Recap

The 2000s ushered in the age of mobile computing, with smartphones and wireless broadband reshaping semiconductor demand. The collapse of the dot-com bubble led to early pricing struggles, but by mid-decade, surging demand for mobile processors and networking chips fueled industry growth. The shift from desktop to mobile required new pricing strategies, with premium SoCs commanding high margins while competition in commoditized segments drove costs lower. The rise of 300 mm wafers and sub-100 nm nodes cut manufacturing costs but required immense capital investment, reinforcing the industry's reliance on high-volume production to maintain profitability.

Introduction

The 2010s ushered in a semiconductor renaissance fueled by two seismic shifts in the tech landscape. First, smartphones and tablets exploded into global ubiquity, transforming the mobile device from a communication accessory to a personal computing hub. Second, data centers and cloud computing scaled at an unprecedented pace, driven by the rising tide of social media, e-commerce, video streaming, and enterprise services delivered online. The decade also witnessed the nascent boom of artificial intelligence (AI) and machine learning (ML) applications—demanding specialized computing horsepower well beyond traditional CPU architectures.

Amid these robust tailwinds, the semiconductor industry experienced intense demand for both high-performance and power-efficient chips. Foundries raced to shrink process nodes from 28 nm down to 7 nm (and beyond by the decade’s close), spending billions on cutting-edge fab equipment. Companies adapted by consolidating, forging new alliances, and exploring novel architectures, while contending with ever-tighter margins in commoditized segments. This article explores the intricate pricing dynamics that emerged in response to hyper-growth in mobile devices, cloud-scale data centers, and the dawn of AI accelerators—revealing how technology’s center of gravity decisively shifted to a world of connected, intelligent devices.

Smartphones take the lead in consumer electronics

From niche to dominance

Although smartphones emerged in the mid-to-late 2000s, the 2010s truly cemented their place as the world’s primary personal computing devices. Apple’s iPhone and devices running Google’s Android OS rapidly captured billions of users across every continent. The popularity of mobile social media, on-demand apps, and streaming services demanded ever-more-powerful mobile chips.

Systems-on-a-Chip (SoCs)

Companies like Qualcomm, Apple, Samsung, and MediaTek poured resources into designing SoCs that integrated CPU, GPU, modem, and other specialized processing blocks (e.g., image signal processors). Each subsequent generation aimed for higher performance, longer battery life, and advanced features such as machine learning accelerators.

Mobile-first pricing

High-end smartphones became status symbols in many markets. Premium SoC vendors could charge elevated prices for flagship chips, banking on OEMs’ willingness to pay for top-tier performance and features. Meanwhile, budget smartphones demanded cost-optimized SoCs, pushing suppliers to streamline designs and negotiate aggressive volume discounts.

Competition and differentiation

As the market for smartphones ballooned, chipmakers sought to differentiate:

Apple’s vertical integration: Apple developed its own Ax series chips, customizing them for iOS devices. This closed ecosystem let Apple optimize power/performance and command a significant price premium, translating into high average selling prices (ASP) for iPhones.

Qualcomm’s modem expertise: Qualcomm became synonymous with high-performance mobile connectivity, leveraging its patent portfolio to secure robust royalty streams. Its Snapdragon SoCs often bundled leading-edge modems, which justified higher ASPs than purely commodity solutions.

Emerging suppliers: MediaTek, HiSilicon (Huawei), and Spreadtrum (later Unisoc) targeted mid-tier and low-tier markets, balancing moderate performance with affordability. This segmentation resulted in layered pricing, where flagship SoCs might fetch ten times the price of mass-market alternatives.

Data centers scale up: CPUs, GPUs, and beyond

The cloud computing surge

The 2010s witnessed an explosion in cloud services and data center construction. Hyperscale providers—Amazon (AWS), Microsoft (Azure), Google Cloud, Alibaba Cloud—invested aggressively in server infrastructure to host everything from streaming media to enterprise SaaS (Software-as-a-Service).

Server CPUs: Intel’s Xeon line dominated much of this market. AMD challenged intermittently, particularly after launching its Zen architecture (2017), which delivered competitive performance at lower cost. This reignited CPU price wars in the data center segment.

Memory and storage: DRAM, NAND flash, and emerging storage-class memory solutions soared in demand. Commodity-like pricing cycles persisted, but scale gave top manufacturers (Samsung, SK hynix, Micron) leverage to invest in next-gen memory technologies.

The GPU renaissance and AI

While GPUs had long been crucial for gaming, the 2010s saw them emerge as the go-to accelerators for AI/ML tasks. NVIDIA capitalized on the GPU’s parallel processing capabilities, quickly adapting them for machine learning frameworks like CUDA. As AI adoption grew, data centers needed specialized GPU-based clusters to train and run large neural networks.

Pricing power in AI: Because of their unparalleled performance in training deep learning models, GPUs commanded high margins—sometimes selling for thousands of dollars per board. AI startups and major cloud providers alike were willing to pay premium prices for performance gains that could significantly reduce training times.

Specialized accelerators: Google introduced its TPU (Tensor Processing Unit) for internal data centers, while other players explored custom ASICs for ML workloads. These specialized chips, though niche, underscored a new pricing model built around efficiency gains in AI, not just raw transistor counts.

Major industry events shaping pricing in the 2010s

Continued process node shrinks

The 2010s saw an aggressive race from 28 nm down to 7 nm processes, with Taiwan Semiconductor Manufacturing Company (TSMC), Samsung, and Intel vying for node leadership. As lithography approached extreme ultraviolet (EUV) for sub-10 nm nodes, costs for new fabs soared.

Impact on pricing: Smaller nodes enabled greater performance and lower power consumption, crucial for both mobile and high-performance computing. However, R&D and fab construction costs rose exponentially, pressuring foundries and IDMs to maintain high utilization. Manufacturers passed these costs on to fabless customers through wafer pricing—especially at the “bleeding edge” nodes.

Mergers and acquisitions

Semiconductor consolidation continued as companies sought scale and complementary portfolios. Examples include Avago’s acquisition of Broadcom (forming Broadcom Inc.), SoftBank’s purchase of ARM, and multiple smaller merges in the analog and mixed-signal spaces.

Impact on pricing: M&A often reduced the number of direct competitors, stabilizing prices in certain segments. Larger, more diversified companies could spread risk across multiple product lines, sometimes allowing them to sustain more competitive pricing in markets where they aimed to gain share.

Trade tensions and geopolitics

Late in the decade, US–China trade tensions roiled global supply chains. Restrictions on technology exports to certain Chinese firms, along with tariff uncertainties, forced many semiconductor companies to rethink sourcing and production footprints.

Impact on pricing: In some cases, geopolitical frictions added cost via tariffs or forced relocations of assembly/test facilities. This complexity translated into occasional price hikes or pressured margins if suppliers chose to absorb costs.

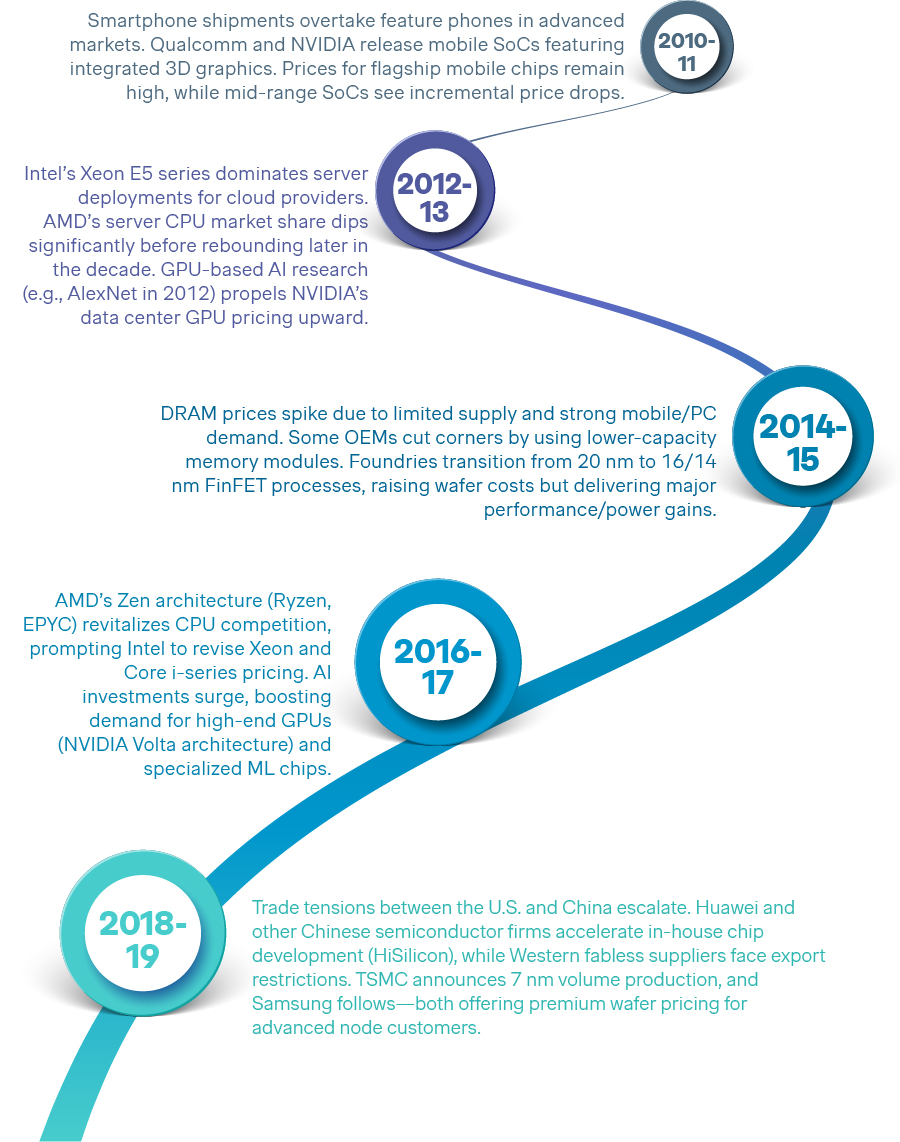

Timeline of pricing milestones in the 2010s

Manufacturing cost structures: beyond the silicon

By the end of the 2010s, semiconductor cost structures became a complex tapestry where raw silicon was just one piece:

Advanced packaging

Techniques like 2.5D/3D packaging, chiplets, and TSV (through-silicon vias) gained ground, enabling higher density and modular designs. While beneficial for performance, these methods could significantly increase back-end packaging costs.

Intellectual property (IP) licensing

As SoCs became more complex, licensing IP blocks (e.g., ARM CPU cores, Imagination GPUs, specialized AI cores) formed a large portion of chip development expenses. Royalties often factored into final device pricing.

Design verification and software

The cost of validating complex chips with billions of transistors soared. Additionally, robust software ecosystems—including firmware, driver stacks, and ML libraries—became integral to a chip’s value proposition, justifying higher ASP for thoroughly integrated solutions.

Notable pricing models of the 2010s

Tiered mobile SoCs

Smartphone OEMs segmented their product lines into flagships, mid-range, and budget devices, each requiring different SoC performance profiles:

Flagship SoCs: Often built on the latest node (e.g., 7 nm FinFET), equipped with powerful CPUs, GPUs, and AI engines. These commanded premium prices—sometimes $50–$70 per chip or higher, depending on volume.

Mid-range SoCs: Prior-generation process nodes (e.g., 10 nm or 14 nm) and scaled-back feature sets reduced costs. ASPs typically ranged from $15–$30.

AI acceleration premiums

AI accelerators (GPUs, FPGAs, dedicated ASICs) found homes in data centers, edge devices, and automotive markets (e.g., self-driving systems). With comparatively fewer direct competitors—especially at the high end—these accelerators carried outsized margins. NVIDIA, for instance, charged thousands of dollars for high-performance data center GPUs, leveraging performance leadership in AI training.

Foundry and OEM partnerships

Leading foundries provided early access to new nodes for top customers, often with higher wafer costs. In exchange, those customers secured capacity priority—a must-have amid tight supply conditions. Volume agreements included negotiated price breaks for large, consistent orders, allowing Apple, Qualcomm, and other heavyweights to scale quickly at relatively stable cost.

Average selling price (ASP) trend of high-end smartphone SoCs (2010–2019)

In this scenario:

2013: A jump occurs with the transition to 28 nm or 20 nm, offering significant performance gains.

2017: Another rise appears with the introduction of advanced AI cores, fueling higher pricing.

Late decade: By 2019, 7 nm chips push performance further, commanding a premium.

Conclusion: the 2010s—when semiconductors became essential infrastructure

The semiconductor industry in the 2010s became the backbone of a hyper-connected world. Smartphones went from high-tech curiosities to indispensable tools, AI transformed business workflows and consumer experiences, and data centers ballooned to house the world’s digital ecosystem. Fueled by these trends, chipmakers experienced accelerating demand but also faced the immense challenges of advanced node complexity, multi-billion-dollar fab investments, and fierce global competition.

Pricing models evolved to reflect market segmentation, technological leaps, and strategic partnerships. Premium segments—whether flagship smartphone SoCs or data center accelerators—commanded high margins, especially when backed by significant performance differentiation. At the same time, large swathes of the market operated under razor-thin margins, where cost efficiencies and scale determined survival.

Key lessons

The 2010s illustrate the power of innovation, branding, and scale in setting semiconductor prices. Firms that controlled cutting-edge IP, led in advanced nodes, or offered differentiated solutions for emerging applications reaped the greatest rewards. Yet, the landscape was far from static—sudden architectural breakthroughs or geopolitical shifts could upend pricing norms overnight. As we turn our attention to the final installment covering the 2020s (and beyond), the stage is set for even more dramatic change. The rise of AI at the edge, 5G networks, and continued node shrinks toward 3 nm and below will bring fresh challenges and opportunities, shaping the next chapter in semiconductor pricing evolution.