Form placeholder. This will only show within the editor

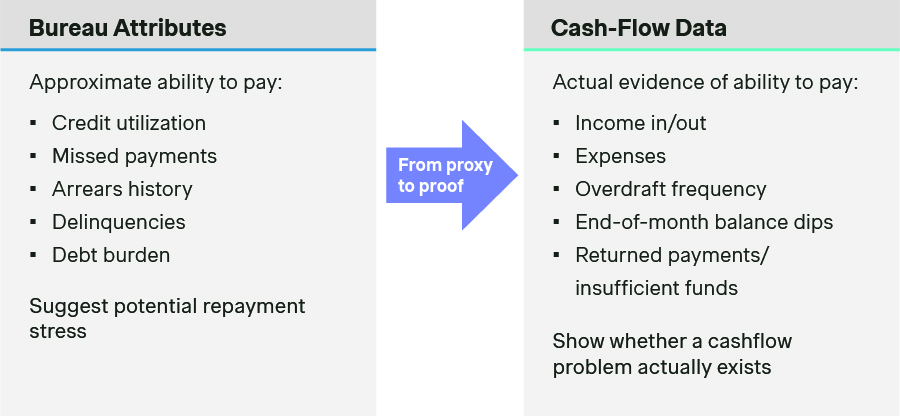

For decades, banks and financial institutions relied on credit bureau data as the foundation of consumer underwriting. They pulled reports with credit scores, tradelines, delinquencies, and utilization rates to determine a consumer’s credit worthiness. However, these metrics only reveal part of the picture. They tell a lender how a borrower handled credit and financial obligations in the past, not whether that borrower has the liquidity and financial resilience to handle repayment obligations now.

To manage credit risk in today’s environment, banks need an underwriting playbook that moves beyond static bureau data and captures the real‑time cash‑flow dynamics that impact current repayment behaviors.

Two applicants may appear nearly identical through the lens of traditional credit bureau data yet have vastly different financial realities. One may have steady income, a healthy cash buffer, and enough flexibility to absorb short-term shocks. While the other may be living paycheck-to-paycheck, with expenses stacked tightly around payday and little room for disruption.

By analyzing a borrower’s bank transaction data including inflows, outflows, balances, and recurring obligations, lenders can build a more complete view of the customer’s credit risk profile. This is especially valuable for thin-file borrowers, customers with volatile income, and customer segments where bureau data provides only a partial signal.

Advances in technology have made cash-flow-based underwriting essential to stay competitive. Open banking infrastructure provides real-time access to transaction data. Data connectivity has become more scalable, and advances in machine learning, especially Large Language Model (LLM)-enabled enrichment, have made it easier to turn unstructured transaction strings into decision-ready underwriting inputs. What once required heavy manual effort is now operationally feasible for most institutions.

The four pillars of modern cash-flow underwriting

Consumer underwriting is increasingly about combining traditional credit history with a real-time view of liquidity, volatility, and affordability. Institutions that do this well will make better approvals, set better limits, and calibrate products more effectively.

A scalable cash-flow underwriting strategy rests on four pillars.

Transaction data does not replace traditional bureau assessments. Bureau data is backward-looking while transaction data is current. The latter captures whether income is recurring, whether balances are repeatedly depleted, and whether customers can absorb recurring obligations without hitting zero. Taken together, lenders have a clearer view of the borrower’s financial resilience, especially in segments where bureau files are thin or noisy.

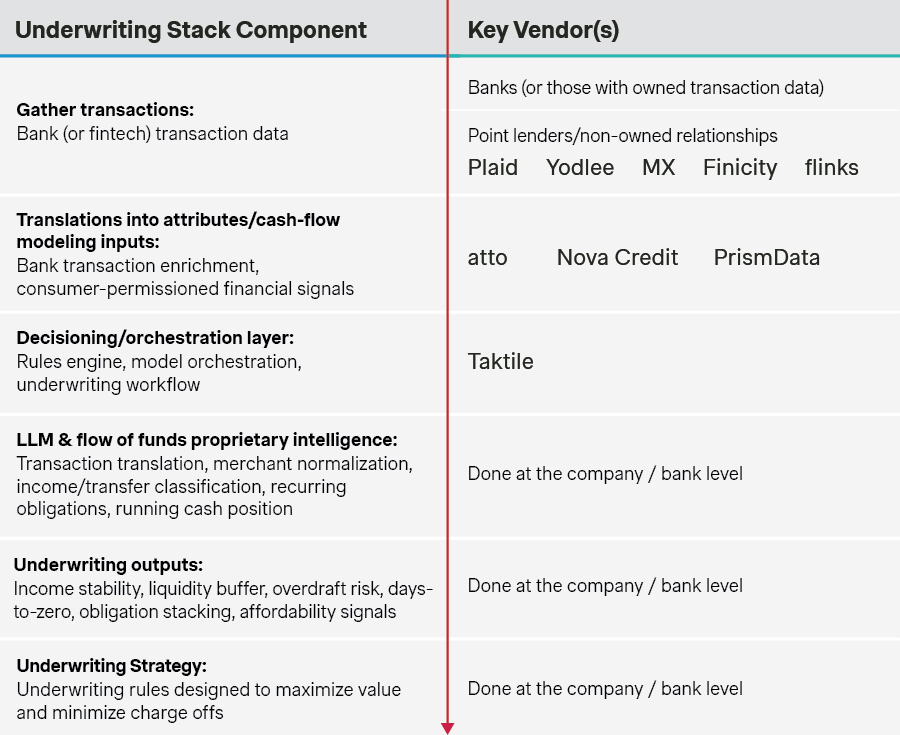

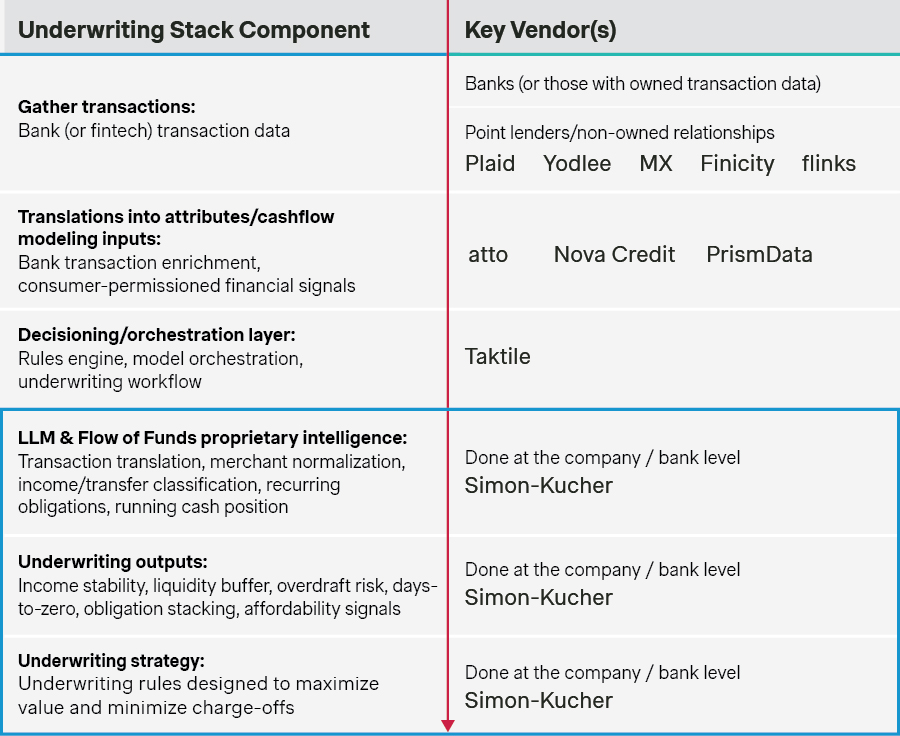

Leverage LLMs to transform raw data. The challenge is not just data access, but working with raw, unstructured data. Merchant names can be inconsistent, transfers can resemble income, and recurring bills can be difficult to identify at scale. LLMs can help normalize merchant names, separate income from transfers, and classify obligations. LLMs can turn raw transaction data into structured, underwriting-ready information. It is important to note that LLMs are not the decision engine. They are the enrichment layer that helps banks create stable, explainable features for downstream models and policy rules.

Operationalize governance and iteration. Instead of treating cash-flow underwriting as a one-time model build, lenders must treat it like an iterative capability. This means regularly testing and comparing bureau-only models against cash-flow-enhanced approaches, allowing for improvements to enrichment logic, and keeping the feature layer stable even as the underlying tagging evolves. To maximize efficacy and effectiveness, underwriting stacks can be organized into three layers: enrichment, flow-of-funds computation, and credit decisioning.

Make sure the economics work. Cash-flow underwriting creates value when improvements in risk assessment outweighs the added cost, complexity, and conversion loss arising from data transformation. The best use cases are when transaction visibility already exists, account linking is easy to justify, or the product economics are especially sensitive to affordability. For banks, that often means focusing on borderline approvals, line assignment, installment sizing, early warning, or thin-file segments rather than trying to overhaul the full underwriting stack at once.

Table stakes and implementation challenges

Cash-flow underwriting is no longer an alternative risk assessment tool used by niche players. It has become standard for traditional banks, credit unions, and mainstream lenders. In 2025, JPMorgan Chase shared that it would use Nova Credit’s cash-flow underwriting software to evaluate potential borrower’s credit worthiness. Similarly, Fannie Mae has expanded its Desktop Underwriter tool to include cash-flow assessments as part of its effort to help mortgage lenders determine creditworthiness.

The question isn’t whether cash-flow underwriting matters. It is how quickly institutions can deploy it in the right places, with the right architecture and business case.

For many institutions, implementing cash-flow underwriting can be challenging. Transaction data is not clean, standardized, or naturally underwriting-ready. Building a true flow-of-funds view means reconstructing how money moves through an account over time, identifying recurring inflows and obligations, and separating signals from noise across highly variable transaction strings.

Institutions must wrestle with a host of logistical, data governance, and workflow issues. This includes managing customer consent across the decisioning journey, overcoming fragmented data pipelines, meeting higher standards of explainability and documentation, and addressing incomplete or unstable data pulls.

Institutional inertia can be another barrier. Most lenders remain organized around bureau-first paradigms, with embedded credit policies and workflows that are not designed to incorporate real-time behavioral data.

Optimizing cash-flow underwriting at your bank

Early deployments of cash-flow underwriting are most effective when they are tightly scoped. Instead of overhauling the full credit stack, leading institutions should start with a single decision point where the impact is measurable, and the economics are clear.

Common entry points include:

- Borderline applications near the approval cutoff, where incremental data can shift decisions

- Affordability calibration for installment products, where payment sizing is critical

- Capacity-based line setting in revolving portfolios, where exposure can be more precisely matched to ability to pay

Cash-flow underwriting offers a clear path forward for banks to improve risk selection, grow responsibly, and modernize credit decisioning. Simon-Kucher can help define that path, prioritize the highest-value use cases, and turn capability into measurable performance.

Esteban De Las Traviesas and Julia Hines contributed to this article.