The US is one of the most attractive markets for B2B fintechs looking to achieve scale. It offers a large addressable enterprise customer base, high spending power, mature fintech ecosystems that facilitate partnerships and distribution, and a financial services industry that continues to rely heavily on legacy infrastructure.

Despite the opportunity, the US market is also highly fragmented, fiercely competitive, and characterized by regulatory complexity. In this environment, success hinges on a disciplined go-to-market strategy (GTM), compelling product, and monetization models that effectively capture value.

In the following sections we provide a GTM framework for fintechs seeking to establish meaningful market presence within three to five years. The framework is designed to help fintech leaders refine their market entry strategies, sharpen their value propositions, and strengthen their right-to-win.

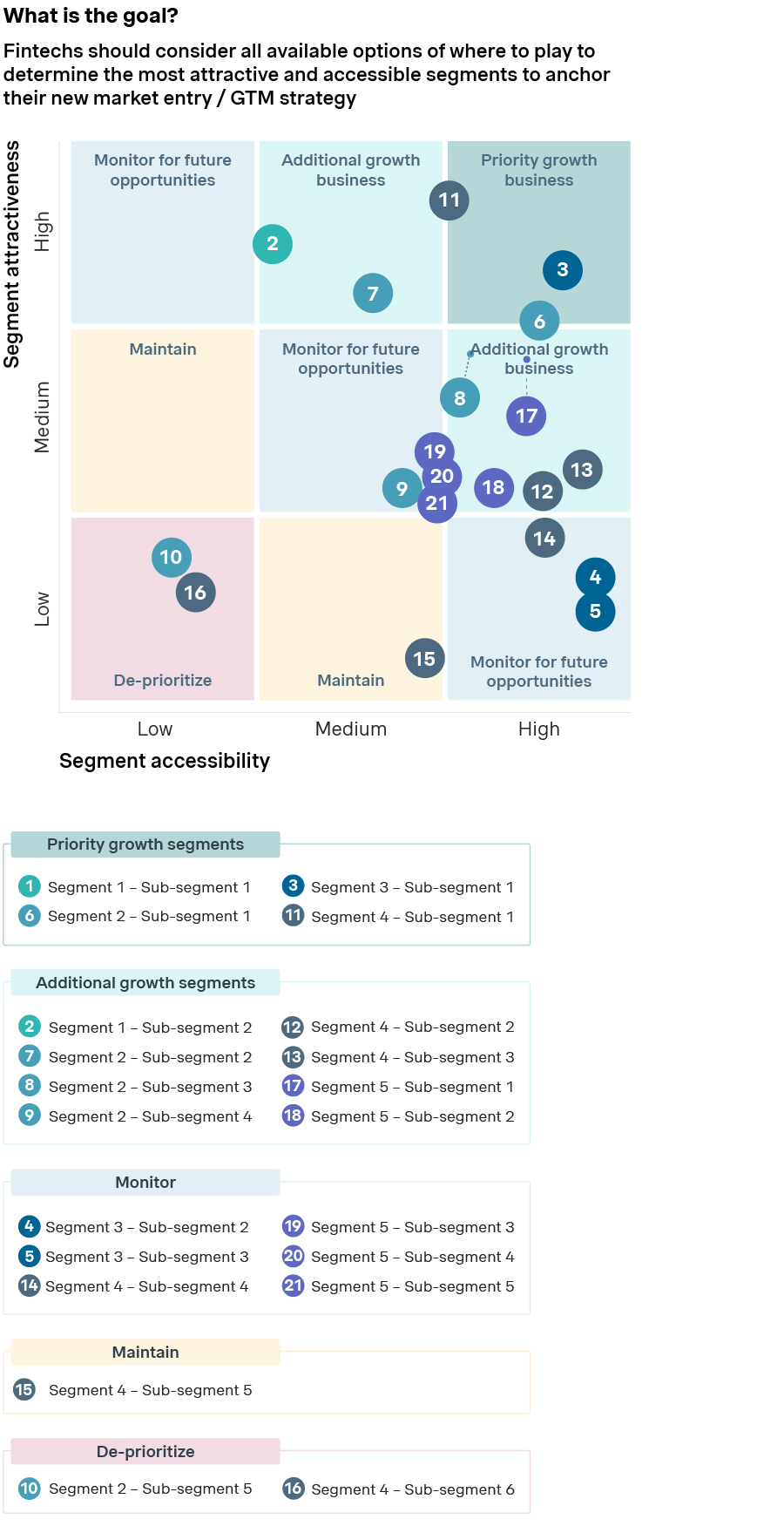

Prioritize segments for market entry

When evaluating the US market, fintechs may initially consider as many as 15 to 20 potential target segments combining size and sub-sector criteria as part of their Ideal Customer Profile (ICP).

However, for a successful market entry, the best approach is to focus on no more than five priority segments, with the goal being to identify those that offer the strongest combination of market attractiveness and accessibility (see Figure 1).

Segment attractiveness should be based on market size, growth potential, revenue opportunity, and strategic fit. Accessibility reflects the likelihood of winning business given the competitive landscape, customer buying behavior, and the fintech's capabilities. A segment that is relatively small today but expected to grow rapidly may represent a compelling opportunity. Conversely, large enterprise segments such as bulge bracket banks may appear attractive due to their size but can be difficult for new entrants to penetrate because of entrenched relationships, long procurement cycles, and high switching costs.

Understand your right-to-win

A fintech's ability to scale depends on whether it can identify and pursue segments where it has a sustainable competitive advantage. This requires an objective assessment of how well the company's offering aligns with the needs and purchase criteria of target segments.

Some segments might prioritize “hard” criteria like product functionality, performance, implementation capabilities, and pricing when selecting providers. Others might emphasize “soft” criteria such as brand reputation, customer relationships, and market presence. A vital question is whether the fintech has sufficient differentiation, capabilities, and market positioning to outperform competitors in a given segment.

For many fintechs, the right-to-win is also determined by access to distribution through banks, software platforms, accounting networks, and strategic partners.

A rigorous right-to-win assessment helps determine where the fintech is most likely to succeed and where it should concentrate resources.

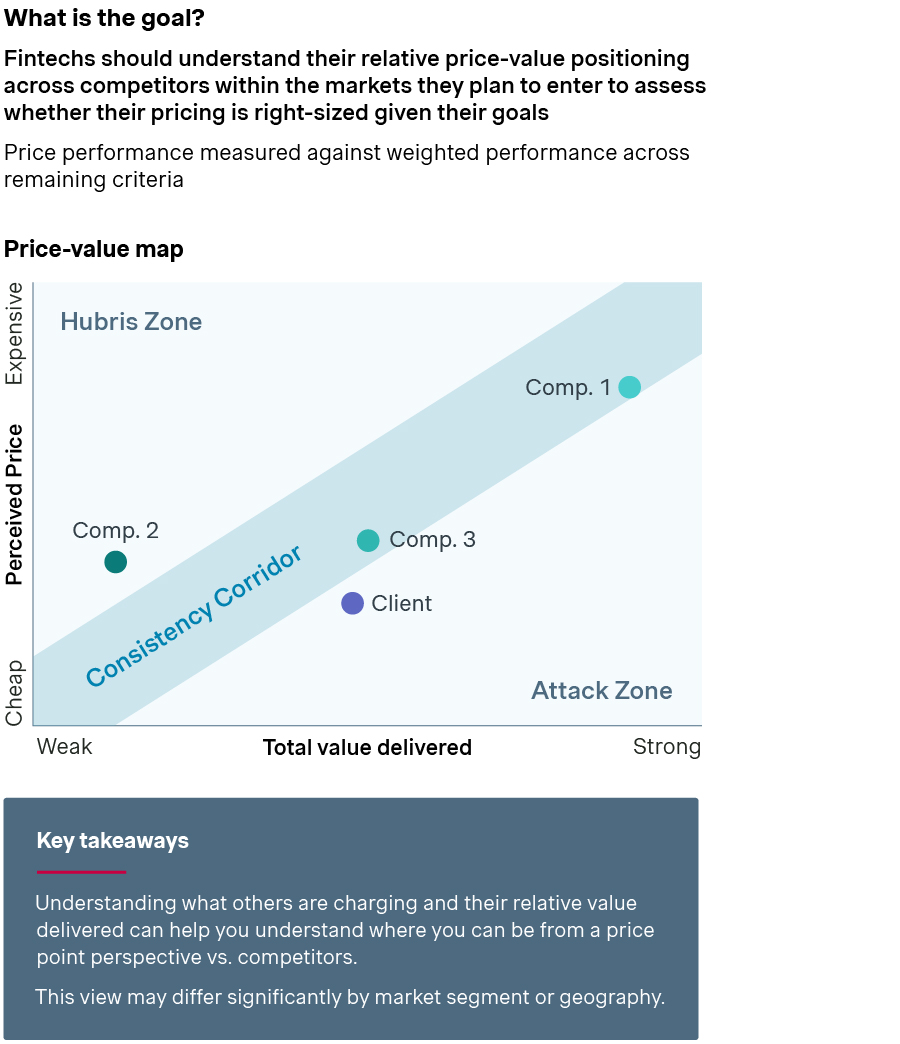

Position yourself along the price-value corridor

Pricing should be aligned with the perceived value customers believe they are receiving. In a nutshell, does the price accurately reflect the value delivered?

Fintechs risk entering the “Hubris Zone” (see Figure 2) when they charge premium prices for an offering the market perceives as delivering only moderate value. In this position, customers perceive the offering as overpriced relative to alternatives, resulting in lower win rates, longer sales cycles, increased discounting pressure, and greater vulnerability to competitors offering similar value at lower prices.

The initial objective for fintechs entering the US market is to establish a foothold by delivering compelling value at an attractive price point. This helps accelerate adoption and build customer references. As the company strengthens its market position, demonstrates outcomes, and builds brand credibility, it can progressively move up the price-value corridor toward premium pricing that is supported by a strong value proposition and recognized market leadership (see Figure 2).

Rethink monetization for AI capabilities

As AI capabilities become an increasingly important source of differentiation, fintechs must also rethink how they monetize innovation.

When pricing AI features and solutions, two dimensions are important: the degree of automation and measurable outcomes. AI solutions that fully replace human effort (full automation) and deliver clear measurable business impact will have the clearest path to monetization. By contrast, AI offerings that primarily augment the human worker, or where the value delivered is hard to quantify, may require hybrid, user-based, or subscription pricing models.

For disruptors seeking to implement outcome-based pricing for AI solutions, success depends on the ability to measure and attribute business outcomes within the client organization. This requires visibility on who is using the AI solution, how it is being used, and where it is creating value.

Fintech disruptors have an opportunity to introduce telemetry capabilities that capture both usage and impact data. This includes tracking business impact, such as improvements in forecasting accuracy, sales productivity, customer migration, operational efficiency, and other relevant KPIs.

Access to this data enables fintechs to quantify value delivered, support outcome-based pricing models, and engage customers in more meaningful value-based commercial discussions.

Achieving scale in a competitive market

Successfully entering the US market requires more than a differentiated product. Fintechs must make deliberate choices about where to compete, understand their right to win, align pricing with customer value, and find ways to measure outcomes. Those that can combine disciplined market selection with effective value capture will be best positioned to achieve sustainable scale in one of the world's most attractive and competitive fintech markets.

As a world-leading commercial and pricing growth specialist, Simon-Kucher supports clients across all key areas of monetization to help them accelerate growth.

Reach out to a team member today.