Executive summary

The semiconductor industry is approaching a trillion-dollar revenue milestone sooner than many expected. Recent forecasts place the market near $1T by 2026–2027. The more important shift is not the size of the market, but how this growth is being generated. Leaders who misread the moment will underperform, even in a rising market.

The key drivers are mix shift and pricing power, not broad unit expansion. Value is concentrating in the AI infrastructure stack, particularly high-value logic, advanced compute, high-bandwidth memory, and the networking silicon around them. As these categories occupy a larger share of spend, industry revenue rises even without a parallel surge in end-device units.

This concentration turns the trillion-dollar era into a commercial capability test. As industry growth becomes more concentrated, value capture will depend less on roadmap ambition and more on commercial execution. Winners translate differentiation and supply position into disciplined price realization, governed discounting, and deliberate portfolio and capacity allocation.

Pricing and mix must become an executive-owned operating system. This article lays out a practical agenda. Companies can build a CFO-grade fact base on price leakage, redesign segmentation around willingness to pay, institutionalize value-based pricing with guardrails, professionalize deal governance, and elevate mix and allocation decisions to the executive level. The call to action is direct: invest now in pricing sophistication and commercial muscle to capture margin on the way up and protect resilience when the cycle normalizes.

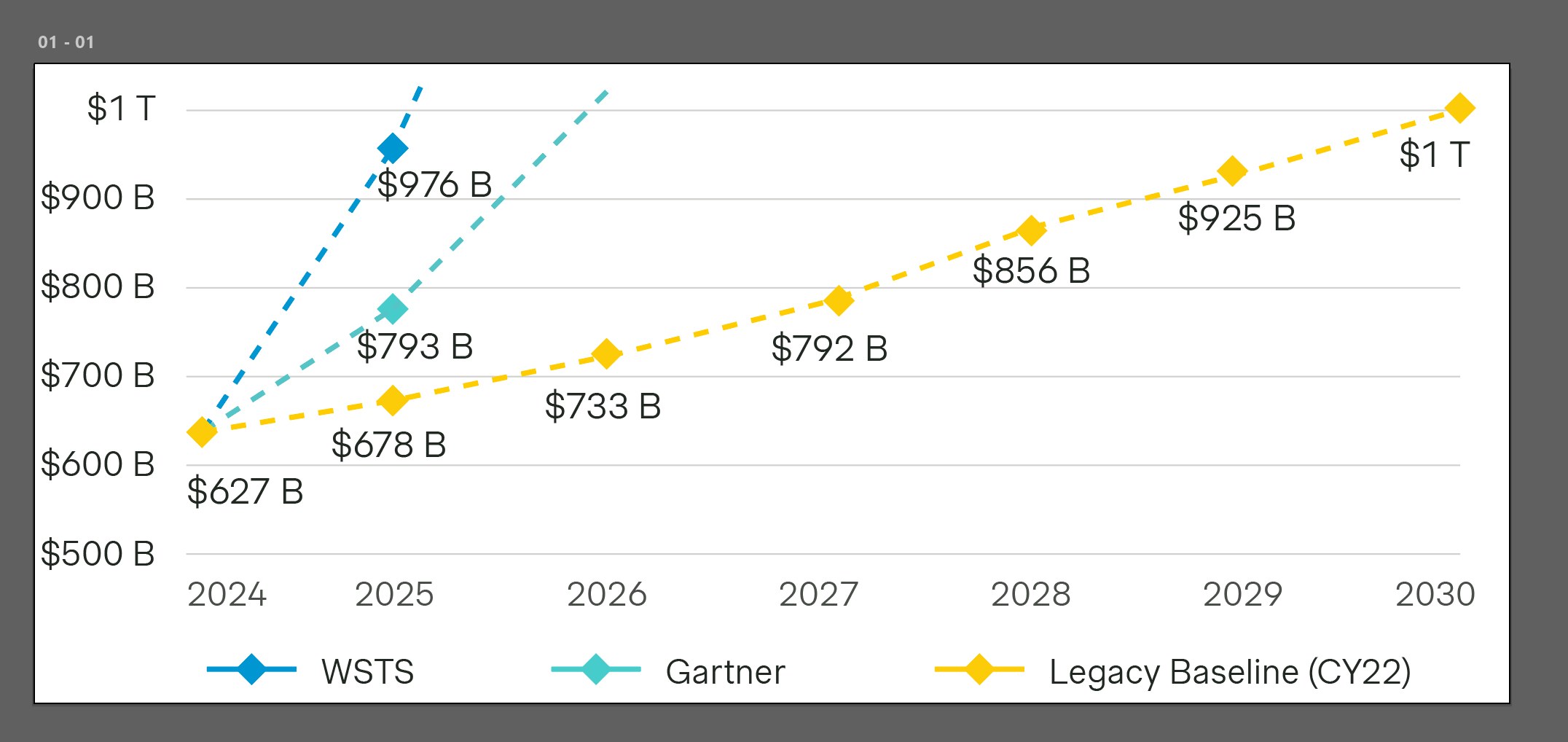

The milestone has pulled forward

As the semiconductor industry is about to cross $1 trillion, earlier mainstream outlooks projected crossing this threshold closer to 2030, but this timeline has been compressed. WSTS projects $975.5B in 2026, effectively within reach of $1 trillion. Gartner’s preliminary results put 2025 revenue at $793B, up 21% year over year.

The point is not whose model is “right,” rather that AI has accelerated value concentration faster than most assumptions. That shift changes how profit is created and captured.

Where the semiconductor growth is coming from: Not broad volume, but high-value categories

WSTS highlights that its upward revisions are mainly driven by logic and memory, boosted by AI-related applications and sustained demand in computing and data center infrastructure. This statement is telling as logic and memory are where mix and pricing power intersect to create outsized impact.

Gartner corroborates the same concentration dynamic from the demand side. It notes that AI semiconductors, including processors, high-bandwidth memory, and networking components, accounted for nearly one-third of total semiconductor sales in 2025. This is not the profile of a market expanding because “everything shipped more.” It is a market expanding because premium silicon is absorbing more dollars per system.

The CEO/CFO implication: Technology advantage is necessary, but not sufficient

In this environment, roadmaps create an advantage while commercial capability monetizes it. The leadership risk is to treat the trillion-dollar narrative as inevitable and therefore self-fulfilling. Category growth does not guarantee company-level value creation. When demand concentrates in a few value pools, the gap widens between companies that ship and those that capture.

Category growth does not guarantee company-level value creation.

That gap emerges in predictable places. When companies have a technological advantage and feel commercially unthreatened, governance of segmentation becomes weaker. Markets that can bear value-based pricing still default to cost-plus instincts. Discounts and exceptions are unmanaged. Contract terms transfer value to customers the moment suppliers have leverage. All of these things are at risk of being exposed when the market turns.

CEOs who combine commercial excellence with technological advantage attain real strategic control. For CFOs and sponsors, the same can be said of underwriting discipline. Pricing power is only real if it is realized.

Price and mix are no longer “commercial levers.” They are the operating system

In the same way that the consolidation of AI infrastructure stacks is dictating product direction, pricing should be treated as an integrated system spanning segmentation, contracting, discount governance, and allocation.

Three principles matter:

- Segment by willingness to pay. Account history is not a pricing strategy. Customers differ by switching costs, qualification depth, urgency, and the economic penalty of downtime. Pricing them as if they are equivalent is an unforced margin transfer.

- Price to customer economics. Cost-plus is a floor, not a compass. In AI infrastructure, customers manage quantifiable economic metrics: performance per watt, utilization, cost-per-inference, and time-to-deploy. Suppliers that price as “last year plus X” will under-monetize differentiation.

- Monetize certainty. Allocation and contracting are pricing instruments. Under constraint, the product is silicon plus certainty. Multi-year agreements, capacity reservation, indexation, take-or-pay, price guarantees, and supply assurance all monetize risk transfer. Treating these as bespoke negotiation artifacts is how value leaks at scale.

A practical agenda for semiconductor leaders and sponsors

The goal is a measurable system that expands upside during upcycles and protects economics when the cycle turns. Each action below should have an owner, a metric, and a cadence.

- Build a CFO-grade price realization fact base. Create a price waterfall by product family and top customers. Quantify leakage from exceptions, rebates, non-standard terms, and free value. Track exception rates and realized price versus defined corridors.

- Redesign segmentation around willingness to pay. Identify segments with high switching friction and high economic penalty for delay. Tighten price fences and governance where leverage is real. Track contribution margin by segment and win rate inside target corridors.

- Institutionalize value-based pricing and guardrails. Define corridor pricing, floors, and explicit trade-offs. Require documented value exchange for any deviation. Track percentage of deals within corridor and the value exchanged per exception.

- Professionalize deal governance. Establish a deal desk with authority and clear approval thresholds. Align incentives to realized price and contribution margin, not volume of shipments alone. Track discount leakage and post-deal margin variance.

- Make mix and allocation an executive decision. Under constraint, allocation is strategy. Decide where scarce supply goes based on value and strategic position. Be willing to walk away from revenue that destroys pricing integrity. Track allocation ROI and the share of constrained capacity deployed to priority segments.

A useful implementation horizon is 60–90 days for diagnosis and pilots, followed by scaling. The hardest part is not analytics; it is governance and consistency.

Conclusion

The industry is approaching the trillion-dollar mark faster than many expected. Value is concentrating in the AI stack. The question for semiconductor CEOs, CFOs, and financial sponsors is whether they build operating systems to capture disproportionate margin in the upswing and sustain advantage once conditions normalize.

The trillion-dollar era will create winners and passengers. Winners will not simply ship differentiated silicon. They will run pricing and mix as an executive operating system, with measurable governance and discipline. Companies can grow revenue, but lacking this system means losing the profit pool to better monetizers.

Contributing author: Emery Engling

With two decades of semiconductor experience, Simon-Kucher has supported industry leaders through transformative cycles - from the rise of the data economy to AI acceleration and the global compute surge. We are well-positioned to anticipate what comes next and excited to serve as a strategic partner in shaping it.