bridge the gap. The findings reveal top strategic priorities for the next 12 to 24 months, ranging from improving clinical performance and boosting workflow automation/efficiency to reducing operational costs. Many acknowledge that the key challenge for labs is achieving these goals effectively amid persistent financial and operational constraints.

What is Clinical Decision Support (CDS)? |

|

Against this backdrop, CDS solutions have become central to many of the innovations transforming diagnostic services today. From improving automation and efficiency to enhancing clinical performance, Clinical Decision Support tools are increasingly embedded across diagnostic workflows. By providing actionable insights at the point of interpretation, CDS can ease workload pressures, streamline complex diagnostic pathways, and enable faster, evidence-based decisions that ultimately improve both operational and clinical outcomes. These capabilities directly support the strategic priorities labs are focusing on over the next 12–24 months, as shown below.

Strategic priorities for labs over the next 12–24 months

Source: Simon-Kucher Global IVD Trend Study 2025

Investment plans clearly reflect this shift. Over half of labs surveyed plan to adopt CDS within the next two to three years, and they rank it among the technologies expected to have the greatest impact over the next four to five years. Integrated CDS features already influence procurement decisions, with an average importance rating of 3.4 out of 5.

CDS offers big opportunities, but the investment journey is anything but simple

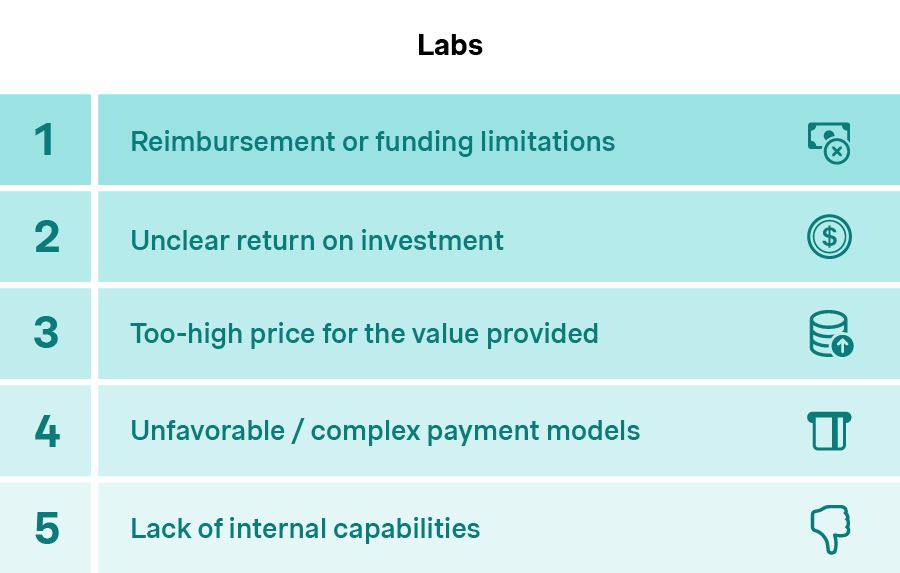

Our analysis across 165 data points reveals a consistent interest in diagnostic innovation. It also highlights meaningful differences in the barriers across stakeholder groups when adopting and commercializing new solutions such as CDS.

Top perceived barriers to diagnostic innovation

For labs, funding uncertainty dominates the landscape. Reimbursement limitations, unclear return on investment, and perceived misalignment between price and value are the primary obstacles to adoption. Tight budgets limit flexibility to absorb upfront investments without near-term operational or financial payback. Even when CDS promises efficiency or quality gains, uncertainty around who pays and how quickly benefits materialize can stall decision-making. Complex payment models and gaps in internal digital capabilities further slow implementation, particularly for labs without strong IT or data science resources.

Source: Simon-Kucher Global IVD Trend Study 2025

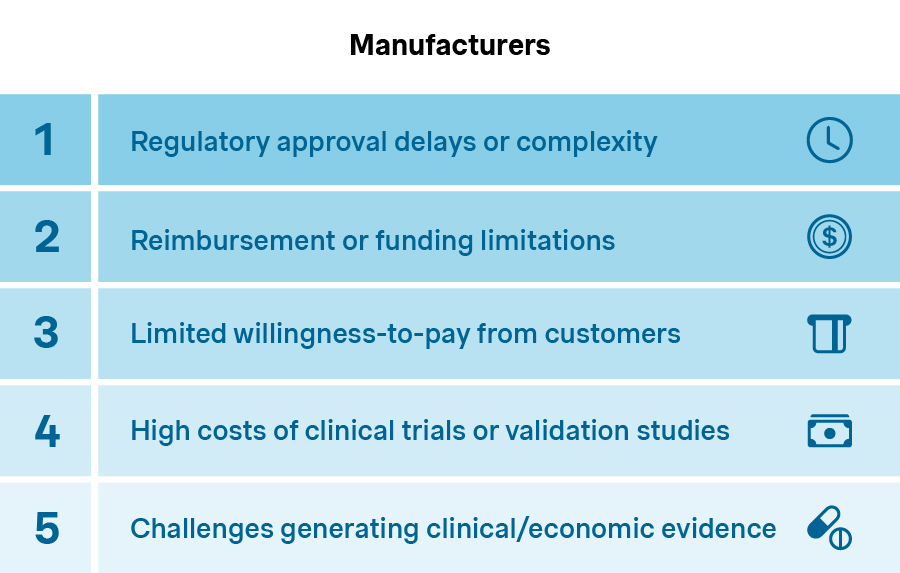

Manufacturers face a different set of constraints. Regulatory timelines and approval requirements are the most frequently cited hurdles, closely followed by reimbursement and funding uncertainty. Commercial realities add further pressure, including customers’ limited willingness to pay, high clinical validation costs, and the challenge of generating credible clinical and economic evidence. These factors make CDS investments capital-intensive and long-cycle, with value realization often dependent on external stakeholders such as regulators, payers, and healthcare providers.

Source: Simon-Kucher Global IVD Trend Study 2025

CDS sits at the intersection of software, clinical evidence, and reimbursement, and inherits the frictions of all three. Adjacent fields such as companion diagnostics and cell and gene therapy testing show how heterogeneous funding pathways, evolving policy linkages between tests and therapies, and reimbursement gaps complicate go-to-market strategies. For CDS, the strategic rationale may be compelling, but value proof, monetization logic, and route-to-revenue design ultimately determines product scale.

Manufacturers and lab stakeholders are shifting their thinking on CDS

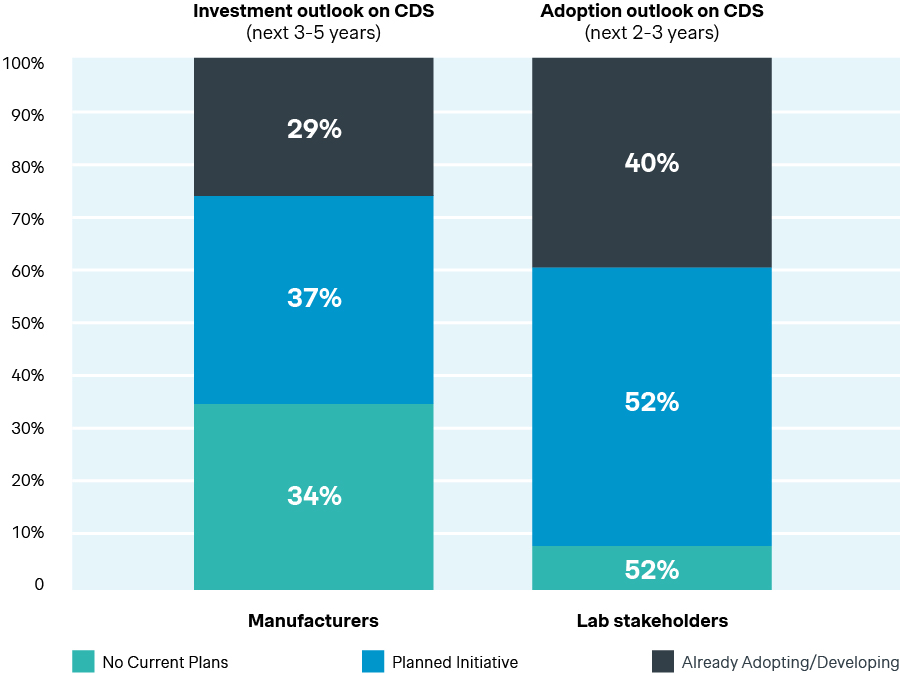

Market behavior is catching up with the narrative. More than a quarter of manufacturers already list CDS among their main technology investment areas, and a clear majority report increasing annual investment in new diagnostic solutions overall. Within that, nearly half plan to invest more in CDS over the next two to three years.

Today, 29% of manufacturers are actively developing CDS and a further 37% have earmarked it for future investments. The primary drivers behind this interest are operational efficiency, cost savings, and improved clinical decision-making and patient outcomes. Broader momentum in AI around healthcare and diagnostics makes the timing for CDS adoption increasingly compelling, positioning it as a core portfolio priority rather than just a “nice-to-have”.

Investment and adoption outlook on CDS

Source: Simon-Kucher Global IVD Trend Study 2025

While manufacturers are ramping up investment, labs are already preparing to act. 52% plan to adopt CDS within the next two to three years, making it the most frequently planned emerging technology in our survey. They also expect CDS to be among the most impactful technologies over the next four to five years. Near-term commercial implications are also already visible. Over 40% of lab directors report that integrated CDS capabilities has a high influence on purchasing decisions for diagnostic or imaging solutions. That influence tilts tenders toward suppliers who can demonstrate credible, integrated decision support and the operational readiness to implement it.

Demand and supply are converging, with customers preparing to use CDS as suppliers scale development. The winners will be those who convert this alignment into value proof and scalable commercial models fastest.

A structured framework helps manufacturers assess CDS opportunities

While enthusiasm for CDS is high, not all manufactuers are convinced. Roughly one-third of manufacturers still have no current plans to invest. Leadership teams therefore need a more nuanced structure to decide where CDS truly makes sense and where it does not.

Clarity typically comes from assessing two factors: Is the opportunity/use case attractive for us, and are we ready to deliver? Examining both opportunity and readiness across internal capabilities, customer and market demand, and competitive dynamics creates a balanced, objective view.

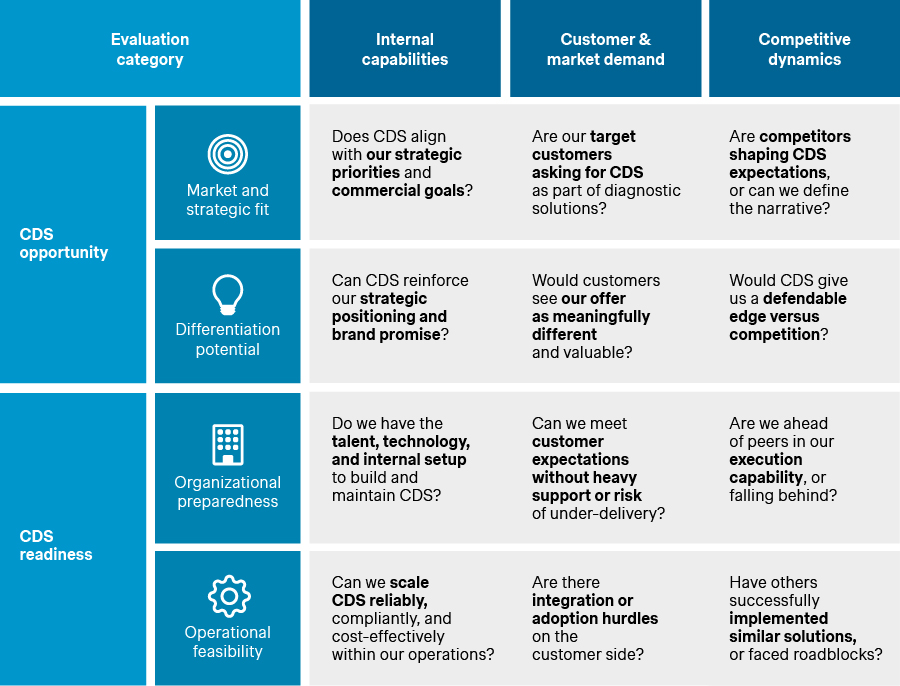

Four evaluation criteria help make the discussion concrete: market and strategic fit, differentiation potential, organizational preparedness, and operational feasibility. To form a balanced view, these criteria should be considered through three complementary lenses, covering internal capabilities, customer and market demand, and competitive dynamics. This helps clarify what the company can deliver, what the market will value, and how defensible the position is versus alternatives. Taken together, this provides a practical way to evaluate whether a CDS opportunity is attractive, whether the organization is ready to deliver it, and where the key risks or gaps lie. The result is a clear CDS opportunity-risk profile that helps align stakeholders without forcing premature commitment.

CDS evaluation framework: What to assess and key questions to ask

Source: Simon-Kucher Global IVD Trend Study 2025

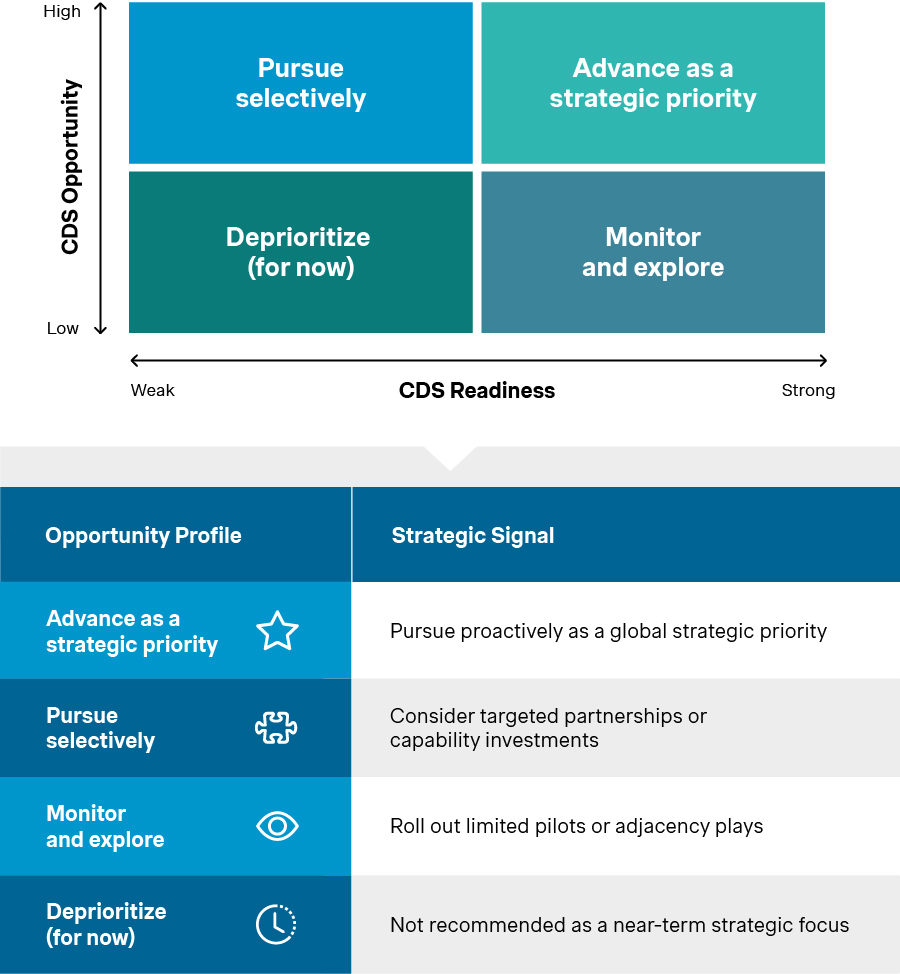

Plotting use cases on the opportunity and readiness axes yields four profiles. These reflect distinct strategic postures, ranging from “Advance as a strategic priority” to “Deprioritize (for now)”. Each carries different levels of urgency, investment, and risk tolerance. The framework becomes the bridge between strategy discussion and execution planning. Its purpose is not to force a decision, but rather ground it in clarity and confidence.

CDS opportunity profiles

Source: Simon-Kucher Global IVD Trend Study 2025

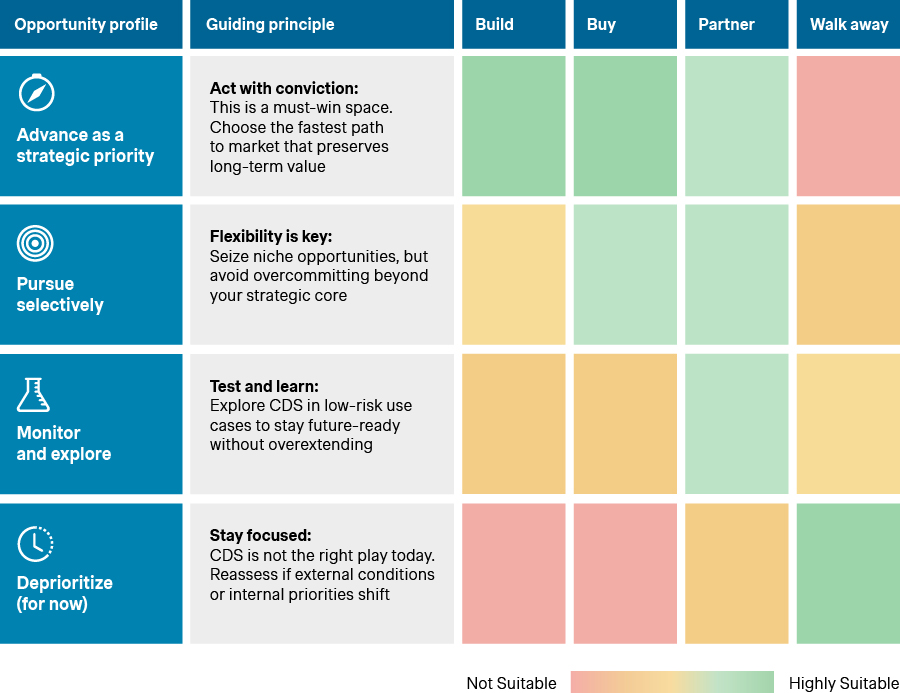

Choosing the right CDS strategy means deciding whether to build, buy, partner, or walk away

The evaluation should culminate in a clear strategic choice, not a one-size-fits-all doctrine:

Build when the strategic fit is high and you have (or can assemble) the necessary capabilities. This path allows you to retain roadmap control and align CDS development closely with your existing portfolio and installed base.

Buy when the business case is strong but internal capabilities or time-to-market are limiting factors. Acquisitions or acqui-hires can accelerate development and reduce technological risk.

Partner when you hold part of the puzzle, such as customer access, data, or brand credibility, but require complementary assets or expertise. Partnerships can create early lighthouse successes and pave the way for deeper integration later.

Walk away when either the opportunity or readiness is low. Protecting focus and capital is often the most strategic decision a company can make.

Across all paths, success depends on translating strategy into execution. That includes a clear value narrative, a monetization architecture that customers understand and accept, and an operating model built for software-enabled delivery.

CDS evaluation framework: What to assess and key questions to ask

Source: Simon-Kucher Global IVD Trend Study 2025

How we help manufacturers convert CDS strategy into measurable success

Delivering results requires commercial engineering equal to product engineering. At Simon-Kucher, we support manufacturers by using the opportunity and readiness framework outlined in this article to guide the full CDS journey. Apart from assessing opportunity and readiness, we apply the framework to define strategic pathways and business cases as well as shape monetization models and go-to-market execution.

This approach goes beyond helping teams decide whether to invest. It provides a pragmatic way to develop, position, and commercialize CDS solutions, ensuring that clinical, operational, and economic value are built in from the start.

How Simon-Kucher supports across the CDS strategy journey

Source: Simon-Kucher Global IVD Trend Study 2025

Effective value capture often depends on deliberate offer architectures. For example, platforms designed with modular capabilities and flexible monetization approaches aligned to demonstrated clinical and economic value. As CDS becomes increasingly integral to diagnostic interpretation, we help teams plan the evolution from transactional pricing toward outcome-based constructs that reward measurable results.

This is why strategy and operations must be designed in tandem. Innovative revenue models can create meaningful value for customers and sustainable economics for suppliers, but only when the value proposition, pricing logic, contracting setup, and go-to-market systems are designed together. That is the difference between a promising CDS roadmap and a scalable growth engine.

Thanks to contributions from Roman Leonard Mueller!