How President Trump’s Most Favored Nation agenda is forcing pharmaceutical companies to rethink pricing, launch sequencing, and the economics of innovation.

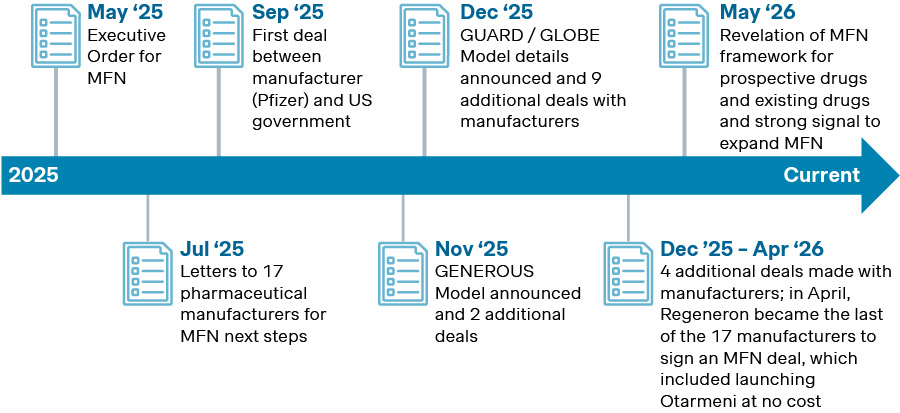

No healthcare policy initiative in the last two decades has had the potential to reshape the global pharmaceutical industry as profoundly as President Trump’s Most Favored Nation (MFN) agenda. From the first executive order last May, to the MFN letters over the summer, to the initial agreements in the fall and the final wave of deals through the winter and into the spring, the past year has been quite an odyssey. The journey was felt most acutely by CEOs, commercial and market access leaders, and the country affiliates now tasked with achieving local access without destroying a product’s overall revenue potential.

But MFN was never going to stop at pricing and market access. It reaches into new product planning, infrastructure choices, therapeutic-area strategy, business development and licensing, and the evidence-generation plans used to demonstrate value over time. In short, this is not just a pricing policy. It is a strategic shock to the operating model of the modern pharmaceutical company, and almost no part of that model will remain untouched.

The real center of gravity

As we have argued previously, the most consequential element of the MFN agenda was never simply the promise of lower prices in Medicaid or a handful of cash-pay discounts through TrumpRx. It was the commitment by the 17 largest manufacturers to realign launch pricing between the United States and the GENEROUS 8 markets at the net level for new medicines. That is the point at which MFN ceases to be a pricing policy and becomes a structural intervention into how global pharmaceutical value is recognized and monetized.

The precise terms of the agreements remain highly confidential, but the recent report from the Council of Economic Advisers confirmed the commitment by all 17 manufacturers to “offer all new drugs launched in the US at prices comparable to those in other high‑income countries”. What the administration has termed “prospective MFN” will apply across all channels in the United States, including the private insurance market. Unlike the proposed GLOBE and GUARD demonstration models, which are confined to Medicare Part B and Part D, this type of launch-price alignment reaches across channels, including the commercial market, which is typically the largest and most profitable part of the US business.

That is why the implications run far beyond traditional pricing and market access. Once net launch prices in ex-US markets begin to determine the economics of the American commercial channel, MFN starts to shape not just what companies charge, but what they launch, where they launch, and whether they launch at all.

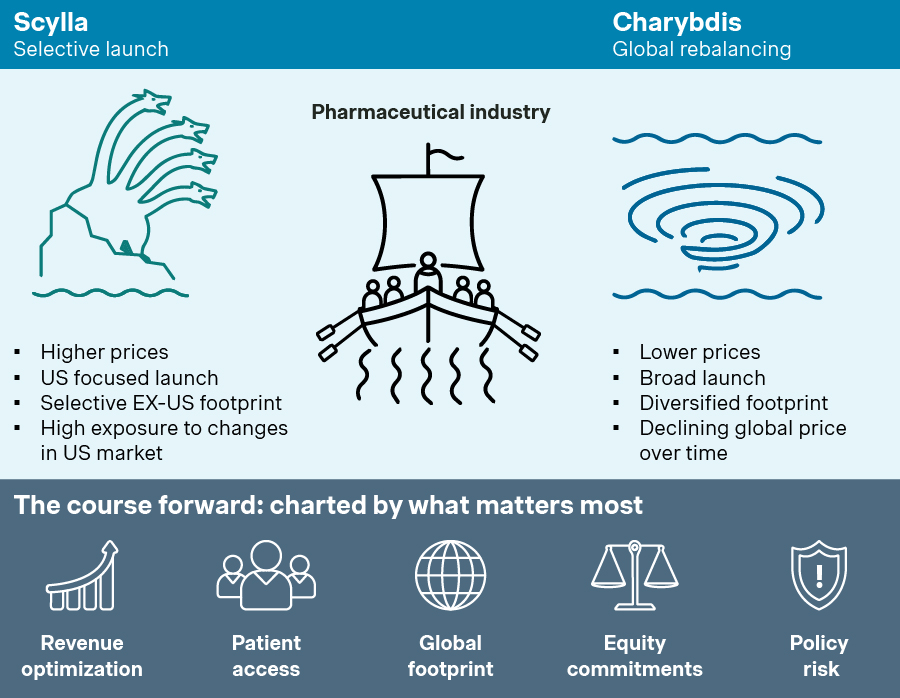

Scylla and Charybdis: Sacrifice or rebalance?

For those companies that have agreed to a White House MFN deal, pricing strategy for new launches now increasingly resembles Odysseus' dilemma between Scylla and Charybdis. Scylla was the painful but survivable sacrifice of a few men, Charybdis was the whirlpool, threatening catastrophic loss if the ship was pulled under. The metaphor is apt for launch strategy under MFN.

Companies that sail toward Scylla would be making a painful but rational decision: accepting a limited sacrifice in order to avoid a much larger disaster. The starting point is the United States. Manufacturers would first determine the optimal US strategy, given that the market has historically accounted for roughly 50% to 70% of global revenue and profit. They would then calculate the weighted-average net price across US channels under that strategy. That number is not static, and it is certainly not singular. It will evolve over time as commercial contracts are renegotiated, government discounts change, inflation penalties accumulate, and the channel mix shifts.

Once that moving US anchor has been established, the next step is to translate it into a GDP-PPP-adjusted net floor price for each of the GENEROUS 8 reference markets. The purpose of that floor is simple: prevent any ex-US launch from dragging down the US net price and, by extension, the core economics of the product. Because US net prices often decline over time for many products and categories, contrary to the popular caricature of ever-rising prices, that floor may itself drift downward over the life cycle. In theory, that creates the possibility that some countries unable to launch early could still launch later, once the US weighted-average net price has eased enough to make the floor more attainable.

But in the early years of launch, the practical implication is likely to be severe. Some markets simply will not be able to reach that floor. And that means Scylla, in strategic terms, is the conscious decision to give up a few launches in order to preserve the wider vessel. There is one important wrinkle, however. If MFN does not apply in cases where only one benchmark market has launched, manufacturers may have a narrow but meaningful escape hatch: a US plus one strategy. In that scenario, a company could select a single GENEROUS 8 country for early launch without triggering immediate consequences for the US price, preserving both some ex-US presence and the much larger economics of the American market.

The alternative to sailing toward Scylla is, of course, to sail toward Charybdis. In pricing and market access terms, this means attempting a true global rebalancing strategy – an optimal pricing architecture across both the US and the GENEROUS 8 markets at GDP-PPP-adjusted net prices. The underlying assumption is that lower US prices could be offset, at least in part, by a combination of greater US volume and meaningfully higher ex-US prices.

This is broadly the direction advocated by the EU’s Network of National Competent Authorities on Pricing and Reimbursement in its recent position paper. Their argument is that lower prices in the US could ultimately support pharmaceutical revenues by expanding access among uninsured and underinsured patients and thereby increasing volume. We remain skeptical that the evidence currently supports such a strong conclusion. Still, one should not dismiss the broader point too quickly. Depending on the degree of US price elasticity, the impact of lower prices on profit can vary significantly. In other words, Charybdis is not pure fantasy. But it is a strategy that requires extraordinary confidence in the responsiveness of demand, the willingness of ex-US markets to absorb materially higher prices, and the industry’s ability to navigate both without being pulled under.

How much pain would a lower US price cause?

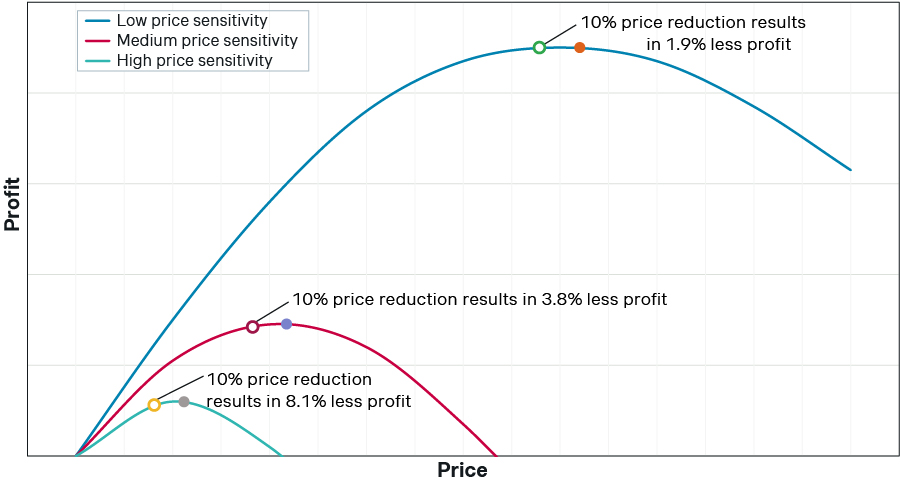

Drawing on the work of Simon-Kucher co-founder Hermann Simon and the broader logic of price sensitivity, we approach the US side of this problem through a simple price-profit curve. In the illustration below, we model three hypothetical scenarios for the US market: low price sensitivity, medium price sensitivity, and high price sensitivity. For each curve, we calculate both the profit-maximizing price and the profit that would result from pricing 10% below that optimum.

When price sensitivity is low, a price set 10% below the theoretical optimum reduces profit by only about 1.9%. Under medium price sensitivity, the reduction rises to roughly 3.8%. Only in the high-sensitivity case does the penalty become much more pronounced, at about 8.1%. The implication is important: not every product is equally exposed to the downside of pricing below the model-derived optimum.

As a further thought experiment, Figure 3 extends this analysis by looking at a wider range of prices below the theoretical optimum and measuring the corresponding loss in profit.

Profit loss from pricing below the optimal price

| Price reduction below optimal | Low price sensitivity | Medium price sensitivity | High price sensitivity |

|---|---|---|---|

| 5% | 0.5% | 0.9% | 2.0% |

| 10% | 1.9% | 3.8% | 8.1% |

| 15% | 4.3% | 8.5% | 18.2% |

| 20% | 7.6% | 15.1% | 32.4% |

| 25% | 11.9% | 23.6% | 50.6% |

When price sensitivity is low, the economics are surprisingly forgiving. A product can be priced meaningfully below the calculated optimum and still retain most of its profit. Even at 25% below the theoretical optimum, profit falls by less than 12% in the low-sensitivity case. But when price sensitivity is high, the picture changes dramatically: the same 25% reduction cuts profit by more than half.

That is what makes this analysis so relevant in an MFN world. For some products, especially those with low elasticity, a deliberately lower US net price may be a manageable trade-off if it unlocks more ex-US launches. For others, the cost of that strategy could be severe. The entire question turns on how much economic pain the US business can absorb before the promise of global rebalancing collapses under its own weight.

That matters because, in our experience over decades of pricing and market access work in the United States, price sensitivity varies enormously across products and therapeutic areas. For some medicines – especially high-value therapies, life-saving products, and many rare-disease treatments – elasticity can be surprisingly limited. In those settings, a US pricing strategy that sits somewhat below the calculated economic optimum may not do nearly as much damage to US-generated revenue and profit as conventional intuition would suggest. And that, in turn, makes the Charybdis strategy at least conceivable for some categories: a manufacturer may be able to give up some price in the US without immediately sacrificing the economics of the product, provided that the resulting volume response or ex-US rebalancing is strong enough to compensate.

The immediate question is why would any company deliberately pursue a US pricing strategy that sits below the economic optimum? In the pre-MFN world, that would have made very little sense. But in a world where the US net price directly determines the GDP-PPP-adjusted floor price for the GENEROUS 8 markets, accepting a modestly lower US price – particularly in categories where profit is only minimally affected – could create the room to launch in more ex-US markets, perhaps even all eight.

But that is precisely why this strategy is so dangerous. If Scylla is the painful but controlled sacrifice, Charybdis is the bet that one can pass through without being pulled under. From a commercial standpoint, the risk of failure is enormous. A manufacturer that does not have a deeply grounded understanding of the true net price-volume relationship across all US channels could easily misjudge the tradeoff and either understate or overstate the GDP-PPP-adjusted floor price that its global strategy can tolerate. Worse still, even a carefully chosen lower US price only works if it meaningfully expands the number of GENEROUS 8 markets that can actually launch at the resulting floor. If the revised threshold is still too high for most of those markets to bear, then the company has simply given up US value without unlocking the ex-US opportunity it was counting on.

That is why this is not a back-of-the-envelope exercise. Manufacturers would need an unusually robust understanding of two things at once: first, the true price-volume curve in the United States at the net level across commercial and government channels; and second, the true price-access curve in each of the GENEROUS 8 markets, including not only formal willingness to pay, but also the local mitigation strategies that might help reach those levels. Only by integrating those two perspectives into a single model can a company begin to understand what the genuine US plus GENEROUS 8 optimal pricing strategy looks like. That demands a level of analytical depth and cross-market sophistication that very few organizations have ever been required to develop – at least until now.

We work with pharmaceutical manufacturers on the US and global pricing strategy under MFN. To discuss how these dynamics apply to your portfolio, contact us.