We previously discussed how in Europe the B2C automotive market is larger and more accessible for Asian brands. But what potential does the enterprise market hold, and how can newcomers tap into it? We wrap up this series by discussing how newcomers can tackle B2B as part of a well-defined long-term strategy.

Having worked extensively with automotive manufacturers from emerging markets, we repeatedly observe unrealistic expectations about enterprise sales. OEMs believe that the European B2B market offers high volume potential, and consider it too big to overlook. Some hope to take a “shortcut” by entering the B2B market through partnerships with large mobility providers, while others plan to grant high price discounts, even before establishing a solid presence in the B2C market. This is a risky strategy that will likely result in weakened brand image and lost price control. In reality, a solid B2C presence needs to come before B2B market penetration, and here’s why…

Why is the B2B automotive market so hard to crack?

In short, because THE B2B automotive market does not exist.

In Europe, the enterprise market is historically grown and highly fragmented. Every European country is unique with respect to enterprise market landscape, operational infrastructure, and client requirements. It calls for a much more customized country-specific approach than for the B2C market. Even within a country, a variety of different dynamics in the enterprise market can be observed.

Take Germany as an example. Corporate fleets have the biggest vehicle parks in the entire enterprise market. But as you can imagine, they need to be hunted down one by one. There is no silver bullet that enables new entrants to scale up the B2B business overnight.

Mobility providers seem to be ideal customers due to their sheer fleet size, but again, this is deceiving. Big players such as Sixt Leasing and Alphabet have negation muscles that can strong-arm any new market entrants with very little leverage. And more importantly, as we mentioned in the last article in this series, succeeding with B2B customers requires a successful track record and a functional sales and service network.

To achieve sustainable growth in the B2B market, newcomer carmakers need a well-defined strategy, including value-based customer segmentation, an offering design based on target segments, and the right value-selling strategy and tactics. Continuing with our focus on Germany, let’s take a deeper look at the potential customers in Europe’s biggest enterprise market.

Who are the B2B target customers?

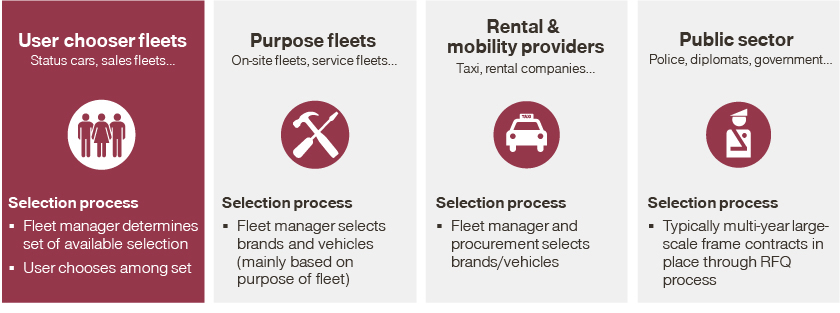

The German B2B automotive market consists of four main sub-segments: User-chooser fleets, purpose fleets, rental, and the public sector. Among all four, the user-chooser fleets are the biggest sub-segment in terms of volume, in which we have also seen strong growth momentum in the last years. For those who are not familiar with the user-chooser concept, it refers to company cars that the end users, or the employees who are entitled to a company car, choose from a selection of models made available by the employer.

Purpose fleets might be interesting for mass car brands. But a new premium brand would not want to see its logo on service cars as this would weaken or even deny their premium image. Rental and mobility providers are very challenging customers, doing things on their own terms, so it would be very tricky for new car brands without a track record to enter this sub-segment. Then the public sector is by far the smallest sub-segment, which tends be less open to new car brands from e.g. Asia.

Therefore, user-chooser fleets seem to be the most reasonable sub-segment to jump-start with. However, there is also a fairly high degree of competition, especially from traditional local brands, and OEMs will need to understand the motivation of the end users as well as the decision-making of fleet managers in order to convince them during the selection process.

Motivations behind user chooser fleets

Usage of company cars is popular in Germany for several reasons: For employers, company cars are a cost-efficient way to provide a company benefit. For employees, a company car can be both a status symbol and a saving.

Whether a company vehicle is offered and which model is chosen generally depends on an employee’s role. For non-executive staff, the vehicles offered are usually lower-priced models and are mainly considered to be simply a means of transport (e.g. for a sales rep visiting customers) rather than a company benefit. In contrast, adoption of more expensive models is generally high among executives, where company cars are seen as a perk.

In a sense, a user-chooser is similar to a private driver. The only difference being that the latter needs to finance the car themselves. A logical consequence is that a user-chooser would pay more attention to the quality or value for the budget at their disposal. Obviously, the status symbol of a premium badge would play in favour of Mercedes, BMW, and co. Newcomers do not have such a privilege, unfortunately. Nevertheless, if a carmaker is in a position to exceed the expectations of target customers on car features and beyond, as they would do in the consumer market, they have a fair chance of winning the user-choosers, too.

Decision-making process of user-chooser fleets

Although the end users have the final say on the car model, it has to belong to the fleet in the first place – a decision that is made by fleet managers.

At large corporates, the fleet manager sources company cars directly from OEMs (mainly domestic premium brands in the case of German market), with negotiation rounds taking place every couple of years. Switching to a less popular brand could result in frustration among employees and therefore must be considered carefully – exactly the reason why foreign brands have great difficulty in penetrating company fleets, especially in their early days on European soil.

Fleet managers have a different set of decision criteria for a car brand than an average car driver. Their primary interest is keeping the fleet up and running with as little hassle as possible. In this light, convenient and reliable after-service matters more than a fancy car. Looking beyond the car, fleet managers would also favor flexible, customizable contracts, which often imply big discounts. This is a trade-off that a new car brand has to make – buying the volume in the enterprise market might prove pricey.

Getting a foot in the door: Grow your B2B business, one company at a time

For newcomer OEMs in Europe, the way to get onto a fleet manager’s radar is through a solid B2C presence. Before negotiating with Chinese OEMs, fleet managers would like to actually see their cars driving in the streets and be able to assess their long-term performance. The next step is to convince the user-choosers with suitable products.

Our recommended strategy for building out the B2B market

- Install a dedicated team: For entering the B2B market, newcomers need to establish dedicated capacities to realize B2B contacts and sales

- Identify your niche and create a special offer around it: Adjust vehicle offering, especially for target fleets (e.g. leasing only, refine trim line with business+ package)

- Identify target companies in a hunt list: E.g. for electric vehicles, this could be identifying companies with a (public) affinity for sustainability (e.g. energy, logistics)

- Approach each company one by one: Address one company at a time by contacting them via fairs, conventions, and cold acquisition

Read more from this series:

Part 1: Six Pillars for Carmakers from Emerging Markets to Succeed in Europe

Part 2: Automotive Newcomers: Sales Model for the B2C Market

Part 3: Automotive Newcomers: Sales Model for the B2B Market