What will define financial resilience for companies in Turkey? Many companies struggle with how resources are allocated. Therefore, moving beyond incremental budgeting and building a culture of cost ownership is becoming critical. Zero-Based Budgeting (ZBB) offers a structured approach to driver smarter spending, stronger discipline, and sustainable growth.

The challenges companies in Turkey face – and why cost optimization matters

Companies operating in Turkey have been navigating a demanding and highly uncertain economic environment in recent years. Persistently high and volatile inflation, currency fluctuations, rising labor costs, and increasing rent and energy expenses have placed significant pressure on profitability, particularly across retail, consumer goods, and service sectors.

Heightened consumer price sensitivity has further constrained the ability to pass rising costs on to customers. The prevailing expectation is that the disinflation process will continue; however, cost volatility is unlikely to abate in the short term. While institutions such as the IMF and OECD point to a gradual growth recovery, they also emphasize that inflation dynamics and financing conditions remain key risk factors for emerging markets.

This environment requires companies to pursue the right growth trajectory while strengthening cash generation capabilities and financial discipline – without undermining commercial momentum.

"For most companies, the real issue is not the costs themselves, but the misallocation of resources."

- Okan Cetinturk, Partner

The hidden cost of incremental budgeting

At its core, resource allocation is the central challenge of economics. Yet many organizations continue to make these decisions by automatically rolling forward budgets from the previous year.

The widespread use of incremental budgeting in Turkey creates structural vulnerabilities in this environment. Continuing last year’s spending without systematic reassessment gradually leads to:

- The persistence of low-value activities

- Blurred accountability over spending

- A “use it because it’s budgeted” mindset

- Unintended damage to value-creating initiatives during reactive cuts.

As a result, cost optimization can no longer be viewed as a temporary cost-cutting reflex. It has become a strategic management agenda that determines organizational resilience and competitiveness. The objective is not a one-time saving, but a system that continuously challenges spending without compromising growth and commercial priorities.

This is where zero-based budgeting (ZBB) is gaining a foothold as a more disciplined alternative.

What is zero-based budgeting?

Zero-based budgeting is a costing and planning methodology that requires every expense to be evaluated from a zero base in each budget cycle. Every cost must be justified with a clear business rationale. Its core principle is simple: a cost incurred in the past is not, by that fact alone, entitled to continue – it must be earned each cycle.

ZBB forces organizations to confront four critical questions:

- Is this activity truly necessary?

- Can the same output be delivered at lower cost?

- How does this spending contribute to business objectives?

- What are the alternative scenarios?

One of its most important benefits is that it enables the right OPEX allocation upfront, reducing the need for abrupt and reactive cost cuts later in the year.

In volatile and cost-pressured environments, it stands out because it:

- Increases transparency across spending

- Strengthens cost ownership and reduces control gaps

- Forces deliberate, value-based resource allocation.

Modern ZBB implementations differ significantly from earlier bureaucratic models. Today, they are designed as dynamic cost management systems supported by digital data infrastructure, clear governance, and strong monitoring mechanisms.

How zero-based budgeting works in practice

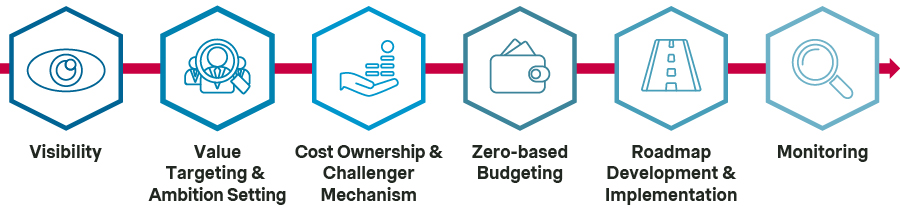

ZBB is an end-to-end management framework, not a one-off budgeting exercise, and it rests on six operational pillars.

1. Visibility

The first step is full transparency across spending. Without a clear answer to who spends what, why, and how much, ZBB cannot function effectively.

2. Value targeting and ambition setting

Organizations assess which costs truly create value and which persist out of habit. External benchmarks and internal business needs are used to set realistic but ambitious targets.

3. Cost ownership and challenge mechanism

One of the most critical components of ZBB is establishing clear ownership and a structured challenge process. In many organizations, budgets exist on paper, but true ownership is unclear. Over time, expenses become “default.” ZBB disrupts this dynamic: every cost line has a clearly defined owner, the roles of requester and challenger are separated, and precedent alone is not considered sufficient justification.

4. Building the budget from zero

Rather than adjusting prior-year figures, ZBB constructs budgets from scratch through structured workshops. Spending is pre-analyzed and broken down by activity. Cost owners, finance teams, and cross-functional stakeholders then convene in workshops where they debate each activity’s purpose, scope, and service level.

In advanced implementations, data-driven and machine learning-supported functional budgeting models further strengthen the foundation of these decisions. In one retail case, a demand- and performance-based machine learning shift model enabled more transparent and measurable workforce optimization.

5. Roadmap and implementation

Approved initiatives are translated into concrete action plans with defined owners, timelines, and financial targets.

6. Monitoring

Actual spending is continuously tracked against budget. Variances are addressed, and ZBB behavior becomes embedded as an organizational habit.

Benefits and challenges of ZBB: Results and realities from a retail implementation in Turkey

The returns from a well-executed ZBB program can be material. At a large-scale retail company in Turkey, a comprehensive implementation delivered recurring OPEX savings potential of 5-10%.

Budgeting discipline improved across the highest-spend categories such as labor, marketing, logistics, and travel. There was notably greater transparency in marketing and outsourcing spend, particularly in service-sector applications. The retail organization also noticed strong structural gains: clearer cost ownership, stronger accountability culture, and budgeting processes that lasted beyond the initial cycle.

The challenges, however, were not trivial. Three issues recurred consistently across the implementation.

The first was organizational resistance. Continuous scrutiny of spending was perceived as additional workload or a slowdown rather than a source of discipline. The second was data visibility gaps. Inconsistent classification or poor data quality limited the depth of ZBB discussions and reduced confidence in outputs. The third was delayed ownership adoption. When ZBB is perceived as a finance-only initiative, business units are slower to engage.

None of these challenges are disqualifying. But they are also not resolved by process design alone. They require careful scoping, strong C-Level executive sponsorship, and disciplined follow-up that outlasts the initial implementation phase.

Critical actions for successful ZBB implementation

Frame it as resource transformation, not cost reduction. How ZBB is positioned at the outset shapes every interaction that follows.

- Focus on high-impact areas first. Organizations that attempt a full reset across all functions simultaneously generate noise and lose momentum.

- Assign ownership with authority, not just responsibility. Cost and budget owners must be genuinely empowered to lead the process, not simply accountable for its output.

- Use pilots to build credibility and conviction. It helps demonstrate returns in a contained environment before broader rollout.

- Let digital infrastructure do the heavy lifting. The right digital tools that make spending transparent and variance tracking continuous are what make the framework repeatable.

- Close the loop between savings and planning. Track and validate realized savings and integrate them into business planning.

- Advance with a growth-oriented mindset rather than a restrictive one. Organizations that prioritize resource redeployment tend to outperform those driven by reduction targets alone.

How is your organization approaching resource allocation today? Where could greater transparency and ownership unlock more value? If you would like to explore how to take a more structured approach, don't hesitate to reach out to us.