AI is acting as the first interpreter of value at the most critical juncture of the buying journey

For more than two centuries, insurers relied on human agents not just to explain complex products, but to temper sticker shock, manage knee-jerk reactions, and shape how consumers understood value.

By contextualizing price, redirecting attention, and framing tradeoffs, agents – both captive and independent – guided consumers and kept the value narrative on the industry’s terms. Even when digital channels arrived, the underlying logic stayed the same. Online and mobile journeys embedded the same choreography: guided flows and scripted messaging shaped how consumers interpreted value ahead of any decision.

AI has disrupted that world order.

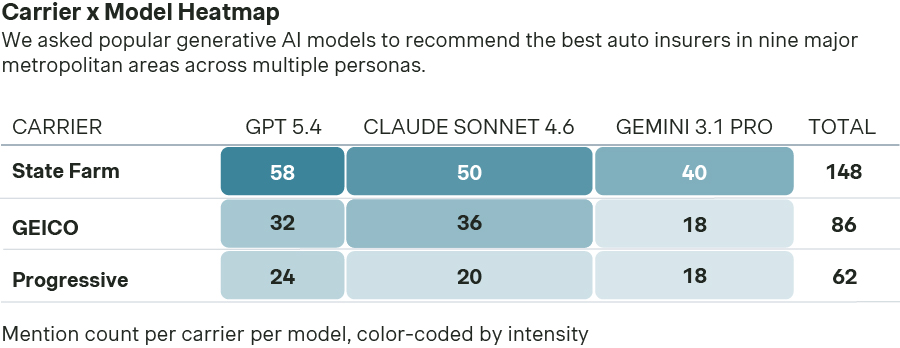

Increasingly, consumers are turning to ChatGPT, Google Gemini, and Perplexity to decide where to buy auto, home, and personal insurance. A prompt like, “Which companies offer the best auto insurance,” returns a curated short list of carriers (such as State Farm, GEICO, or Progressive) alongside a brief explanation of why those carriers are strong options.

If you appear on that list, AI becomes a new distribution advantage. If you don’t, your brand may be excluded before the buying journey begins.

By going directly to generative AI, consumers are effectively relegating authority to an AI model to deliver the first explanation of value, a position formerly occupied by the carrier, its agents or distribution partners. The consumer’s frame of reference is now defined by an AI system that processes information based on its own generative logic, rather than the industry’s preferred narrative.

This fundamental reordering of who frames pricing and value at the start of the insurance buying journey sent shockwaves across financial markets in early 2026. Major U.S. insurance broker stocks including Willis Towers Watson, Aon, and Arthur J. Gallagher fell sharply following news of a ChatGPT-integrated AI insurance app.

What changes when AI talks first

When AI takes over as the first interpreter of value, the dynamics of the insurance buying journey shift dramatically.

For decades, insurers designed products under the assumption that human intermediaries would contextualize premiums, explain tradeoffs, and highlight the protection and security benefits their products offered. Complexity gave agents room to shape the value story.

With AI, the complexity that once supported differentiation and performed well in a guided sales environment is now a liability.

AI assistants are trained to make complex information digestible and to prioritize clarity and simplicity. They summarize pricing structures, discounts, and bundles based on what can be easily explained, not on what supports a carrier’s differentiation in the marketplace. Premiums are evaluated without context or guidance, and price comparisons are instant.

The shift also transforms the role of independent agents. Agents have traditionally been the first interpreters of coverage, tradeoffs, and price. As AI assistants increasingly perform that role upstream, agents are more likely to enter the journey after options have been narrowed, and expectations set. Their role shifts from shaping the decision to validating one that’s already formed.

The new economics of buying

When consumers make AI assistants the first stop in their buying process, comparison becomes narrative-driven rather than journey-driven. Instead of reviewing price tables or feature lists, customers receive synthesized judgments about relevance, value, and tradeoffs.

This shift matters because:

Pricing and packaging are interpreted by an AI model before a carrier enters the conversation. AI compresses fine-grained product differentiation into broad, simplified takeaways.

The willingness to engage and willingness to pay are shaped far earlier in the customer journey than customary. The customer’s value perception is formed upstream, before they even request a quote or decide to renew.

AI blunts the impact of top-of-the-funnel spend. AI framing outweighs advertising, SEO placement, and channel investments in shaping first impressions, brand awareness, and value considerations.

This is a fundamentally new customer experience with significant implications for insurers’ revenues and margins. When AI controls the opening narrative, it determines what consumers are willing to consider and what they are willing to pay.

Reorienting for AI discovery

The writing is on the wall: consumers are starting their financial services shopping journeys with AI assistants, not industry-controlled channels. This shift is already forcing some firms to rethink their distribution strategies.

Online insurance marketplace EverQuote has described its strategic focus as building an “AI-optimized” upper funnel designed for a “new world of AI-driven discovery.” The emphasis is on content, quoting infrastructure, and discoverability when customers arrive with intent already shaped by AI assistants.

Wells Fargo’s AI assistant, Fargo, now handles hundreds of millions of customer interactions, acting as a front-line interface for everyday banking needs such as payments, transfers, and account inquiries. Rather than routing customers through traditional digital flows or human support, Fargo interprets intent and explains next steps directly through an AI-driven experience.

Personal lines are where AI rewrites the rules first

Personal lines are the most exposed to AI-driven, top-of-the-funnel disintermediation. Auto, homeowners, and renters’ insurance are standardized, price-sensitive products where customers have been conditioned to compare, switch, and self-direct. AI effectively removes the last remaining barrier to frictionless comparison shopping.

Historically, the first point of interpretation — What’s covered? What matters? What’s a fair price?”— came from within the industry through its agents, call centers, marketing, advertisements, and comparison sites. Today, that first contact is shifting outside the industry’s sphere of control and into the hands of AI assistants. Consumers still comparison shop, but the narrative shaping that comparison is authored by generative models, not carriers.

This creates a deep strategic risk for the industry: insurers are being forced to compete on terms they did not design.

The threat is not that AI will get things wrong. The threat is that AI decides what matters.

In this environment, insurers compete on explainability and relevance as much as price. Pricing structures that rely on explanation weaken. Differentiation embedded in product complexity disappears. Value is reduced to simple labels such as good value, expensive, or confusing.

Carrier’s pricing and packaging strategies were not designed with these constraints in mind. Once value is framed upstream, pricing, underwriting, and retention actions become reactive. Marketing shifts from shaping demand to competing for inclusion.

A broader pattern across financial services

The shift underway in insurance mirrors a larger realignment across financial services.

In wealth management, institutions like Morgan Stanley are deploying generative AI tools to help advisors retrieve, summarize, and explain complex investment content and client interactions. These tools point to the same underlying change: the interpretation of financial value is increasingly being delegated to AI before it reaches a human professional.

Whether the audience is a financial advisor or an insurance customer, the implications are the same. As AI becomes the first interpreter of value, complexity is compressed into simple, digestible narratives. Financial institutions lose the ability to rely on mediation provided by relationship managers, advisors, or insurance agents to explain differentiation.

How C-Suite should respond

The strategic priority is no longer how quickly a firm can deploy AI internally. It is whether the business is ready to be interpreted externally.

Leaders should be pressure-testing:

How would an external AI describe our value proposition today?

Which elements of our pricing or packaging depend on human explanation to uphold?

Where does our customer journey assume effort or patience from the buyer?

Which competitors would appear stronger when evaluated by a neutral, AI-generated comparison?

These are diagnostic questions about exposure, not technology maturity. They require leadership visibility into how AI surfaces, summarizes, and ranks the firm’s offerings in actual buying situations.

Key takeaway

Customers will increasingly use AI to shop for personal lines insurance because it reduces effort and increases clarity.

The issue is whether insurers are prepared to compete when AI, not humans, becomes the primary interpreter of value.

Readiness starts with understanding how existing distribution and value propositions perform when no one is helping explain them.