This article looks ahead to how semiconductor pricing might evolve from the transformation of the 2020s through the innovation-saturated 2030s and into the speculative frontiers of the 2040s. It integrates pandemic-era supply shocks, AI’s explosion across cloud and edge, advanced-node cost inflation, regionalized supply chains, and prospective post-silicon breakthroughs. Along the way, it highlights how pricing strategies respond to capital intensity, yield complexity, geopolitical forces, sustainability pressures, and potential shifts in business models like “chip-as-a-service”.

Reflecting on the 2010s

The 2010s saw smartphones, cloud, and AI propel demand. Process nodes shrank from 28 nm to 7 nm, capital costs ballooned, and the gap widened between commodity components (tight margins) and performance parts (premium pricing). Rising US – China trade conflicts foreshadowed the next decade’s challenges.

Introducing the 2020’s: Pandemic, supply chain disruptions and AI-driven demand

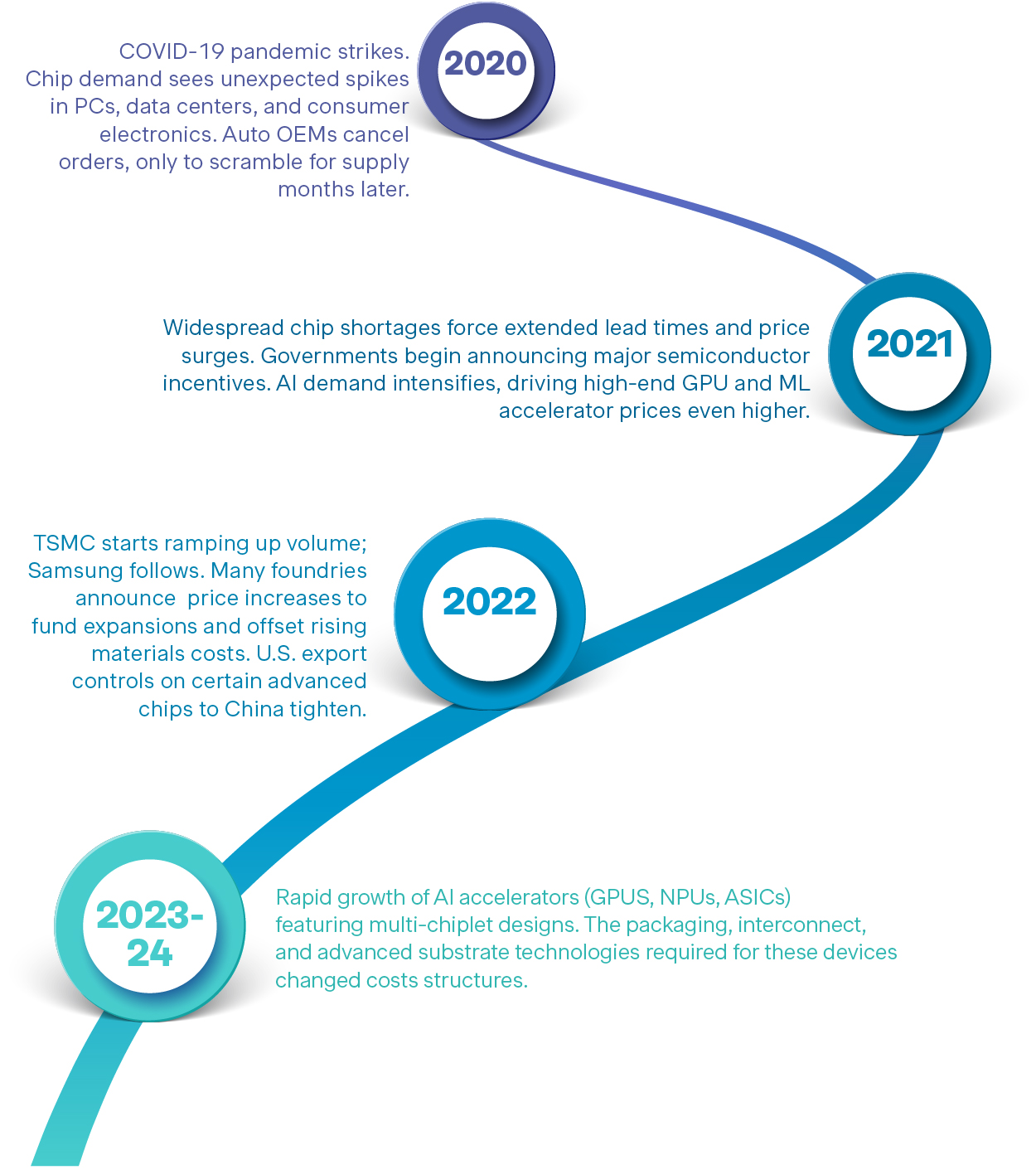

The 2020s opened with COVID19 and consumer behavior changed practically overnight. COVID-19 upended demand patterns and supply chains. Remote work, distance learning, and at home entertainment surged, while 5G, AI, and HPC kept pushing technology forward. Pricing quickly reflected scarcity, risk, and the value of guaranteed capacity. This new era of demand and disruption began to look like this:

Pandemic fueled surge: Laptops, tablets, webcams, home networking, game consoles, and cloud infrastructure spiked.

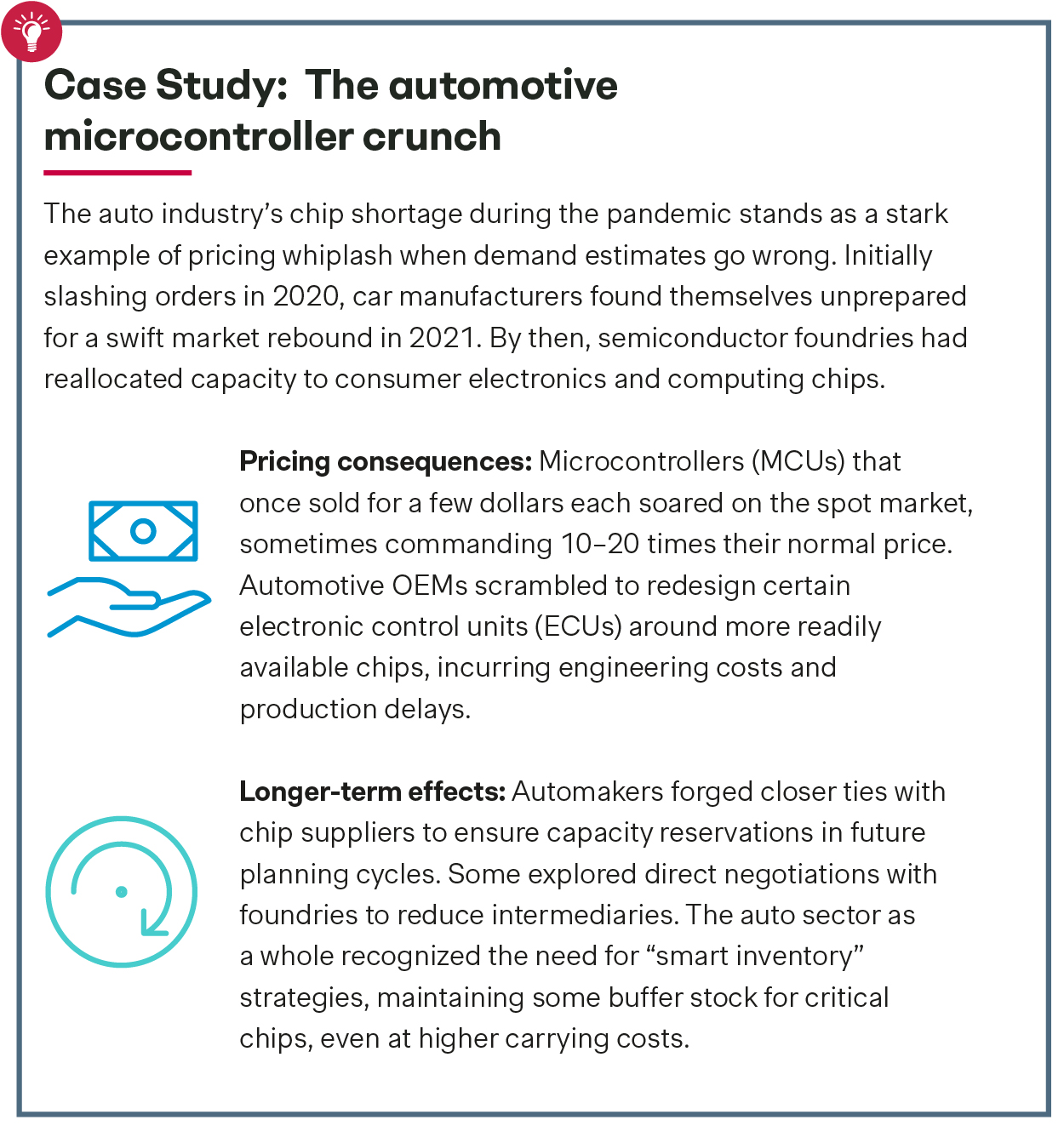

Auto industry missteps. Automakers cut chip orders expecting a slump, then rebounded into shortages, triggering factory stoppages and price hikes in vehicles and automotive electronics.

Global chip shortage: By mid-2021, lead times extended across nearly every category. Panic buying and double ordering tightened supply.

Impact on pricing: With supply lagging and surging demand, prices for many chips soared. Commodity parts (like automotive microcontrollers) experienced dramatic markups on the open market. Even leading-edge chips faced inflated pricing as companies jockeyed for the scarce manufacturing slots at 5 nm and 7 nm nodes.

Strategic overhauls: Governments labeled semiconductors “critical infrastructure.” Incentives (e.g., U.S. CHIPS Act, European Chips Act, etc.) targeted onshoring and diversification. Near term tightness sustained elevated pricing in many segments.

Heightened geopolitical tensions

Geopolitical challenges heavily influenced the semiconductor industry:

US – China tech rivalry: Strained US - China relations escalated in the early 2020s, influencing everything from export controls on advanced chips to blacklists of specific Chinese tech firms. On the other side, China’s government pushed a major “Made in China” initiative to bolster domestic semiconductor capacity.

Other trade reconfigurations: Mounting geopolitical frictions, combined with pandemic-related logistic snarls, prompted many industry players to “reshore” or diversify their supply chains.

Technology drivers: AI, HPC, and 5G

Alongside geopolitical changes, technological advancements reshaped chip demand and pricing:

AI continues its ascent: LLMs and generative models scaled; NVIDIA continues to lead in data‑center AI while AMD, Intel, and startups added competition in specialized AI chips or novel architectures. Edge AI neural processing units, or NPU’s, have become standard in phones/IoT with premiums for robotics, autonomous vehicles (AV), and security.

High performance computing: CPUs and accelerators are duking it out for simulation, analytics, and AI. Tiered SKU structures let vendors charge thousands per chip at the high end while using midrange for volume.

5G rollout: Base stations, RF frontends, and phased arrays are driving complexity and support solid margins for some vendors despite supplier competition.

Timeline: Key pricing milestones in the early 2020s

Changing cost structures and rising input prices

The semiconductor industry is experiencing significant shifts in cost drivers, from expensive advanced manufacturing equipment to rising input prices, prompting innovative risk-sharing partnerships.

Extreme ultraviolet (EUV) lithography: EUV systems from ASML, essential for advanced nodes, cost hundreds of millions each, while foundries are recouping via higher wafer prices and long-term capacity deals.

Input cost inflation: Specialty gases, rare metals, substrates, and logistics have seen spikes; meanwhile, packaging constraints are adding friction.

Risk sharing models: Deep partnerships are exchanging co-investment for guaranteed wafers and preferential pricing.

Pricing approaches and balancing advanced nodes with mature technologies

To manage these growing production expenses, companies adopt differentiated pricing approaches that balance premium charges for cutting-edge nodes with stable pricing for mature, high-volume components.

Premium for advanced nodes: 5 nm/3 nm access commands higher wafer/mask costs; first wave customers (e.g., Apple, AMD, NVIDIA, Qualcomm) translate those costs into end product pricing.

Commodity vs. specialized: Mature nodes (28/40/65 nm) remain essential yet are more cautiously expanded to avoid boom bust cycles. AI specific SKU’s price above commodity levels, tiered for workload and TCO.

Early 2020s takeaway

The early 2020s show that in this era of globalization, pandemics, and political tensions, semiconductor pricing has become intertwined with far more than raw production costs. Although each decade brought its own lessons, the early 2020s remind us that agility, foresight, and robust partnerships are more vital than ever to thrive in this indispensable, yet deeply complex industry.

Beyond the mid-2020s and the future of semiconductor pricing

The technological horizon and pushing past 2 nm

NextGen nodes. By the start of the decade 3 nm will likely be at volume, with 2 nm and 1.4 nm following with steeper lithography, mask, and materials challenges.

- Capital intensiveness: Currently, a state-of-the-art fab could cost upwards of $20 billion to construct and equip. By the late 2020s and beyond, those figures may climb higher due to new lithography tools, advanced wafer-handling robotics, and deeper R&D spending.

- Yield complexity: Approaching physical/quantum limits raises defect sensitivity. AI driven‑ process control and aggressive design for manufacturing, or DFM, will become mandatory to hit economic yields.

- Anticipated pricing impact: Bleeding edge wafers will carry substantial premiums, and many segments may favor mature nodes (16/28/45 nm+) for cost stability and proven reliability, especially auto, industrial, and IoT.

New computing paradigms

Quantum’s niche expansion: Usage may concentrate in cryptography, molecular simulations, and optimization problems. Pricing favors cloud delivered access and ultra-premium hardware for specialized buyers.

Neuromorphic and photonic processers: Neuromorphic chips, designed to mimic brain-like architectures, and photonic processors (leveraging light instead of electrons) have both garnered R&D attention in the 2020s. By the late 2020s, we may see early commercial scale-out of these technologies in AI inference, sensor fusion, and specialized HPC tasks.

- Value-based pricing: If neuromorphic and photonic solutions deliver order-of-magnitude gains in power efficiency or latency for specific workloads, they could justify premium pricing comparable to or higher than AI GPUs in the late 2010s.

- Incremental commoditization: Over time, as multiple companies develop similar solutions, competition may drive down ASPs and mirror how GPUs moved from niche to mainstream over two decades.

AI acceleration in semiconductors

Data center AI - scaling model sizes: LLMs and advanced generative AI systems’ sizes could leap again (may grow 100x bigger or more) while specialized training/inference ASICs and premium GPU boards fetch five figure prices per unit/board. Cloud subscriptions obscure chip ASPs but embed hardware premiums.

Edge AI - low power, high value: Consumer SoCs integrate AI with volume driven ASP decline. Industrial, medical, and auto chips command durable premiums for safety, reliability, and certification. Wearables, smartphones, and home assistants will continue to see moderate, volume-driven ASP declines

Semiconductor supply chains & geopolitical changes

Ongoing regionalization: Multiple hubs (Americas, Europe, Asia) expand capacity and mandate redundancy for critical sectors, trading higher baseline costs for security of supply.

Shifting trade regulations: Although the intensity of US – China tensions or other geopolitical frictions is unpredictable, such rivalries could persist. This could lead to continued export restrictions and licensing around dual-use AI/encryption persisting. Additionally, “regional variants” would raise development overhead, while “secure supply chain” labels would add risk-based premiums.

Innovations in semiconductor manufacturing

3D ICs & chiplets: Modular die markets will emerge, with per-chiplet pricing and premium packaging fees (2.5D/3D) for bandwidth and form‑factor advantages.

NextGen materials: Carbon nanotubes and 2D semis may enter pilots. Novel materials often require small-batch, specialized handling, creating initial supply constraints. Early adopters may pay steep premiums for “carbon transistor” chips that promise leaps in energy efficiency or speed.

Macro and market pressures’ growing role in semiconductor pricing

Energy and sustainability: As chips grow more powerful and data centers become gargantuan, energy consumption looms large. Green fabs, renewable sourcing, and efficiency standards allow eco-labeled premium positioning, especially for hyperscale buyers with net zero pledges.

Cyclicality: Climate disruptions, currency swings, and new pandemics keep volatility alive, while ASPs swing with capacity/sentiment.

Perspectives on the future

The enduring theme for the mid 2020s and beyond, and indeed for the entire semiconductor historical arc, is that technology leaps alone aren’t enough. While we can’t know all the nuances the future will bring, we can be certain of one reality: the essential role of semiconductors in powering virtually all aspects of modern life. As history has shown for over eight decades, whenever technology and demand converge, semiconductor pricing evolves to meet a dynamic market head-on, combining the cutting-edge with the pragmatic in pursuit of the industry’s next great leap.

Cross‑ decade themes & pricing implications

- Capital intensity → premium access: Every node/packaging leap lifts capex; first wave access retains steep premiums.

- Mature node resilience: 28/40/65 nm and similar nodes anchor auto/industrial/IoT with stable yields and cost—avoiding over migration to bleeding edge.

- Packaging as a profit center: 2.5D/3D and chiplets shift value capture from lithography alone to integration and interconnect.

- Geopolitics baked into price: Export regimes, onshoring, and redundancy add structural costs, and customer willingness to pay for “secure supply.”

- AI everywhere, pricing everywhere: From five figure datacenter boards to cents per unit edge sensors, AI stretches the pricing barbell.

- Sustainability as a differentiator: Eco labeled capacity and lifecycle contracting enable pricing power with net zero buyers.

- Services & IP stacks: CaaS models and layered royalties transform onetime ASPs into recurring ARPU.

Key semiconductor takeaways by decade

- 2020s: Pricing set by shock management: capacity guarantees, geopolitical permissions, and inflationary inputs dominate alongside AI/HPC premiums.

- 2030s and beyond: Pricing could broaden to include packaging modularity, regional assurance, and energy credentials, while mature nodes remain sticky.

Innovation, uncertainty, and opportunity for the semiconductor industry

From COVID era shortages to chiplet rich architectures and post-silicon experiments, semiconductor pricing is a choreography of technology, capital, regulation, and demand. The coming decades reward those who treat pricing not as a simple passthrough of wafer costs but as a strategic portfolio: premium access where performance is scarce, resilient mature node supply for longtail volume, eco-efficient positioning for regulated buyers, and service/IP models that smooth cycles. Whatever the device or decade, the winners will align R&D bets, supply chain design, and pricing mechanics to a world where semiconductors remain the essential substrate of modern life.

Whether you have questions, want to share your perspective, or explore partnerships, our team would be happy to engage in a discussion about the future of semiconductors, and the role pricing plays in current times.