The rise of agentic AI is reshaping how enterprises think about AI implementation across their systems and workflows. Building on advancements from predictive and generative AI, this third wave introduces autonomous agents that execute complex tasks with minimal human input.

Increased adoption across industries is prompting companies to move beyond experimentation to scaled deployment. According to our 2025 Global Software Study, 74%² of US buyers plan to adopt new AI solutions in the next two years.

However, SaaS, data, and software-heavy companies across the broader market have lost $2 trillion¹ in market value as investors reassess the role of traditional software models in an increasingly AI-driven landscape. Traditional software tools are designed to enable human-led workflows with sticky UI/UX and administrative control for users. Software Incumbents now face disintermediation, and a loss of market share as agentic AI and LLMs continue rewriting the rules.

AI is fundamentally changing where value lives in the software business. Investors and management teams must adjust their monetization strategies to better position assets and ask:

- How structurally exposed is the company’s asset?

- What actions can be taken to improve moats and monetize available upside?

From interface advantage to orchestration control

Traditionally, software moats were characterized by features like user interface optimization and user assistance. However, agentic AI is shifting this basis of competition to end-to-end orchestration and workflow execution.

AI disruptors and LLMs are challenging human-operated workflow enablement tools particularly as agentic solutions become increasingly “headless.” In these environments, agents interact directly with software and servers without human intervention, resulting in UI and UX becoming less pertinent to workflow enablement.

Industry incumbents are already responding to tangible substitution risk, as production adoption becomes simplified. For example, Zendesk’s acquisition of Forethought in March 2026 was a play at bolstering its AI-driven customer service capabilities. Similarly, Anthropic launched its “managed agents,” to help reduce the engineering burden of deploying agents for businesses.

However, incremental product enhancements won’t be enough to maintain competitiveness. Moving forward, companies should implement a three-step framework that:

- Assesses defensibility and moats

- Improves the moats

- Provides clarity over how monetize the upside

Assess defensibility and moats

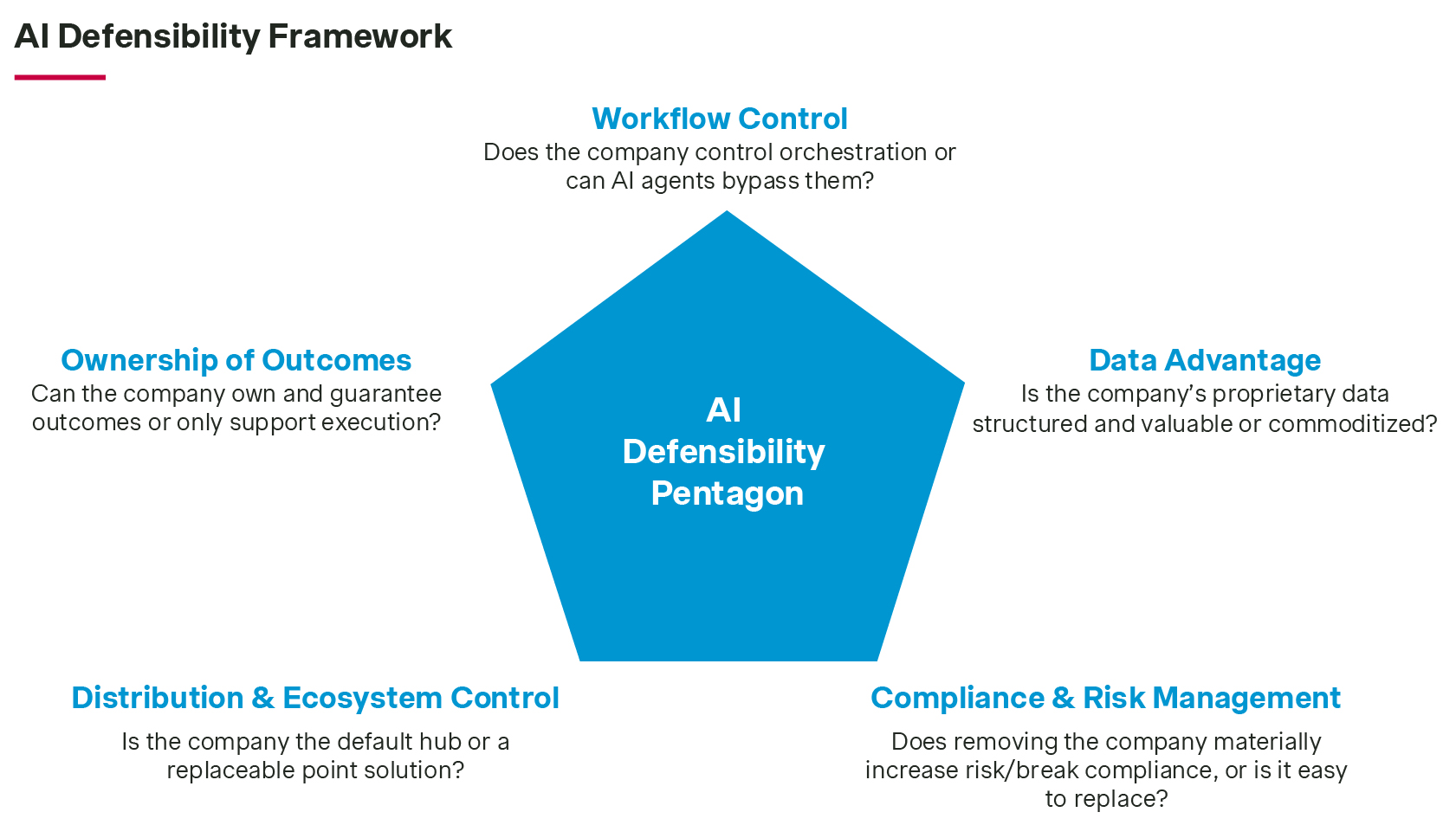

As agentic AI redefines economics and workflows, the first step for incumbents is to identify where value is created. Competing in a fast-paced agentic landscape requires enterprises to identify which combination of the following five emerging moats they want to build upon to future-proof their business.

Workflow control: Take ownership of the orchestration layer where work is coordinated and executed, often through deeply embedded, cross-functional workflows with high switching costs. AI exposes point solutions to a disintermediation risk while workflow controllers have greater defensibility, shifting the moat from feature excellence to orchestration superiority. Example: ServiceNow’s workflow engine that orchestrates approvals, tasks, notifications, and documentation.

Data advantage: Have access to unique, high-quality, proprietary data tied to core workflows. A company’s data is built on proprietary, non-replicable datasets that ensure strong moat defensibility. AI shifts data from storage to intelligence layer for training, fine-tuning, and benchmarking. Moreover, rich usage data powers the retrieval layer for RAG-enabled assets. Examples: Crunchbase structures its data on companies, startups, investors, leadership, acquisitions, and market activity. Atlassian leverages product usage and workflow data ticket activity, collaboration patterns, and project velocity.

Compliance & risk management: Embed regulatory, security, auditability, and accuracy layers risk mitigation into customers’ control environments, increase switching costs and making removal materially risky, especially as demand for AI solutions grow. Example: Microsoft controls enterprise compliance layers, protecting data security, identity, and regulated cloud infrastructure.

Distribution & ecosystem control: Establish platform gravity through deep integrations and partner ecosystems, position the company as a default hub while making standalone point solutions structurally weaker. Example: Salesforce fully controls customer and partners access with key integration layers for partners to build on their platform.

Ownership of outcomes: Capture value by delivering and monetizing end-to-end outcomes, shifting from enablement to execution and strengthening the link between usage and measurable impact. Example: Intercom moved from seat to outcome-based pricing, charging per successful resolution.

Being strong in one area is not enough to maintain a competitive edge. For example, a company may have strong proprietary data but lacks protection across the other moats. Another company may adopt agentic capabilities to improve its marketing workflows but doesn’t own the orchestration system where the actual work is being performed.

By assessing their defensibility across moats, companies can begin making improvements in areas of their defensibility framework.

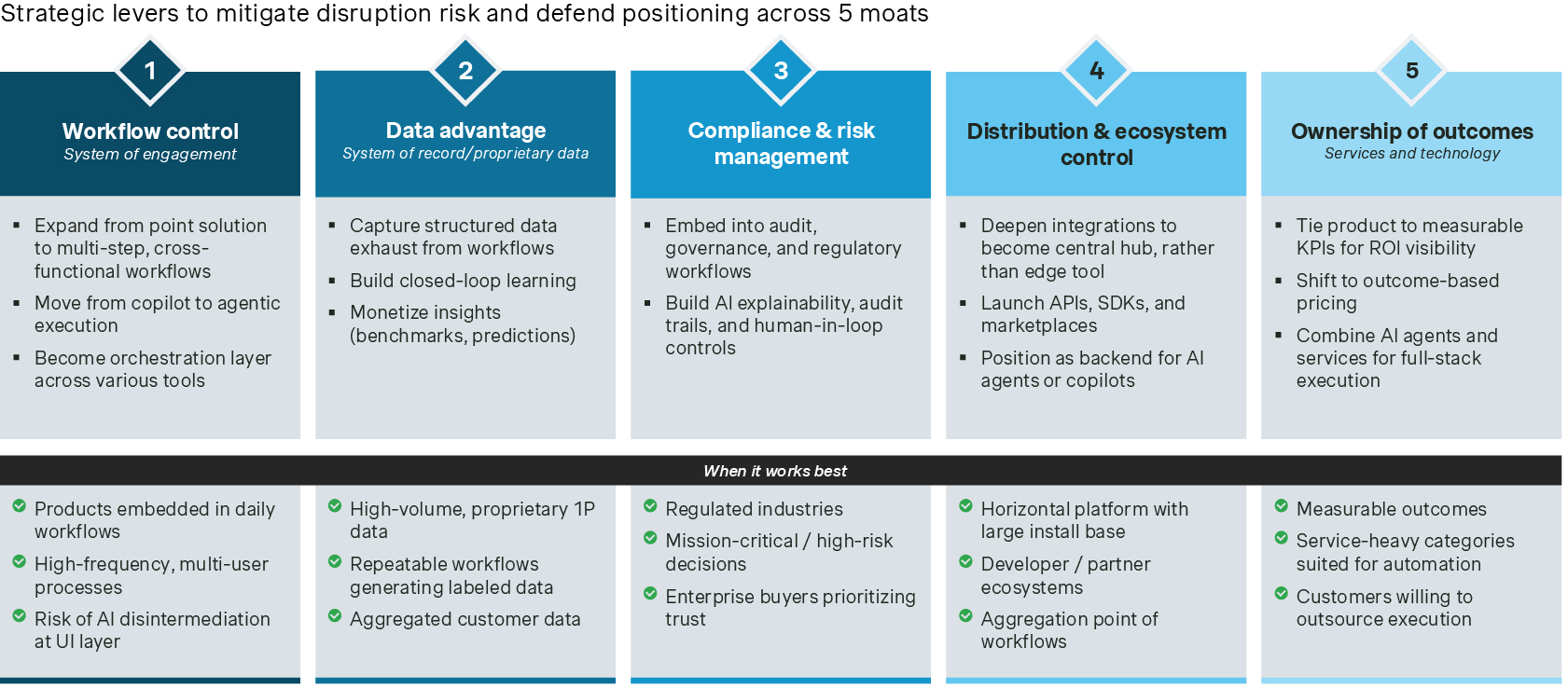

Improving moats for further defensibility

Companies can defend their existing capabilities while repositioning for agent-led growth.

Strengthening defensibility will hinge on shifting from interface ownership to control of the orchestration layer (i.e., owning the agent rather than the UI), while building proprietary feedback loops through continuous learning and embedding more deeply into enterprise systems through APIs and ecosystem integrations.

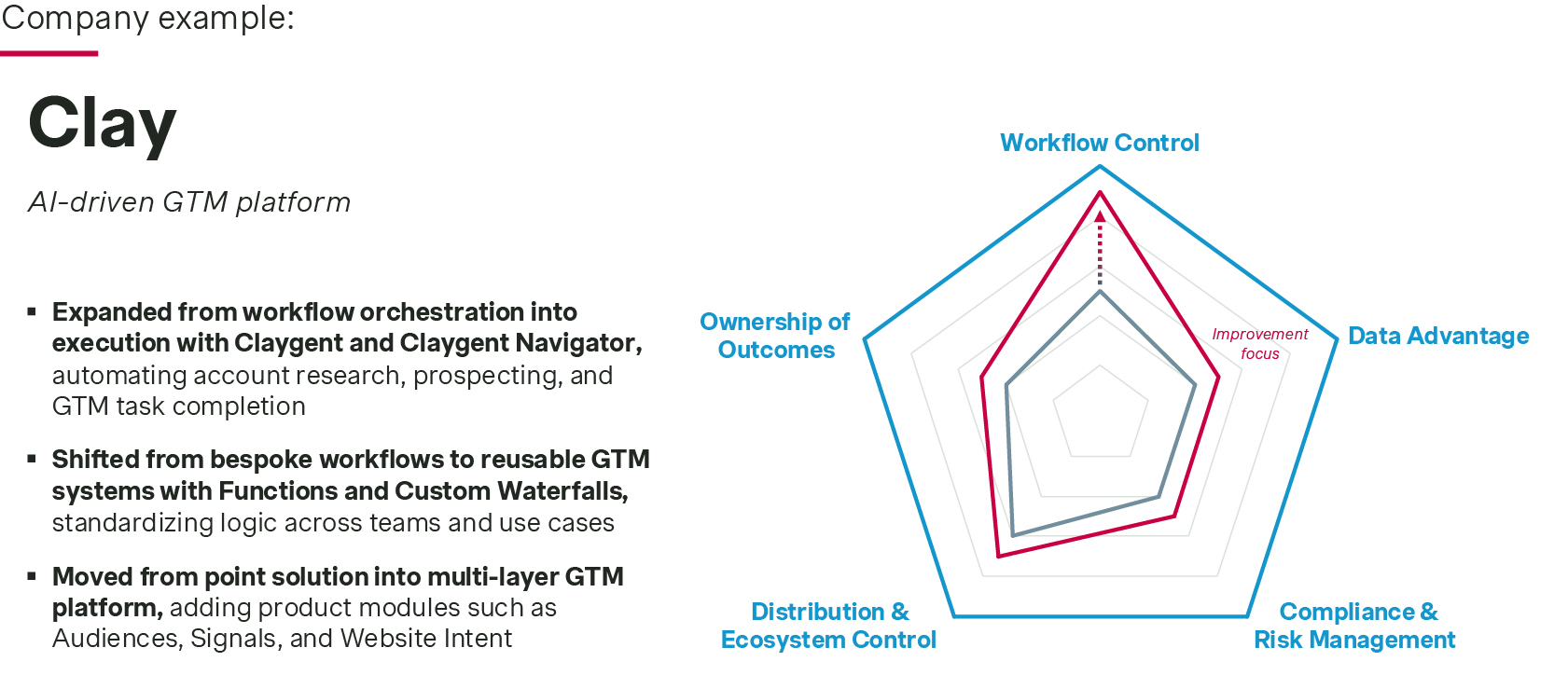

Clay, for example, moved away from workflow orchestration and expanded to an AI-powered GTM execution layer, deepening its workflow control. HubSpot improved its data-advantage moat by monetizing data as an intelligence layer using a credit-based pricing model, with added workflow execution.

In both examples Clay and HubSpot defended their existing capabilities while repositioning for agent-led growth.

Monetize the upside

Few companies have achieved high-impact AI monetization so far. While roughly two-thirds of companies in our Global Software Study report achieving their AI revenue targets, those targets have generally been modest, often implying less than 10% revenue uplift.

Part of this reflects a deliberate prioritization of adoption over short-term revenue maximization. However, many companies also lack a clear monetization playbook, instead relying on fragmented strategies that combine premium-plan bundling, seat-based add-ons, and usage-based pricing.

The pressure to establish scalable monetization models is increasing rapidly. Nearly all software companies are expected to launch new AI capabilities over the next two years, intensifying competitive pressure and reducing the window for experimentation.

But what does an effective monetization plan look like?

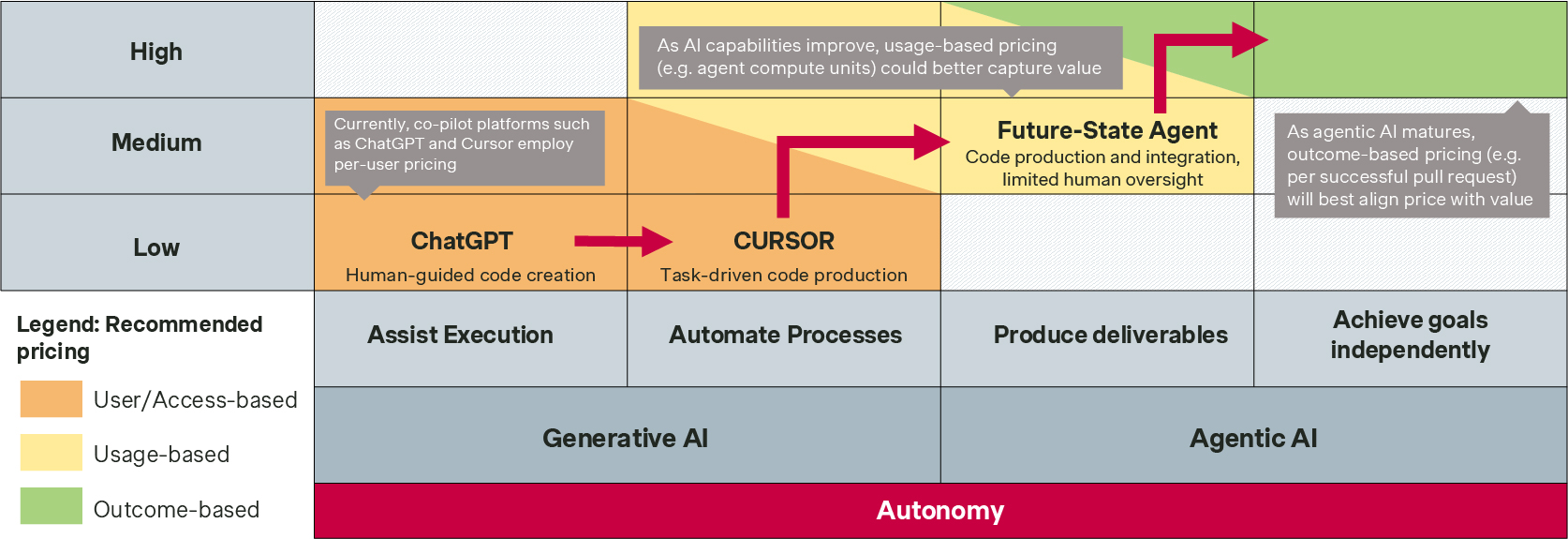

Capturing the upside from agentic AI will likely require a fundamental shift in monetization logic, as traditional seat-based pricing increasingly comes under pressure.

At the same time, while outcome-based pricing has attracted significant attention, it remains difficult to operationalize for many companies today. A more practical starting point is to evaluate AI solutions across two dimensions:

Autonomy: The degree to which an AI agent can operate independently. Higher autonomy implies broader scope, less human intervention, and greater ownership of workflows and decisions.

Attribution of impact: The extent to which outcomes can be clearly linked to the agent’s actions. Higher attribution enables clearer accountability and more measurable value creation.

For example, coding agents such as Cursor already automate parts of the software development workflow, but attribution remains relatively limited because they primarily augment developers rather than replace them. As a result, these solutions are still largely monetized through seat-based subscriptions, often with usage limits attached. Over time, as both autonomy and attribution increase, monetization models may evolve toward usage- and eventually outcome-based pricing, similar to Intercom’s Fin, where customers are charged per successful AI resolution.

The real shift in value

As AI agents take on more responsibility and their impact becomes more measurable, they will unlock more value-aligned metrics and pricing along the way. For companies, this creates both risk and opportunity. Existing moats can erode quickly if they are tied to interfaces or fragmented capabilities. Those that successfully move up the stack by owning orchestration, embedding into core workflows, and monetizing outcomes can achieve more value.

Simply adopting agents won’t be the path forward. Instead, companies must redefine where the business sits in the execution layer. That requires strengthening defensibility across moats, building continuous learning loops, and aligning monetization with delivered impact.

Contributing author: Jack Benson

References:

- Forbes, Thoma Bravo Says Public Markets Have Software Wrong And Is Positioning To Buy, 2026

- Simon-Kucher, Global Software Study 2025