2025 NRDL features a record number of longlist candidates for NRDL new listing and renewals, and the latest debut of the C-list as an alternative for high-value high-cost therapies, heralding intense competition and interesting dynamics at the same time.

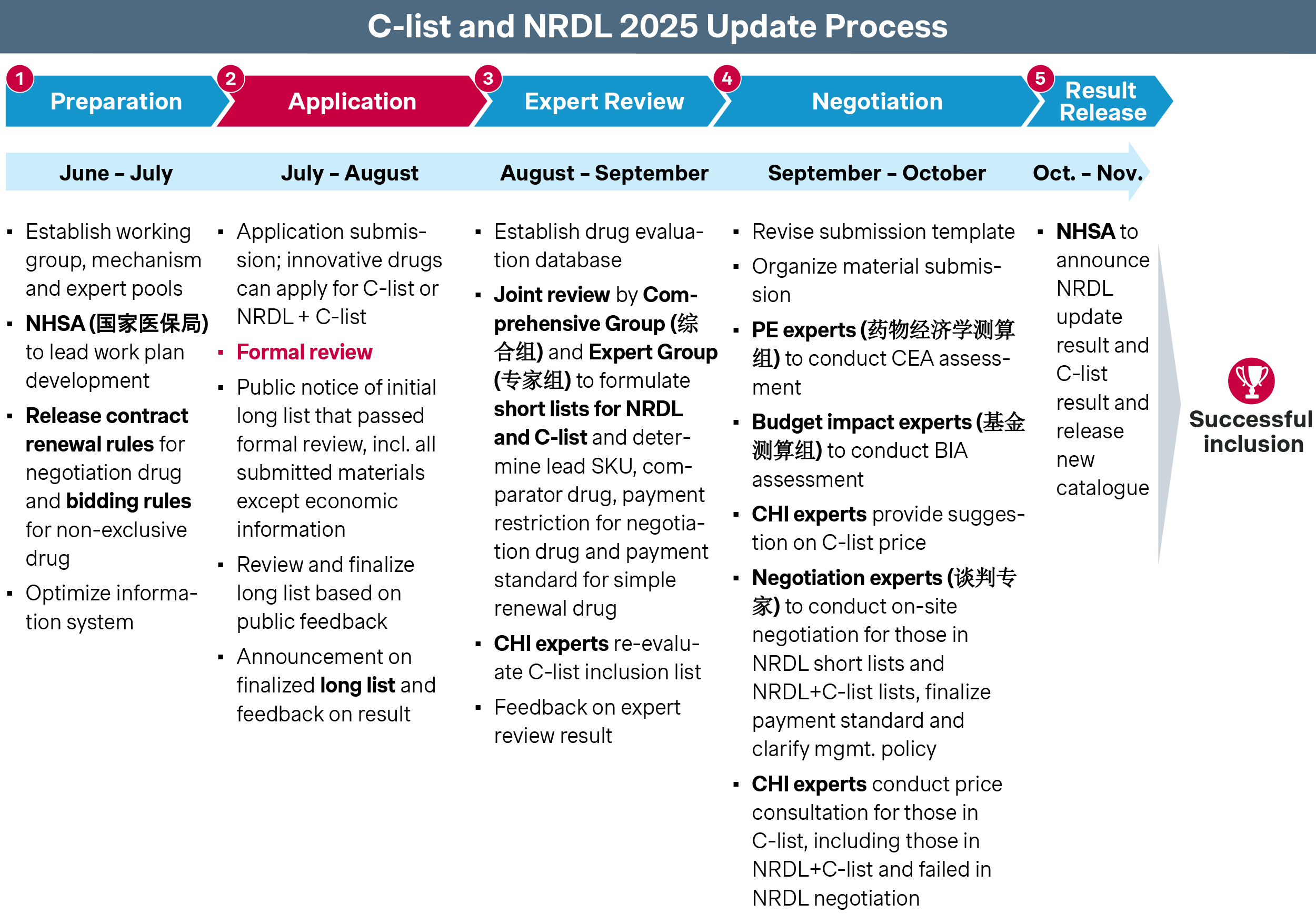

The 2025 National Reimbursement Drug List (NRDL) annual update has been unfolding as planned, with the first-round results released in mid-August. A record number of longlist candidates made it through formal review to the next rounds, foreboding fiercer competition ahead. Meanwhile, the newly introduced C-list offers both an alternative pathway and a fallback option for high-priced therapies, representing a new yet unproven opportunity that many cannot afford to brush aside.

- 310 drugs passed the first round for NRDL new listing – up from 249 last year.

- 224 drugs passed the formal review for NRDL renewals and re-negotiations, compared with 196 last year.

- 121 candidates passed the first round for C-list, of which 79 are pursuing NRDL new listing in parallel.

NRDL | C-list | |

Positioning & drug inclusion criteria |

|

|

Catalog enforcement |

|

|

Pricing mechanism |

|

|

Key therapeutic areas (TA)

For NRDL new listing, oncology, rare disease, neurology, anti-infectives and cardiovascular are the top five therapeutic areas this year, each with distinct dynamics.

Oncology

Oncology remains by far the largest TA, with 61 longlist candidates for NRDL new inclusion and another 21 additional candidates for C-list only.

- In lung cancer, three local KRAS G12C inhibitors, fulzerasib, garsorasib and glecirasib, have all passed NRDL formal review. All three candidates are innovative drugs with Breakthrough Therapy designations and similar clinical profiles, and will see head-to-head competition and potential showdown at next round.

- Multiple myeloma sees four major candidates this year. Sanofi’s Sarclisa is taking an all-in approach on NRDL, striving to demonstrate its clinical superiority over Darzalex. In contrast, three new bispecific antibodies for later-line therapy have all opted to skip NRDL in favor of the new C-list, including Talvey and Tecvyli from Johnson & Johnson and Elrexfio from Pfizer, potentially to bypass the price constraints that would come with NRDL listing.

- The ovarian cancer space will see three new candidates with distinct positioning: senaparib is aiming to be the next-generation PARP inhibition, sevacizumab is positioning as an upgrade to anti-VEGF drug bevacizumab, while Elahere touts itself as a truly innovative therapy with a novel mechanism of action and impressive PFS and OS results for FRα-positive patients, a rare breakthrough in ovarian cancer.

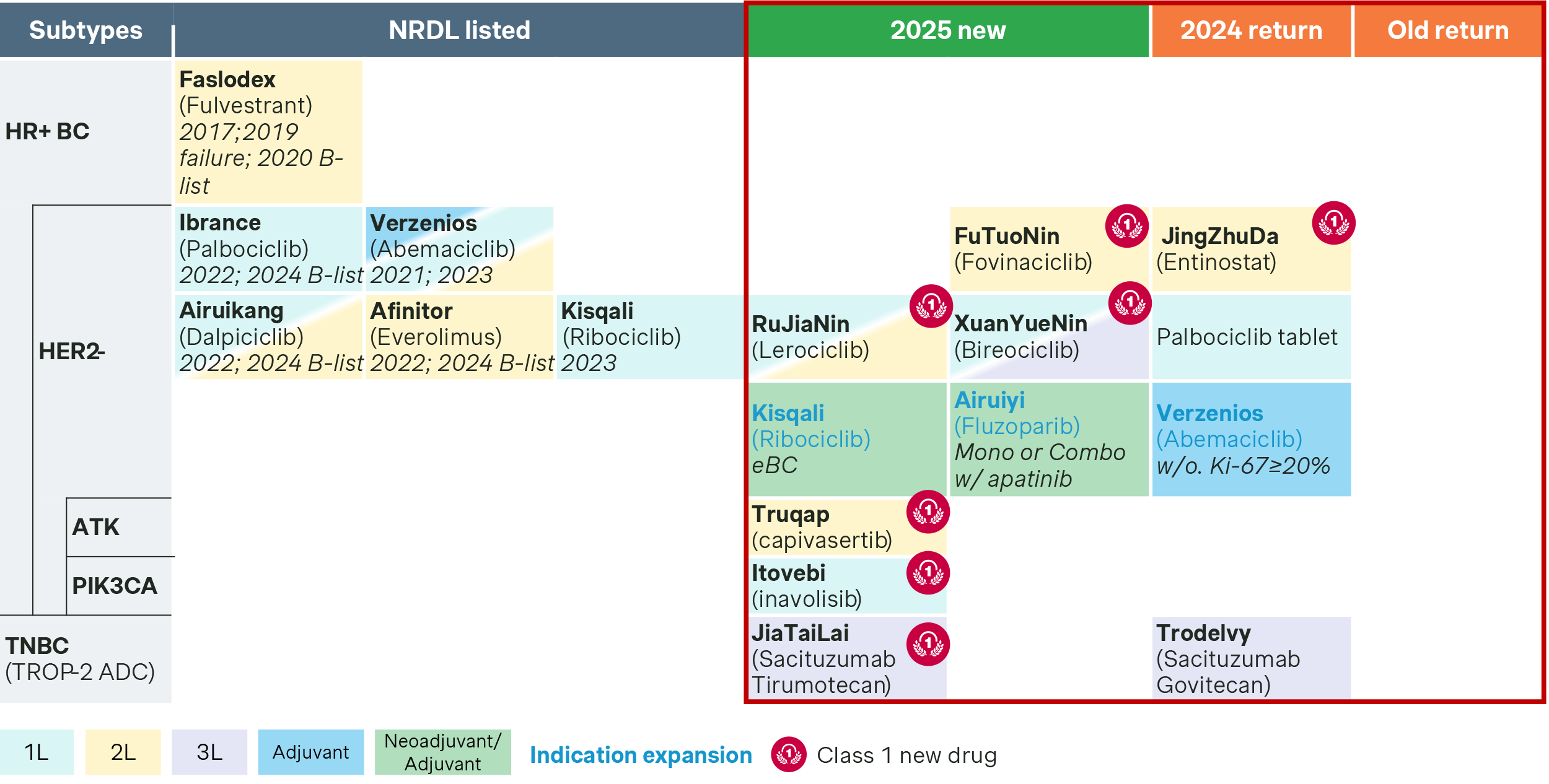

- In breast cancer, the spotlight is on the many HER2-negative therapies this year. Three domestic drugs entered the fray of CDK4/6 inhibitors, challenging the four NRDL-listed incumbents targeting the same pathway. Meanwhile, two target therapies, Roche’s Itovebi and AstraZeneca’s Truqap, are striving to differentiate themselves as the Class 1 first-in-class new precision medicines for chemo-resistant patients with PIK3CA/AKT mutations, aiming to address the significant unmet needs in the smaller but important patient segment.

Rare diseases

The rare disease space is seeing 37 longlist candidates for NRDL new listing, of which more than half pursuing C-list in parallel, and another 15 candidates for C-list only. Not surprisingly, C-list carries more hope and weight in rare disease than other therapeutic areas, given the many high-value high-priced therapies in the space.

- Ztalmy or ganaxolone is pursuing NRDL and C-list in parallel. Aiming to bring new standard of care for seizures associated with CDKL5 deficiency disorder, it emphasizes the high disability and mortality rates among CDKL5 children, and its differentiation from other common types of epilepsy treatments with superior clinical efficacy and safety track record, as well as its innovative mechanism of action.

- Agamree or vamorolone is also applying for both NRDL and C-list, Positioning as a new-generation dissociative corticosteroid, it highlighted both clinical data and real-world evidence of its reliable efficacy with a safety profile that is superior to traditional steroids, as a pediatric-friendly treatment for Duchenne muscular dystrophy (DMD) patients in China.

- Two IBAT inhibitors Livmarli and Bylvay have been approved in China for Alagille syndrome (ALGS) and progressive familial intrahepatic cholestasis (PFIC), respectively. Both are pursuing C-list only in the hope of better pricing, and bringing with them real-world evidence to demonstrate that their addressable patient segments are pediatric patients with low body weight, towards preempting budget impact concern of the commercial payers.

- Takeda’s Gattex or teduglutide has made the switch to C-list after failing last year’s NRDL as the new therapy for short bowel syndrome. It brings to the table new real-world evidence from early access pilot at Bo’ao to strengthen its value dossier. Similarly another high-price therapy for Gaucher disease velaglucerase beta also decided to pursue C-list only, while competitor Vpriv or velaglucerase alfa went for both NRDL and C-list in parallel.

- In hemophilia, Novo Nordisk’s Esperoct is making a comeback for NRDL listing this year, pivoting to recombinant factor VIII as its comparator while making strong arguments on its long-acting benefits clinically, social economically and pharmaco economically. In contrast, Roche’s Hemlibra is pursuing C-list only. Hemlibra has been notably successful with the fast growing City CHI coverage over the past four years, and the new C-list is the logical next step both as a defensive and offensive move. Concurrently, China’s first approved gene therapy Xinjiuning or dalnacogene ponparvovec for hemophilia B, made its debut as a C-list candidate as well, with strong emphasis on its innovativeness and compelling arguments on the lifetime pharmaco economics as a revolutionary gene therapy.

Neurology

In neurology, the most anticipated duel is between the new Alzheimer therapies Leqembi and Kisunla. Both drugs pursued NRDL and C-list applications in parallel, and both positioned as first-in-class therapies with no-comparators in their dossiers.

- Eisai’s Leqembi (or lecanemab) highlights safety as its core strength, supported with multi-dimensional data from real-world evidence and post-marketing adverse event surveillance.

- Lilly’s Kisunla (or donanemab) emphasizes dosing convenience as its unique advantage, with the regimen of one injection every four weeks and possible treatment discontinuation after plaque clearance. Moreover, its impressive efficacy among the low- to mid-Tau protein population was highlighted as a key differentiator.

Kisunla (donanemab) | Leqembi (lecanemab) | |

| MoA | pE3Aβ | Aβ |

| Manufacturer | Lilly | Eisai |

| CN approval time | 2024-12-17 | 2024-01-05 |

| Designation | Breakthrough Designation, Priority Review | Breakthrough Designation, Priority Review |

| Class 1 new drug | ✔ | ✔ |

| Indication | AD with mild cognitive impairment (MCI) or mild dementia stage of disease | |

| Dosing | IV, 700mg Q4W for the first 3 times and 1400mg Q4W after | IV, 10mg/kg, Q2W |

| Comparator | Likely result: No comparator | |

| Current annual price | 253K RMB | 196K RMB |

| Application | NRDL+ CHI-IDL | NRDL+ CHI-IDL |

Infectious diseases

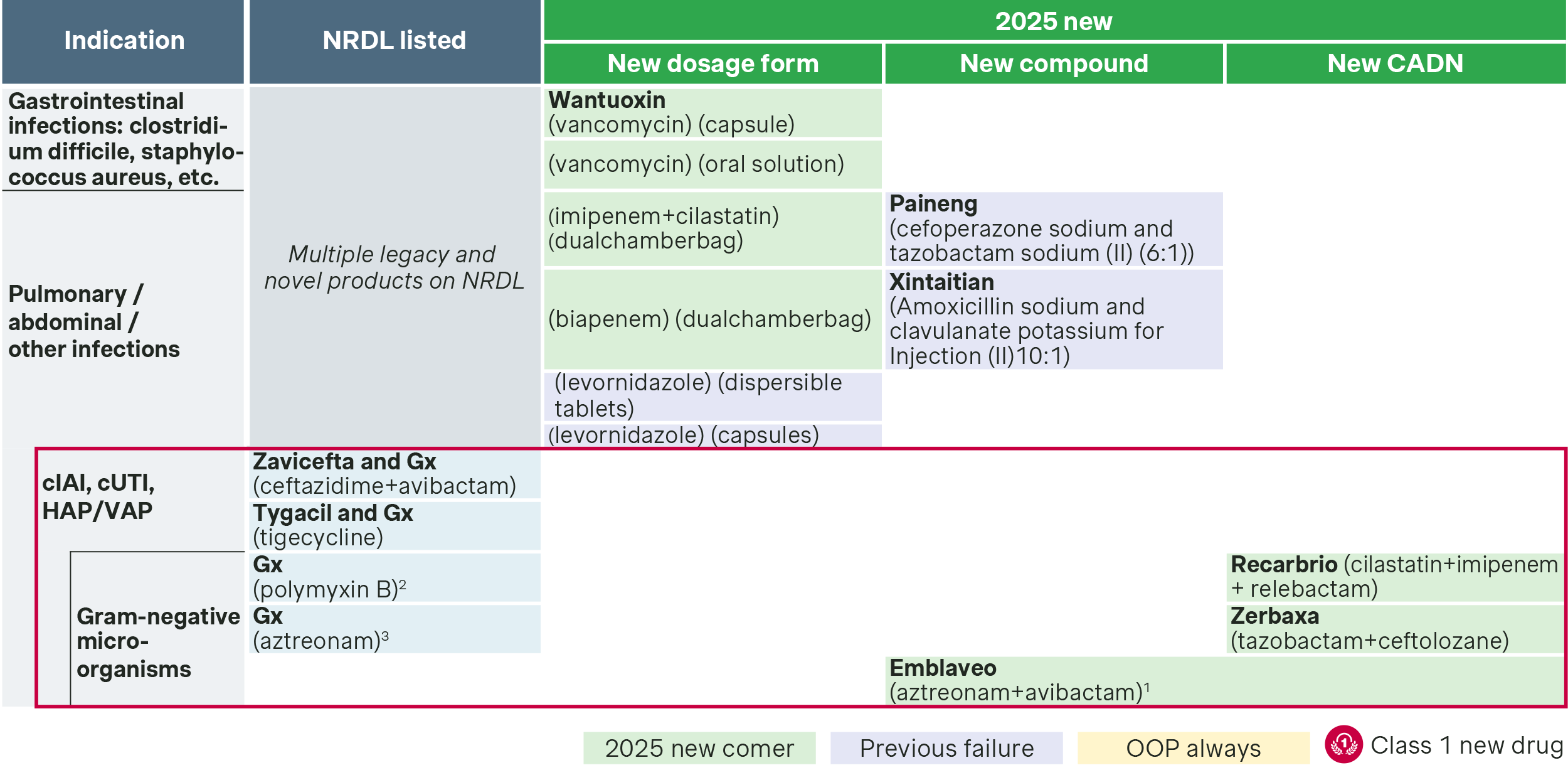

Competition is especially intense in severe infections caused by Gram-negative bacteria, with three new candidates vying for NRDL inclusion, as public reimbursement is still the all-important battle ground for anti-infectives.

- Recarbrio, also known as cilastatin-imipenem-relebactam, is a new combination for carbapenem-resistant Enterobacteriaceae and Pseudomonas aeruginosa (CRE/CRPA) infection. By adding the next-generation β-lactamase inhibitor relebactam to the imipenem + cilastatin-based therapy, it offers enhanced efficacy. Phase III RESTORE-IMI results showed favorable renal protection and superior safety, and it has already been recommended as a first-line option by multiple clinical guidelines.

- Zerbaxa, or tazobactam-ceftolozane, targets multidrug-resistant Pseudomonas aeruginosa (MDR-PA) infections. While partially overlapping with Recarbrio’s target population, it differentiates itself with pediatric indication, addressing a critical gap in the treatment of drug-resistant bacteria in children.

- Emblaveo, or aztreonam-avibactam, targets metallo-beta-lactamase–producing carbapenem-resistant Enterobacteriaceae (MBL-CRE), a high unmet-need infection with no approved treatment options. Compared with empirical treatment, it significantly reduces mortality and ICU stay in CRE patients and is positioned as the “last line of defense” against many drug-resistant bacteria.

Cardiovascular

Cardiovascular is seeing both established and new players competing, with many striving for differentiations in some of the most contested indications.

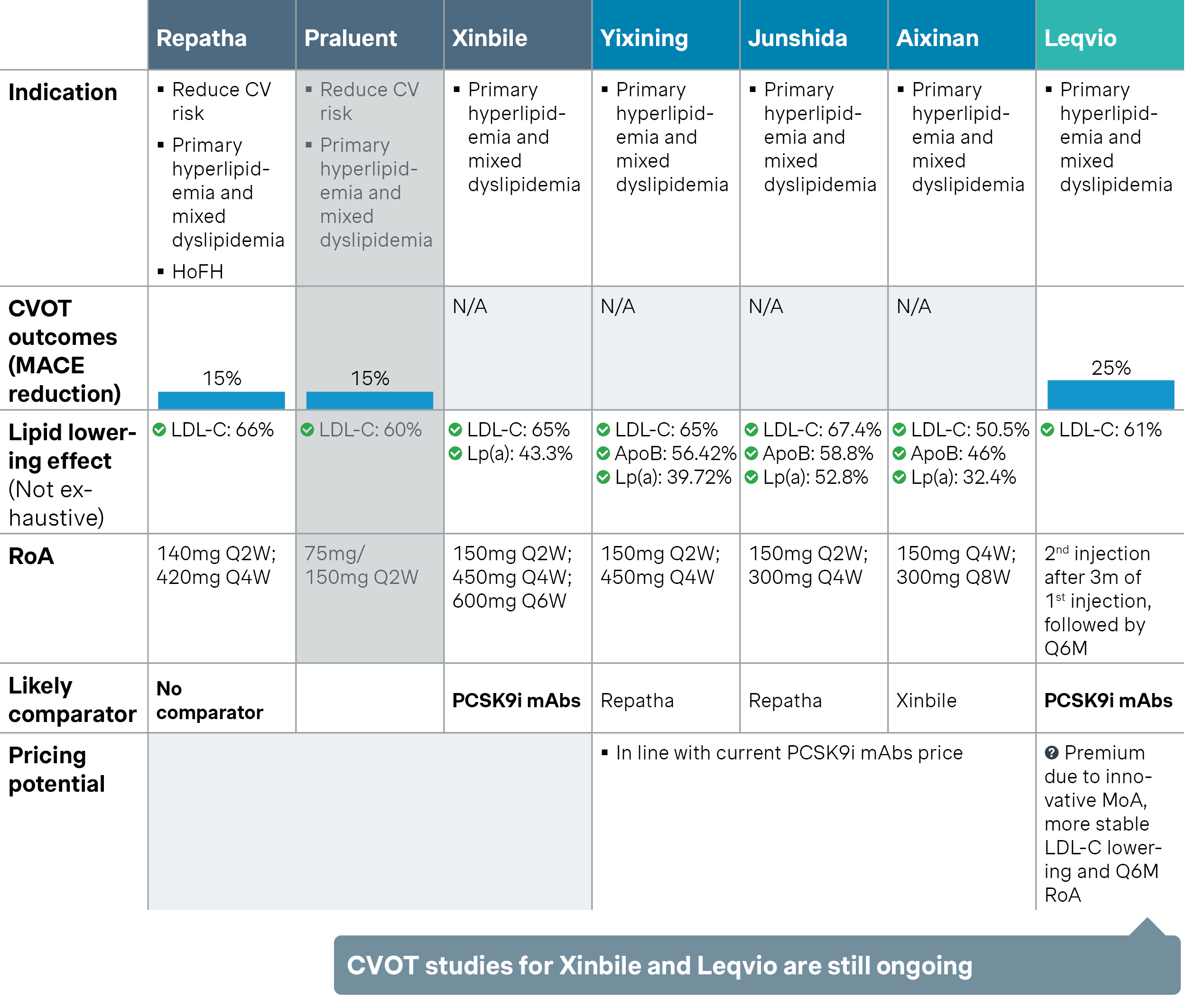

- Three domestic PCSK9 monoclonal antibodies have passed NRDL formal review, each taking a distinct position to stand out in the crowded lipid-lowering market. Both ongericimab and ebronucimab proposed Amgen’s Repatha or evolocumab as the comparator. The former focuses on superior dual reduction of LDL-C and Lp(a) for better residual cardiovascular risk management, while the latter highlights exceptional LDL-C target attainment in high-risk patients. Recaticimab takes a different approach, emphasizing its 8-week dosing interval as the world’s first ultra-long-acting PCSK9 mAb, with the potential benefit of improved adherence. It also proposed a higher-priced comparator, tafolecimab, aiming for a more favorable NRDL price outcome.

- Leqivio, or inclisiran, has shifted from a “no-comparator” approach last year to benchmarking against PCSK9 mAb. It added multiple pieces of real-world evidence to underscore its twice-yearly dosing advantage over PCSK9 mAbs, highlighting better adherence and sustained LDL-C lowering and target attainment, as well as innovative MoA as an innovative siRNA therapy.

Renewals

With 224 drugs up for NRDL renewal this year, some long established listed drugs are seeking to go into regular listing as a safe heaven, many recent ones are jostling for simple renewals, while others are bracing for re-negotiations either due to over-budget sales or significant indication expansions. In fact, 57 of the 224 drugs are seeking indication expansions or coverage restriction rewording, many of which would expect tougher battles going into next round.

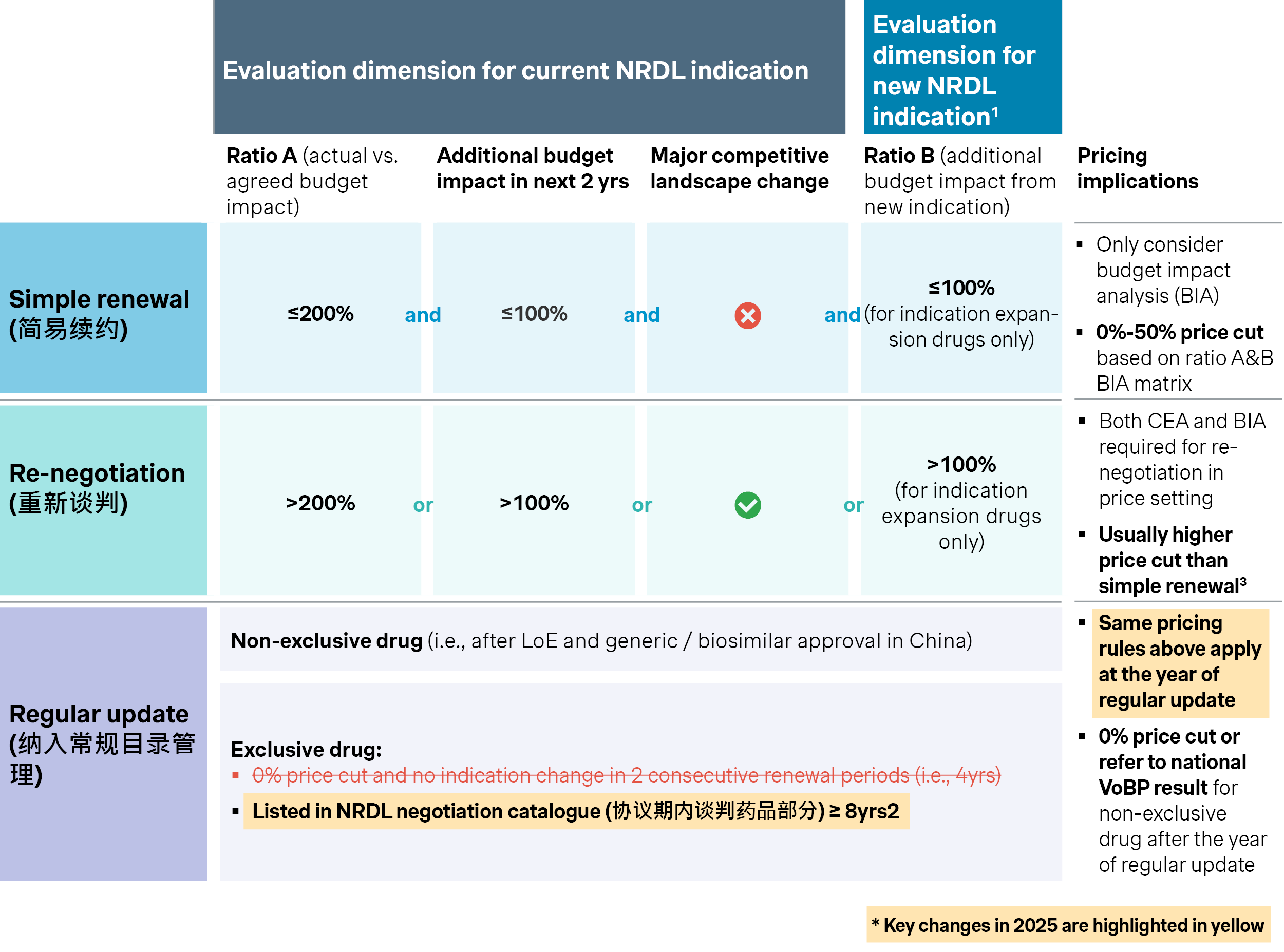

Meanwhile, the renewal rules for NRDL-listed products have been further finetuned this year:

- Stricter pathway to regular catalog listing: The previous shortcut of regular listing after two consecutive contract periods has been phased out starting this year, so the possibility is now reserved only for drugs that have been NRDL listed for eight consecutive years. In addition, the rules also explicitly require listed prices to be revisited before going into regular listing, posing new uncertainties to the 9 eligible drugs that were first listed in 2017, including Lucentis, NovoSeven and Epidaza among others.

- Selective expansion of indications will be more challenging: There have been cases of selective indication expansion to manage renewal price cuts in recent years, that will be put under more scrutiny this year as NHSA requires renewal applications to include all indications approved in China to date. Among the longlist candidates this year, some are still trying to seek expansion only for high-price low-budget impact indications, but may have a tough time pulling that off this year.

- Oncology dominates renewals with 58 candidates: Many of them are likely to be summoned into re-negotiations with different triggers, including several immune-oncology products applying for new indications with combination therapies, including high-fliers like cadonilimab, camrelizumab, sintilimab, savolitinib and anlotinib alike. The combo consideration is likely to exert additional pressure on their renewal prices if both are NRDL listed, while how the combo would fare between NRDL and C-list drugs will be of great interest to many.

C-list debut

The C-list debut is the highlight of the year after all. While it could be and has been seen as somewhat an overreach on the part of NHSA, the industry is also cautiously optimistic that it may help drive the next wave of growth for commercial healthcare insurance, and it can theoretically synergize with basic medical insurance for more comprehensive and systematic coverage. In addition, it may serve as a testing ground for innovative payment models like budget capping, outcome-based payment and coverage with evidence alike, and turns out to be an agent for change.

As a result, many rare disease and oncology drugs have been testing the new waters, including around half that previously failed with NRDL listing, and another half that didn’t even bother with NRDL before.

- Of the 121 C-list candidates, 42 high-value products are focusing solely on C-list, including ultra-rare disease drugs like Qalsody, Hunterase and Qarziba, which have repeatedly failed in NRDL negotiations. Newcomers like benmelstobart are also steering clear of the overcrowded PD-1/L1 competitions by pursuing C-list only as well.

- 79 drugs are applying for both NRDL and C-list in parallel, including many high-priced therapies like bispecific antibodies, antibody-drug conjugates, enzyme replacement therapies and cell therapies.

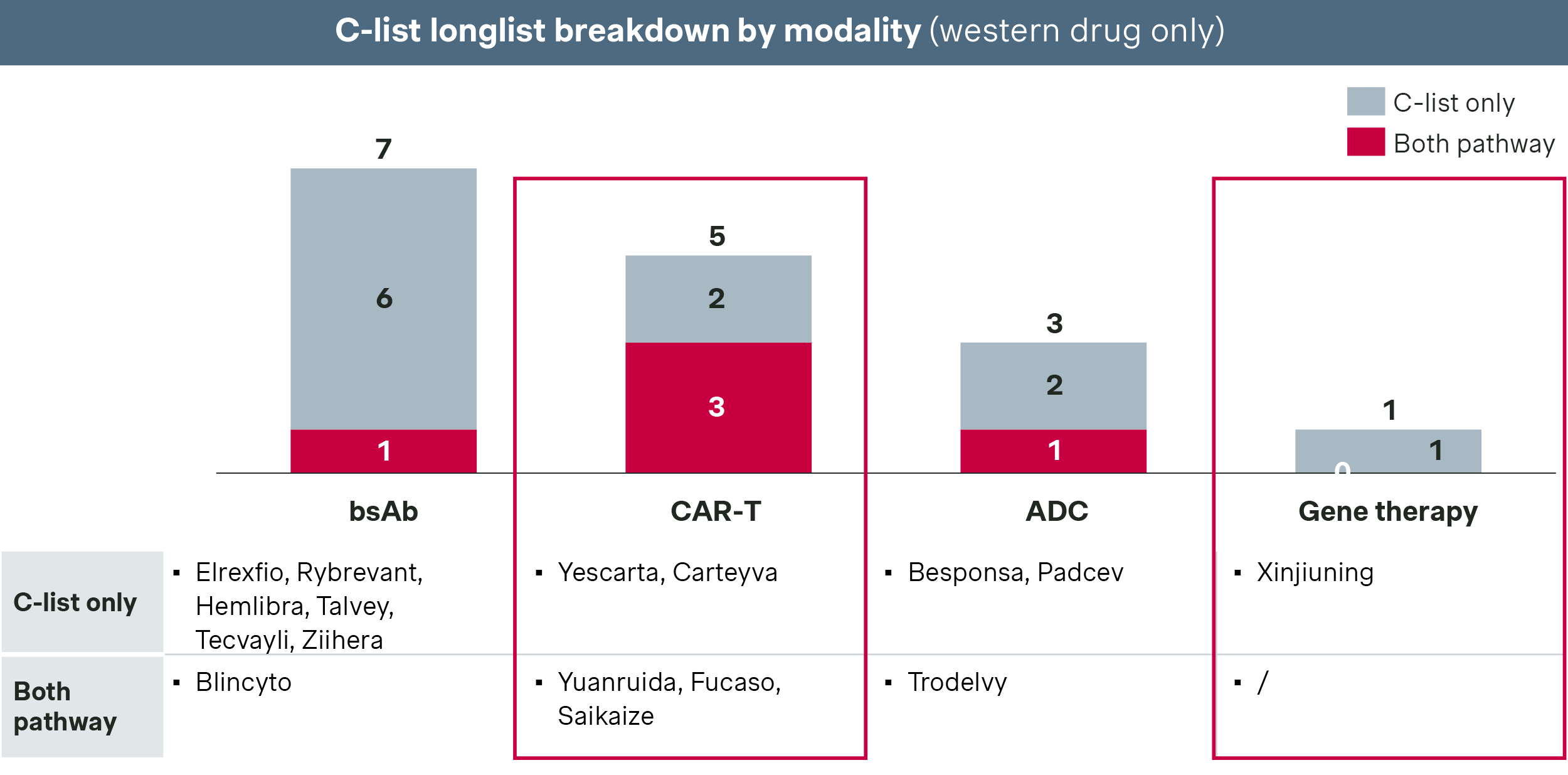

- Of particular interest are the five CAR-T therapies and the only gene therapy that are going after C-list. If successful, the C-list could very well become a catalyst for next-generation therapies, helping them overcome access and affordability challenges going forward.

Looking ahead

While the landscape and dynamics vary by TA and indication, a few important themes are emerging for 2025.

First of all, the overall competitive intensity is reaching a new high with the record number of longlist candidates for 2025, meanwhile the overall budget for NRDL remains tight by all indications, which leads to an easy prediction of record low success rate and high price pressure for eventual NRDL listing this year around.

The saving grace will be the C-list, which is designed to be more inclusive than NRDL especially for high-value high-priced therapies. It is reasonable to expect a much higher success rate for C-list with less price cuts, while it is much harder to predict how much gain in volume and uptake will be garnered in return. Hence, 79 of the candidates decided to pursue both in parallel, with NRDL listing still as the first choice and C-list as a potential fall back.

Overall, there will be a recurring emphasis on innovation like previous years. In fact, there are over 100 candidates that were approved within the past 12 months, and 54 candidates with Class I drug designation as they are recognized as first-in-class globally. Even for them the competition could be cut-throat as seen many cases above, more so for the others which would have much more work to do to articulate differentiated value propositions, preempt payer concerns and furnish compelling evidence accordingly, NRDL or C-list.

With the fork in the road, many have decided to take it with hope.

Thanks to contributions from Yucheng Dong, Victoria Liu, Justinian Liu, Selene Peng, and Grace Ge!