Recap

By the 1980s, semiconductors had become a global industry, expanding beyond computing into consumer electronics, telecommunications, and industrial automation. The decade saw the rise of the microprocessor, memory market fluctuations, and the entry of new manufacturing regions like South Korea and Taiwan. U.S.-Japan trade tensions led to government intervention, while strategic pricing models—such as value-based differentiation and cost reductions through process node advances—became standard. The formation of SEMATECH and the foundry model’s emergence hinted at the shifts that would define the 1990s, where the internet and globalization would further reshape the industry.

Introduction

The 1990s emerged as a transformative era for the semiconductor industry—one that brought the dynamics of globalization, consolidation, and unprecedented demand from the burgeoning internet age. Where the 1980s introduced geopolitical complexities and heightened competition, the 1990s amplified these forces amid rapid technological progress. The decade witnessed the mainstreaming of personal computing, the birth of the World Wide Web, and a surge in mobile communications. Together, these trends dramatically increased the appetite for powerful yet cost-effective semiconductor devices, propelling the industry into new pricing frontiers.

At the same time, manufacturers grappled with balancing declining cost-per-transistor against rising capital expenditures for ever-larger fabs and advanced process nodes. Consolidation among major players, coupled with the continued ascent of Asian manufacturers—most notably in South Korea and Taiwan—brought a new wave of global competition. As this article explores, the interplay between technological leaps, market forces, and strategic partnerships redefined semiconductor pricing in ways that echo through today’s industry. We’ll examine how developments like system-on-a-chip (SoC) integration, the foundry model, and the internet boom shaped an evolving pricing landscape that strived to accommodate both soaring demand and intense cost pressures.

Tech boom meets semiconductors: Market drivers of the 1990s

Personal computing matures

By the start of the 1990s, personal computing had firmly taken root. Microsoft’s Windows operating system and Intel’s x86 architecture (often dubbed “Wintel”) dominated the desktop PC market, while Apple continued to maintain a dedicated albeit smaller following. From corporate offices to households, computers were no longer a novelty.

CPU performance race

Intel (with its Pentium line) and competitors such as AMD and Cyrix pushed microprocessor clock speeds higher every year. The “Megahertz Wars” accelerated, leading to rapidly improving performance at decreasing cost per MIPS (Million Instructions Per Second).

Desktop and mobile markets

Laptops and early mobile computing devices emerged, driving demand for low-power chipsets and specialized packaging. This growing product diversity influenced pricing structures, as premium performance segments could command higher margins while more price-sensitive consumer segments required lean cost models.

The internet and networking boom

Arguably, the most significant catalyst of the decade was the rise of the internet and the World Wide Web. As commercial web services and electronic mail became widespread, the demand for servers, routers, and networking hardware soared.

Server processors: Companies like Intel, Sun Microsystems (SPARC), IBM (PowerPC), and Digital Equipment Corporation (Alpha) vied for supremacy in the lucrative server CPU space. High-performance chips for data centers could command premium prices, with customers paying extra for faster clock speeds, larger caches, and reliability features.

Networking equipment: Cisco and other network infrastructure vendors fueled demand for specialized ASICs (Application-Specific Integrated Circuits) that handled packet routing and switching at ever-increasing speeds. This domain offered robust margins for semiconductor suppliers adept at customizing designs.

Mobile and communications growth

While cellular phones were still evolving from “bricks” into more compact devices, the 1990s ushered in 2G digital standards (GSM, CDMA). This shift toward digital mobile technology required baseband processors, power amplifiers, RF front-ends, and memory devices specifically tailored for wireless communications. Though initially a small slice of the semiconductor market compared to PCs, mobile communications pointed to a major growth avenue—one that pricing strategies would need to accommodate in full force by the early 2000s.

Major industry events and pricing implications

The foundry model takes hold

Taiwan Semiconductor Manufacturing Company (TSMC), founded in 1987, rapidly expanded throughout the 1990s as one of the first pure-play semiconductor foundries. Competitors such as UMC (United Microelectronics Corporation) in Taiwan and Chartered Semiconductor in Singapore also ramped up capacity.

Impact on pricing: Fabless companies like Qualcomm, Broadcom, and NVIDIA (founded in 1993) no longer needed to invest in their own fabs to produce cutting-edge chips. This separation of design and manufacturing lowered barriers to entry for design-focused firms, intensifying competition in many product segments. Over time, as foundries vied for business, they refined their cost structures to offer volume pricing, further driving down per-unit costs.

Rapid process node shrinks

The industry pushed from 1-micron geometries at the dawn of the decade down to 0.35-micron (350 nm) or even 0.25-micron processes by its close. Each node transition demanded state-of-the-art lithography, more advanced cleanrooms, and enormous capital investment.

Impact on pricing: Smaller geometries enabled higher transistor densities, directly reducing cost per transistor. Yet the soaring cost of fabs—often exceeding a billion dollars—introduced greater financial risk. Pricing strategies had to account for faster product lifecycles; chips needed to pay back the fab investment within a shorter window before the next node shrink arrived.

Consolidations and acquisitions

The 1990s saw a wave of mergers and acquisitions among semiconductor companies. Some consolidated to gain scale and reduce redundant R&D costs, while others sought to diversify product lines.

Impact on pricing: Larger conglomerates could leverage synergies in manufacturing and sales, offering competitive pricing across multiple markets (processors, memory, ASICs, etc.). In some cases, consolidation reduced market fragmentation, stabilizing prices in certain segments—particularly if it helped avoid the overcapacity issues that had led to price collapses in previous eras.

Asian financial crisis (1997)

Late in the decade, the Asian financial crisis rattled several key economies in the region, notably South Korea. This turmoil temporarily curtailed capital spending and dampened demand for consumer electronics. Korean giants like Samsung faced debt challenges but ultimately emerged with refined cost structures and a renewed focus on global markets.

Impact on pricing: For a time, memory prices fell as manufacturers scrambled to maintain cash flow, but the short-term oversupply also fueled cyclical price recoveries. The crisis underscored how macroeconomic events could swiftly reshape semiconductor pricing, especially in commodity-like segments.

Cost structures and yield imperatives in the 1990s

As process nodes shrank and volumes soared, manufacturing cost structures became a balancing act of higher capital expenditures offset by the potential for massive volume sales.

Transition to 200 mm (8-inch) wafers

In the mid-1990s, many leading-edge fabs migrated from 6-inch to 8-inch wafers. This boosted throughput significantly, but the retooling expenses were enormous. Those who executed the transition smoothly gained a cost advantage, enabling more aggressive price competition.

Sophisticated EDA (electronic design automation)

Design complexity grew exponentially with increasing transistor counts. Improved EDA tools helped designers manage larger-scale integrations (like SoCs), but these tools came at a cost—one that fabless companies ultimately baked into product pricing. Still, better design verification and optimization often enhanced yields, lowering the overall manufacturing cost per good die.

Packaging and test automation

Ball Grid Array (BGA) packages gained popularity, particularly in higher-pin-count devices like microprocessors, ASICs, and GPUs. Automated test handlers became more advanced, reducing both test time and labor. These incremental gains in packaging and test efficiency, while not as dramatic as fab-level changes, contributed to lower overall costs.

Notable pricing models: Premium brands, commodity memory, and foundry contracts

Premium brands in microprocessors

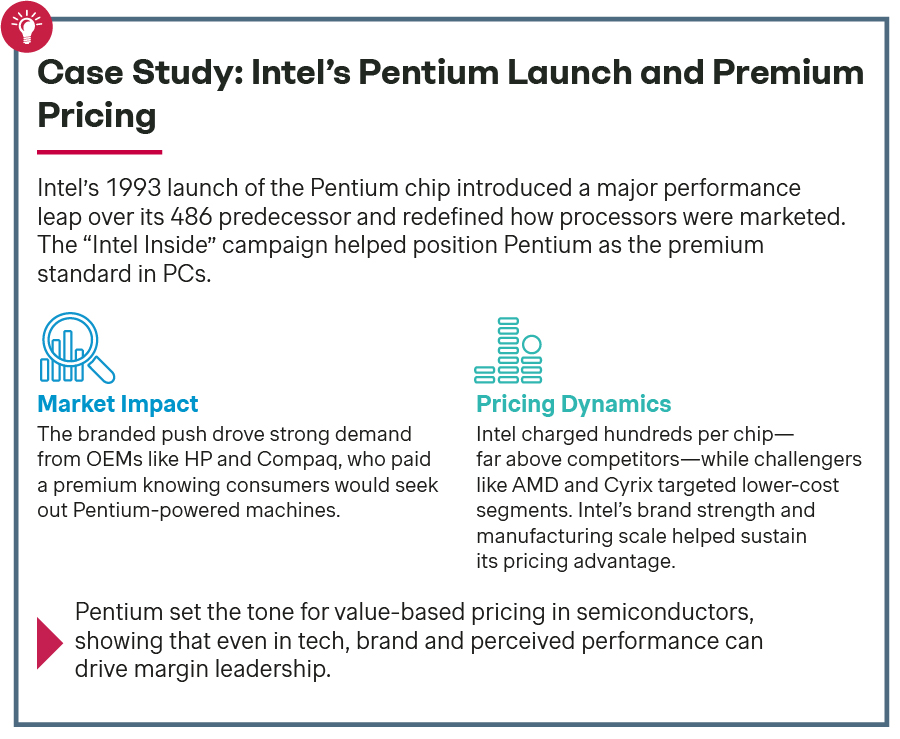

Intel’s approach in the 1990s exemplified a premium brand strategy. Its Pentium line—later Pentium Pro, Pentium II, and Pentium III—regularly commanded above-average prices, justified by marketing, perceived performance leadership, and brand loyalty. Competitors like AMD sought to undercut Intel’s pricing, positioning “Intel-equivalent” products at slightly lower price points to capture cost-conscious segments.

Commoditized DRAM and flash

Memory, especially DRAM, continued to behave like a commodity market with cyclical price swings. Manufacturers often operated on razor-thin margins, hoping to recoup investments during periods of tight supply. NAND flash also started to gain ground for specific applications, though it had not yet exploded into the massive consumer market that smartphones and solid-state drives would later create.

Foundry engagement and volume seals

As the decade progressed, fabless companies entered into volume-based foundry contracts. Foundries offered tiered pricing depending on wafer starts per month. Customers who reserved significant capacity could negotiate better rates, which in turn helped them offer more competitive chip prices downstream.

Risk sharing: Some deals included cost-sharing mechanisms for yield improvements. If a fabless firm required a cutting-edge process, the foundry might charge a premium until yields stabilized.

Capacity reservations: Customers paid up-front fees to guarantee fab space, insulating them from the risk of capacity shortages. This arrangement, though expensive initially, often paid off by ensuring a steady flow of product during peak demand periods (e.g., holiday seasons, new product launches).

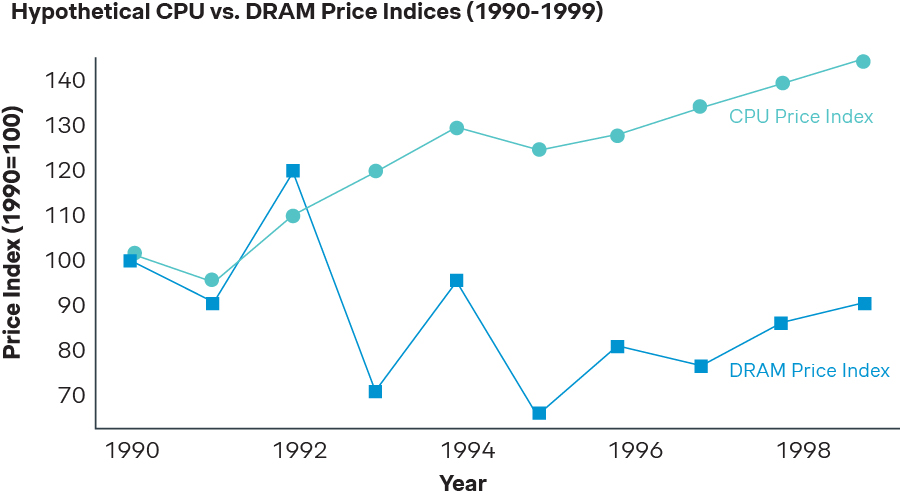

CPU Price Index shows relative stability or modest growth due to premium branding and continuous performance improvements.

DRAM Price Index fluctuates more sharply, reflecting cyclical supply-demand imbalances and market shocks (like overcapacity or the Asian financial crisis).

Conclusion: The 1990s—when technology met mass-market demand

In the 1990s, the semiconductor industry found itself at the intersection of phenomenal market growth (the PC, the internet, budding mobile technologies) and increasingly demanding technical challenges (sub-micron processes, ballooning fab costs). Overall, the decade cemented the industry’s global character, with robust expansions in Asia, intensifying competition, and consolidation shaping the quest for cost leadership.

Despite these pressures, the decade’s unwavering appetite for new, faster, and more functional chips meant that per-transistor and per-bit costs continued to plummet. The rise of the foundry model opened avenues for fabless innovation, while premium branding in segments like microprocessors demonstrated that not all chips needed to compete purely on price. Memory products, meanwhile, reminded everyone that the semiconductor cycle was alive and well, with volatility driven by capacity expansions and sudden market shifts.

Key lessons

The overarching lesson from the 1990s is that relentless technological progress—though crucial—must be paired with nuanced pricing, branding, and partnership strategies. The flood of demand from personal computing, networking, and emerging mobile devices produced vast opportunities, yet only the most agile and well-capitalized players consistently turned technology advances into sustained profitability. By blending cost leadership (through scale and node shrinks) with strategic product positioning and strong alliances (the foundry model, OEM relationships), semiconductor firms of the 1990s laid the groundwork for the even more complex and interconnected ecosystem we see today.

In our next article focusing on the 2000s, we’ll examine how the dot-com crash, the explosive rise of smartphones, and the move to ever-smaller process geometries reshaped semiconductor pricing into its modern form. From advanced nodes to fabless giants, the next decade would see the industry reach unprecedented levels of integration—setting the stage for the data-driven economy that now underpins almost every aspect of modern life.