Great deposit marketing doesn’t have to mean higher rates

Most banks reach for interest-based promotions when they need deposits. This approach works, but it’s expensive, hard to sustain, and tends to attract exactly the wrong kind of customer.

Smarter marketing doesn’t just buy deposits. It builds relationships and drives both growth and retention without giving away margin.

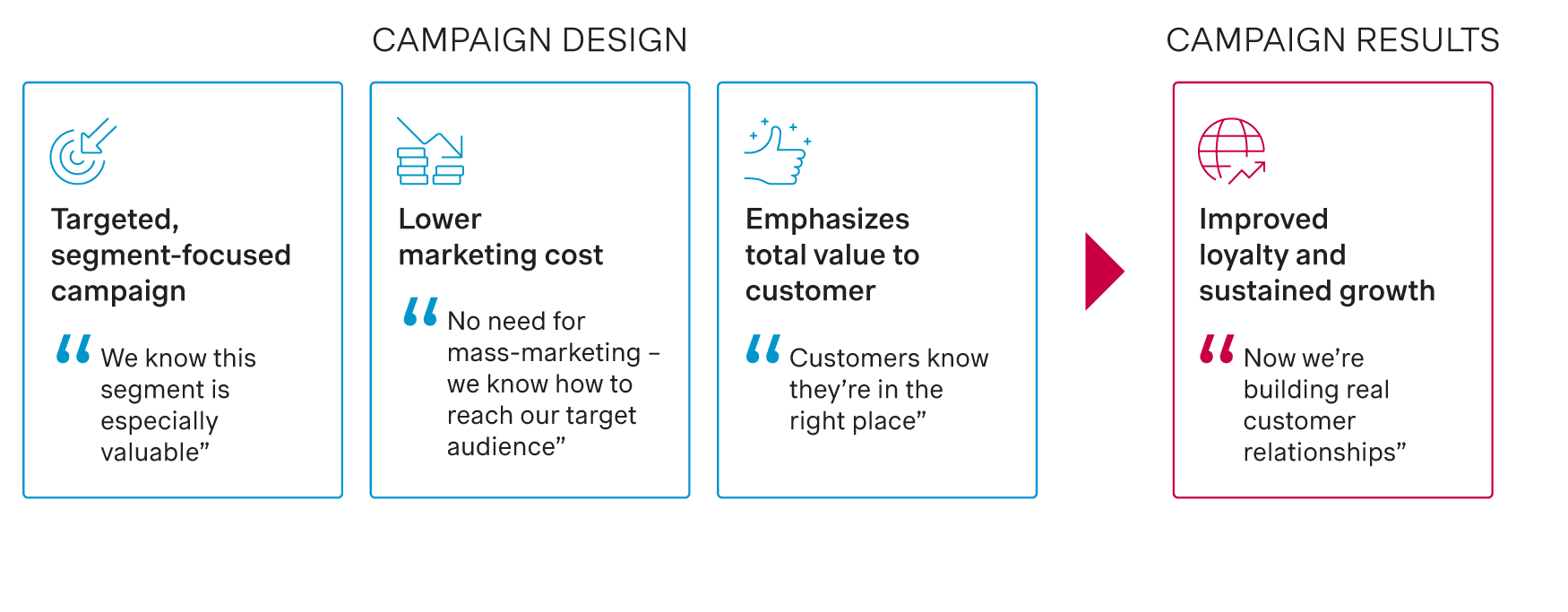

What successful deposit growth really looks like

Less spend, more stickiness. Real results.

When targeting and coordination come together, the numbers can shift.

- 20–25% improvement in ROAS through sharper targeting.

- 12–18 bps NIM uplift by pulling back on blanket promotional rates.

- Stronger retention among promo-activated customers through smarter follow-up engagement.

- Higher cross-sell via coordinated campaign design that turns one-product customers into multi-product relationships.

The problem with “rate-first” marketing

Volume without loyalty drains value.

Rate-centric campaigns can fill the books, but they tend to bring in customers who vanish the moment the promo ends. Promotions frequently run in silos, creating disconnect from pricing teams and frontline channels. This may result in misaligned campaigns, poor ROI, and bloated interest expenses.

The fallout is predictable: higher cost of funds, lower retention, and marketing budgets that never quite translate into profit.

Project example: A leading bank relied on top-of-market promotional rates for years to attract deposits. After trialing mid-market campaigns, acquisition volumes remained virtually unchanged. The real driver turned out to be brand presence; the premium rates had simply been giving away margin for no incremental benefit.

Bottom line: You’re overpaying for customers who won’t stick around.

What smarter deposit marketing looks like

Personalized, purposeful, and profit driven.

Smarter marketing is precise. It starts with who you want to attract and works backwards into how you keep them.

Key ingredients:

- Target your highest-value customers: Segment by behavior, lifetime value, or product mix. Ally Bank, for instance, runs campaigns focused specifically on customers approaching retirement, a segment with outsized deposit potential. See Ally’s campaign example.

- Integrate across channels: Campaigns need to connect with CRM, digital, and the front line. When these run independently, value leaks at every handoff.

- Test and learn constantly: A/B campaigns, control groups, and conversion tracking. Without measurement, marketing remains a cost line instead of becoming a data asset.

- Sell the total value, not just the rate: Convenience, loyalty rewards, and relationship benefits. Commerce Bank, for example, promotes saving for a child’s future, tapping a life-stage goal rather than competing on bps. See Commerce Bank’s ad.

Example: Banks can offer bonus interest exclusively for balances above a customer’s prior 90-day average, or to customers who bundle checking and savings. Taking this approach benefits the financial institution by rewarding growth instead of churn.

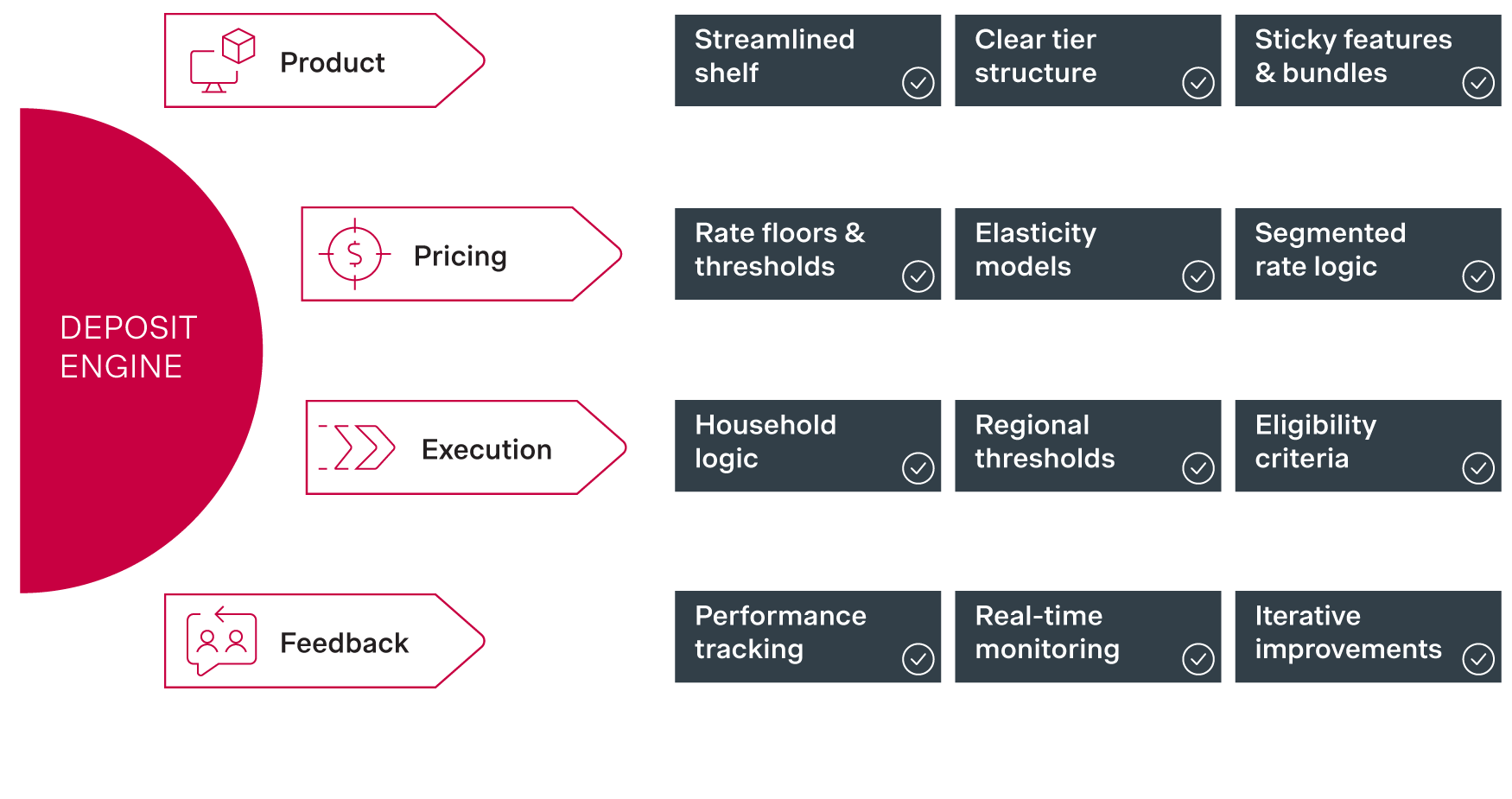

Link marketing to pricing, product, and execution

The best campaigns don’t work in isolation.

A winning campaign depends on what sits behind it. The strongest deposit marketing is wired into a broader commercial engine, not bolted on as an afterthought.

- Simplified product shelf: A modernized lineup sharpens messaging and focuses attention where it matters. For more, see our article on smarter product design.

- Pricing coordination: Marketing and pricing need to align on thresholds, floors, and elasticity. Without proper alignment, campaigns either overshoot on cost or underperform on conversion. See our article on segmented and individualized pricing.

- Disciplined execution: The best-designed campaign still fails if the rules aren’t followed. Household logic, regional thresholds, and eligibility criteria need to be implemented cleanly, not approximated.

Closed-loop feedback: Every campaign should feed performance data back into pricing and segmentation models. Each cycle gets sharper than the last. Essentially, campaigns should be part of the deposit engine, not one-off bursts of marketing activity.

How we can help

The commercial logic behind great campaigns.

We help banks turn marketing from a cost center into a margin lever. Our approach brings marketing, pricing, and product teams together to:

- Define a value proposition beyond rate: Articulate why customers should stay, not just why they should switch.

- Design campaign mechanics that align with actual customer behavior and margin targets.

- Coordinate cross-functional execution so marketing, pricing, and product aren’t working at cross-purposes.

- Build ROI tracking, targeting logic, and governance frameworks that make performance consistent and measurable.

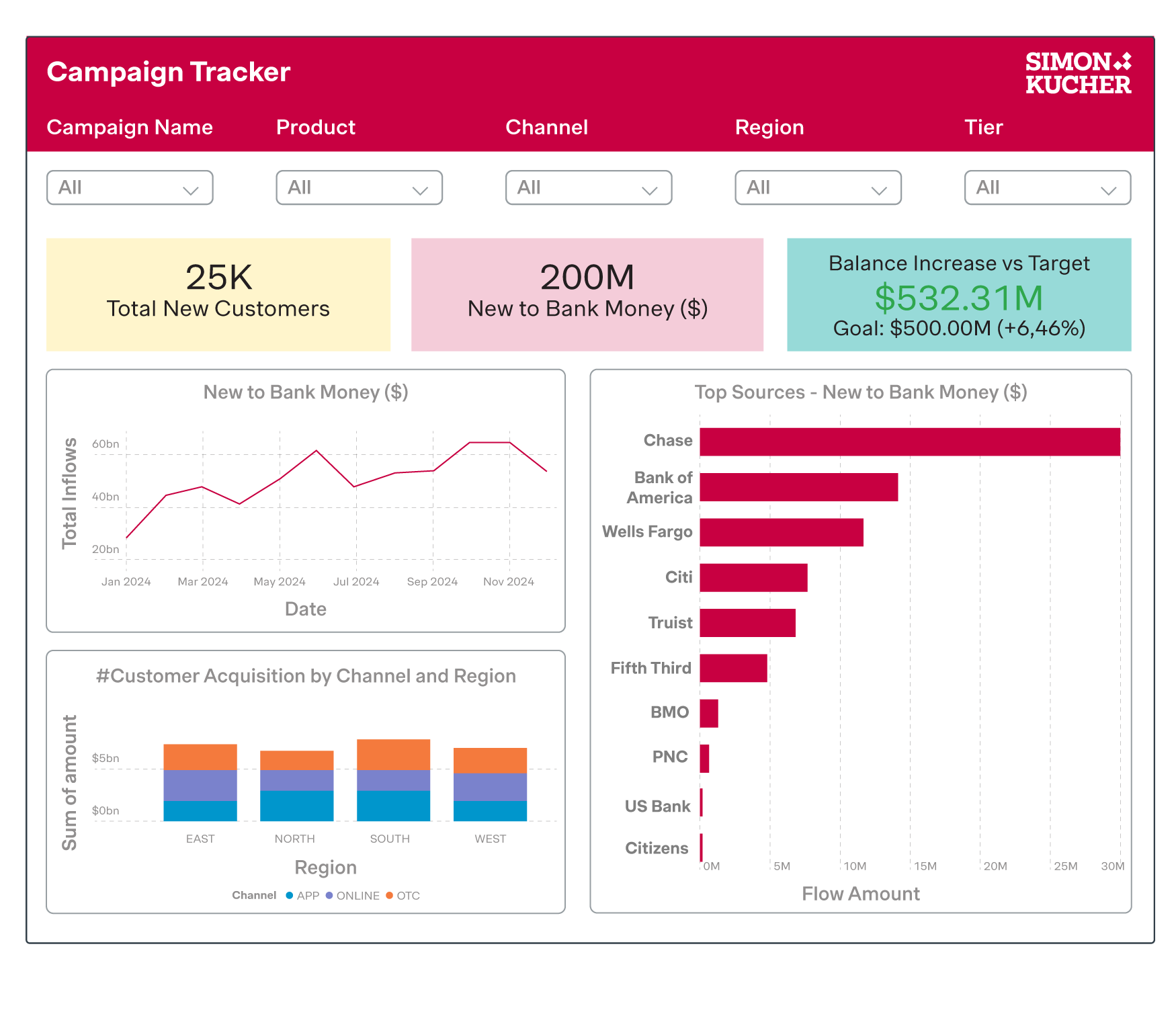

Our capability enables highly actionable data to fine-tune and amplify marketing strategies. We cleanly identify new-to-bank funds, the competitors from which they are acquired, and the level of off-set driven by internal cannibalization.

Ready to market deposits more profitably?

You don’t need to outspend your competitors. You need to out think them. Smarter deposit marketing drives better growth, stronger loyalty, and higher profitability while avoiding overpaying for rate chasers.

Let’s talk about how we can help you market deposits more profitably.

For our full suite of “Deposits” articles, click here.

{kind=link}