While the OCFO software market shows strong underlying growth, investor attractiveness – beyond generic target selection parameters such as ticket size/EV and investment strategy – is ultimately determined by exposure to high-growth segments and company-specific capabilities.

These can be assessed across five key characteristics to identify the most attractive segments. In addition, attractive OCFO solution providers score well on two key company capabilities:

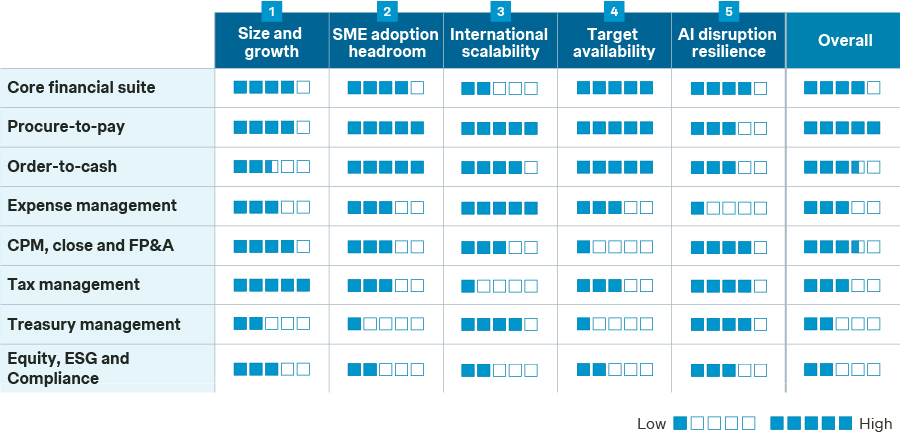

The five segment characteristics are: 1. Product segment size & growth, 2. Headroom in micro/small and mid-market customer segments, 3. International scalability, 4. Target availability and 5. Resilience to AI disruption.

The two company capabilities are: 1. Alignment with the evolving CFO role and 2. AI innovation maturity.

Segment characteristics

Overall, solutions for core financial workflows are most attractive:

Product segment market size and growth potential

Except for order-to-cash, solutions for the core financial workflows are the largest product segments in the Dutch OCFO market. Tax management and procure-to-pay are the two largest of these segments, both still having significant further potential. In fact, all segments are expected grow strongly with double-digit percentages, driven by moderate to significant potential adoption headroom.

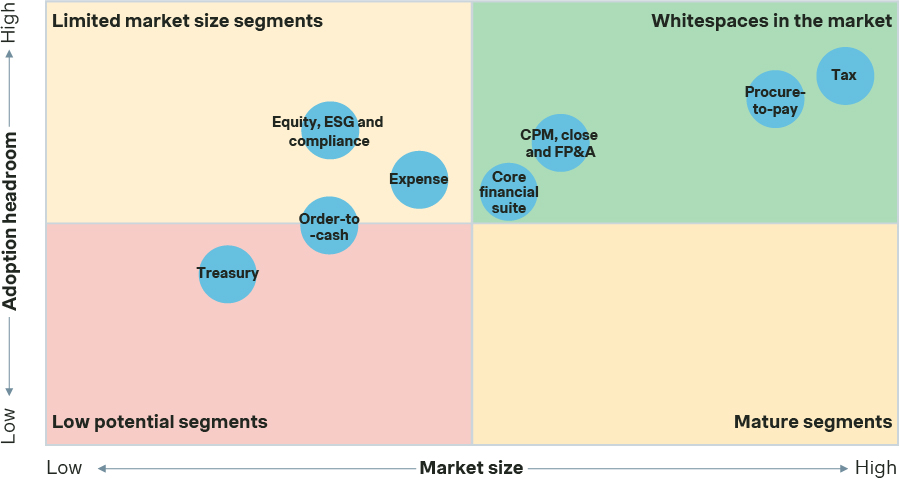

Adoption potential in micro/small and mid-market customer segments

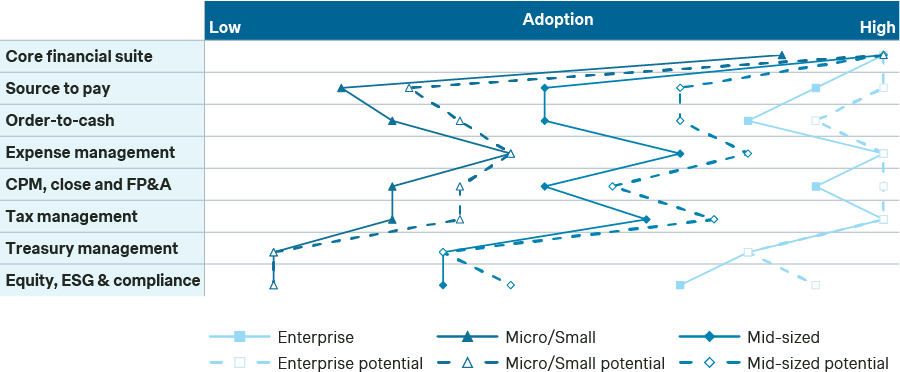

Micro/small and mid-market customers offer the strongest growth potential, as adoption in various OCFO segments remains relatively low. Investors should therefore prioritize product segments with high relevance and significant headroom for adoption in micro/small and mid-market customers as the large enterprise segment is dominated by leading ERPs like SAP and Oracle.

The most attractive segments combine (i) strong importance for micro/small and mid-sized customer groups with (ii) still-moderate penetration, enabling growth through continued adoption. Examples include source-to-pay, order-to-cash, and expense management, where solutions address critical workflows and adoption is still scaling.

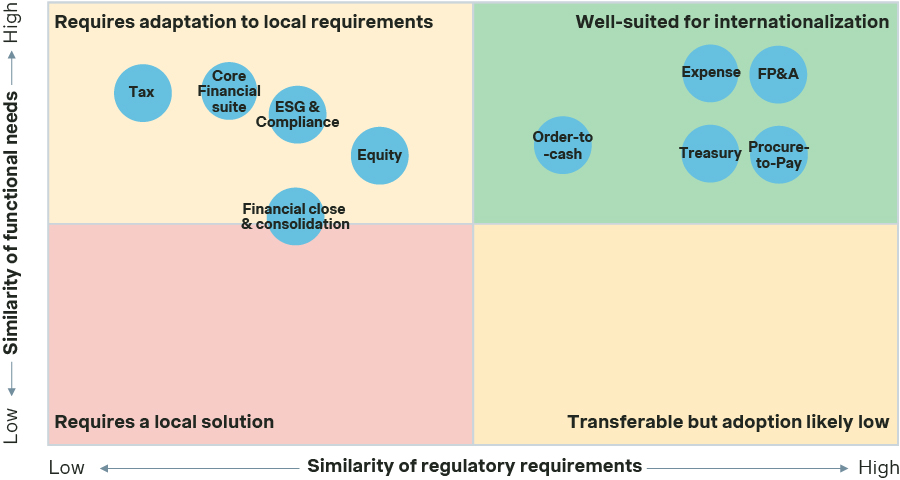

International scalability

A key investment consideration is the ability to scale internationally with limited localization requirements. While functional requirements are often similar across countries, differences in local regulation (e.g., accounting standards, tax rules, compliance requirements) can significantly impact scalability.

Segments such as procure-to-pay, order-to-cash, expense management, and FP&A are well-suited for international expansion, combining standardized functionality with relatively low regulatory complexity. This enables product portfolio simplification and scalable, repeatable go-to-market models across countries.

By contrast, segments such as core financial suite, tax management, and ESG & compliance require substantial localization, making them more ‘local-for-local’ and harder to scale efficiently as adapting existing solutions is impractical from a time-to-market, technical, and financial perspective. As a result, expansion in these areas often relies on M&A to access local capabilities (e.g., Visma, Wolters-Kluwer).

Target availability

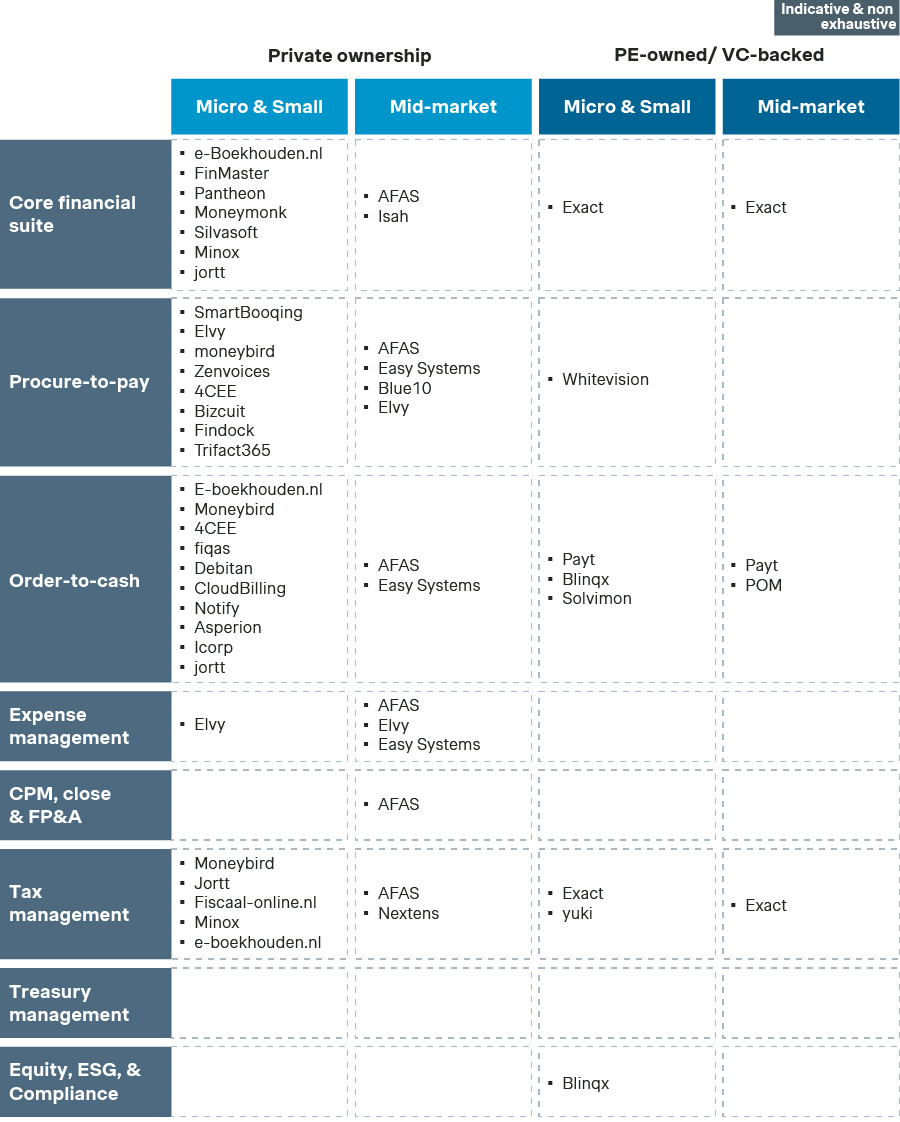

There are many potential target OCFO software providers active in the Dutch market serving micro/small and mid-sized companies. This includes well-known large players such as Exact and AFAS but also increasingly a diverse landscape of companies in the scale-up or growth stage offering SaaS solutions with an anchor point solution which they are gradually expanding into a wider integrated OCFO solution with many integrations.

Many of these companies remain privately owned but may be seeking new partners to support scaling both domestically and internationally. The availability of potential targets is particularly strong across the core financial suite, procure-to-pay, order-to-cash, and expense management segments. Except for core financial suite, these segments are especially well suited for international expansion due to their relatively low regulatory burden.

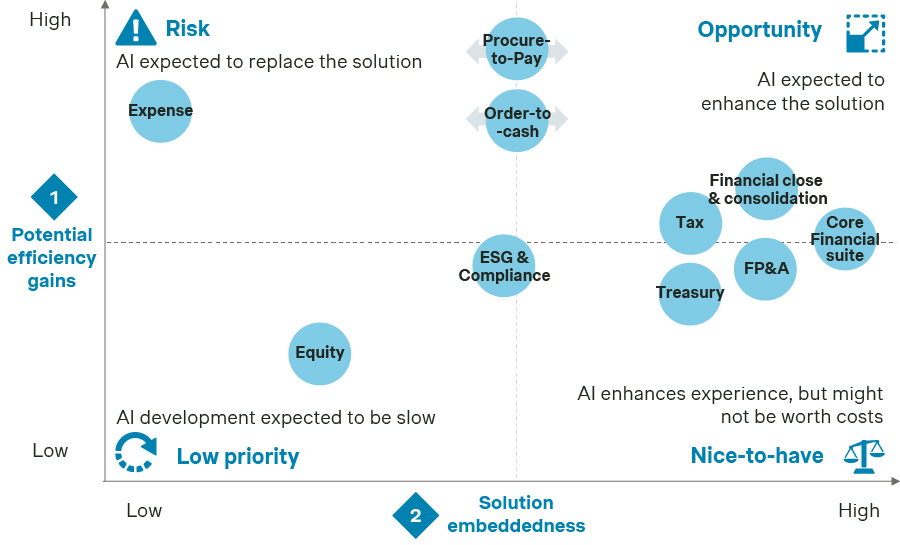

Resilience to AI disruption

AI disruption risk is currently top of mind in software investing; however, its impact is unlikely to be uniform across the OCFO software space, with several segments showing higher resilience. Whether AI is a risk or an opportunity for software providers depends largely on the scale of potential efficiency gains it enables and how deeply the software is embedded in core workflows. Mission critical vertical software is far harder to replace than a standalone productivity workflow tool.

Potential efficiency gains are largest in segments where productivity improvement is high and/or cost savings are high and the standard for quality of workflow output is not very high/critical. Solutions will be more embedded if the solution is mission critical, has a high number of users, the workflows have a low degree of repetition/standardization and there are high switching costs (e.g. training of staff).

Expense management is the most exposed to AI disruption given that the potential efficiency gains from AI are high while expense management solutions are relatively easy to replace by organizations.

Agentic AI is expected to automate many of the repetitive and standardized workflows in the procure-to-pay and order-to-cash processes. On the one hand this can drive penetration of innovative solutions but can also pose a challenge as it reduces reliance on user-based interactions, which impacts traditional SaaS user-based revenue models.

More complex and/or regulated segments (e.g., FP&A, tax) tend to be more resilient to feature commoditization and workflow disruption, given higher requirements for domain expertise, accuracy and compliance.

Company capabilities

Companies that are attractive to investors are well positioned to capture the opportunities arising from the evolving CFO role and the automation and performance potential of AI. This can be achieved through strong product development capabilities, while M&A can further accelerate product breadth and depth and support the development of more integrated platforms. As OCFO companies transform, it is imperative that their commercial models adapt accordingly.

Alignment with evolving CFO role

Investment attractiveness increasingly depends on how well customer and product strategies align with the evolving role of the CFO. The shift in focus from reporting and compliance toward performance management and forward-looking decision-making is driving demand for solutions that provide real-time insights and connect financial and operational data.

Narrow point solutions risk losing relevance, whereas platforms that cover end-to-end workflows or integrate seamlessly into existing ecosystems are better positioned to capture value. Companies that combine strong capabilities in core CFO workflows with expansion into adjacent, higher-value use cases are therefore better positioned to benefit from this shift and drive sustained growth.

AI innovation maturity

AI represents both a risk and an opportunity. Laggards will lose ground to companies that effectively capture AI-driven potential. Successful companies must proactively enhance their products through superior automation of repetitive workflows, improved insights and forecasting, and stronger decision support to create differentiated – albeit often temporary – competitive advantages.

However, these advantages are rarely durable, as AI also accelerates feature replication and convergence. Investors should therefore assess not only current product differentiation, but also a company’s ability to sustain innovation through continuous development and proprietary data advantages,

At the same time, companies must actively manage the downside risks AI introduces to their revenue and operating models. Pricing pressure may emerge as AI accelerates competitor catch-up and erodes differentiation, requiring more disciplined pricing and packaging. In parallel, shifting usage patterns may lead to revenue erosion, making it essential to adapt monetization models – for example through usage-based pricing or more dynamic packaging structures.

OCFO software companies are investing heavily in product expansion, vertical functionality, and AI capabilities. While this supports innovation, it also increases cost intensity and reinforces scale advantages, widening the gap between scaled leaders and subscale players. As seen in other software markets, sustained innovation pressure is likely to drive consolidation, with larger platforms pursuing capability-led M&A while subscale players face increasing pressure on competitiveness and standalone viability.

Key takeaways for investors

Against the backdrop of the wider software market – where valuations have reset but structural demand remains intact – the Dutch OCFO software space offers a selective but compelling M&A opportunity. Investors should move beyond broad SaaS exposure and proactively screen for scalable, AI-enabled platforms in high-growth segments such as procure-to-pay, order-to-cash, and FP&A – particularly those with strong penetration potential in the mid-market and clear pathways to international expansion.

With a deep pool of founder-owned and scaling assets available, now is the time to build conviction, engage early, and position for consolidation-driven value creation in a market that will continue to reward strategic buyers with a clear thesis.