In the third edition of our External Asset Management (EAM) Market Study, we assessed the Swiss EAM business and highlight market dynamics. Here, we share industry best practices and insights into growth trends.

For our EAM Market Study, we interviewed eight prominent banks operating in Switzerland. We focused on five key dimensions encompassing various aspects of the business – key performance indicators (KPIs), product landscape, competitive advantages, pricing structure and methods, and client profitability management.Here’s a summary of the most important insights and trends to watch out for in the EAM business.

At a glance

- A few big players dominate both the Swiss and global EAM markets.

- Custodian services, experienced front office staff, and flexibility on pricing and services are the three key value drivers today.

- In the future, user-friendly, high-performance digital platform and experienced, high-quality front office staff are projected to be the main value drivers.

- Banks generally have a business size threshold at which they start to structure their product and service offering.

- Swiss EAM market increasingly leaning toward excluding retrocession from pricing.

- The largest banks use tools to support their discounting processes and regularly carry out profitability checks and correct unpriced relationships.

Three major KPIs for measuring business success

Asset volumes

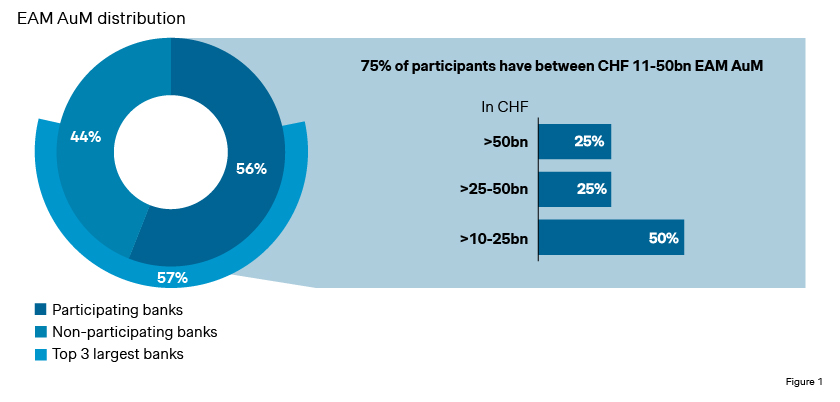

Three banks exert control over approximately 60 percent of the total Swiss market landscape, representing around CHF 350 billion in assets under management (AuM). Additionally, our study shows the importance of EAM activity varies among banks, not only in terms of EAM assets, but also in relation to total banking activities.

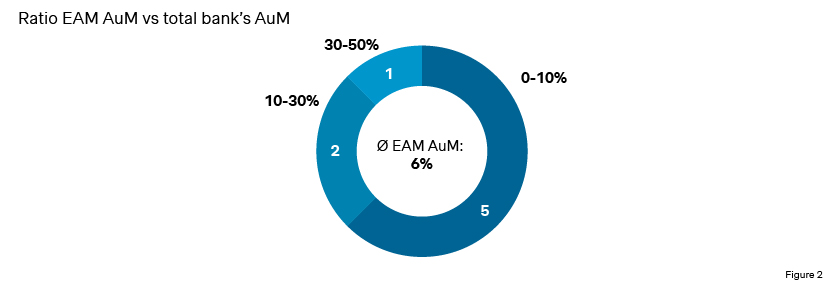

For around 60 percent of participants, the EAM activity represents a small part of their total activity, with a low EAM AuM ratio (0 to 10 percent). On the other side of the spectrum, the bank with the highest EAM AuM ratio does not surpass 50 percent.

What does this mean?

While several banks view the EAM business with apprehension, perceiving it as a competitive threat that could potentially disrupt their traditional operations, other banks possess a more progressive outlook. These banks recognize EAM not only as a lucrative revenue stream but also as an intrinsically attractive business segment that can diversify their service offerings and client base.

Return on Assets (RoA)

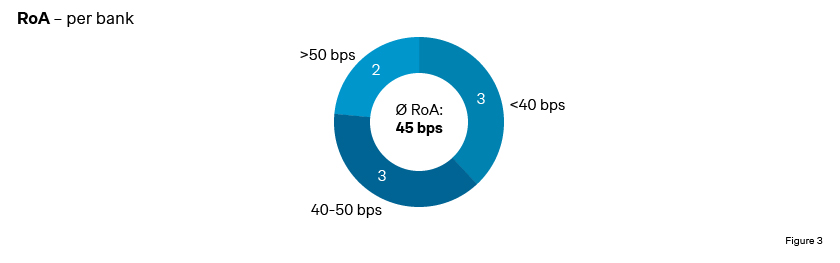

Banks achieve, on average, a RoA of 45 bps. The RoA varies widely between the participants. While three banks have a RoA below 40 bps, two of the participants have a RoA above 50 bps.

What does this mean?

Banks with relatively low margin should consider introducing revenue development measures. One approach involves revamping the offering by bundling services together to monetize them more effectively, as many value-added services are still offered free or at a substantial discount. Additionally, banks must monitor the profitability of each EAM on an annual basis and reconsider the pricing agreement if profitability is deemed too low or unsatisfactory. Finally, it is time to pass on to clients the growing operational costs that most banks are facing. For instance, some banks are already applying surcharges for labor-intensive, high-risk EAM to account for the substantial increase in legal and compliance requirements over the years.

Stakeholder relationship

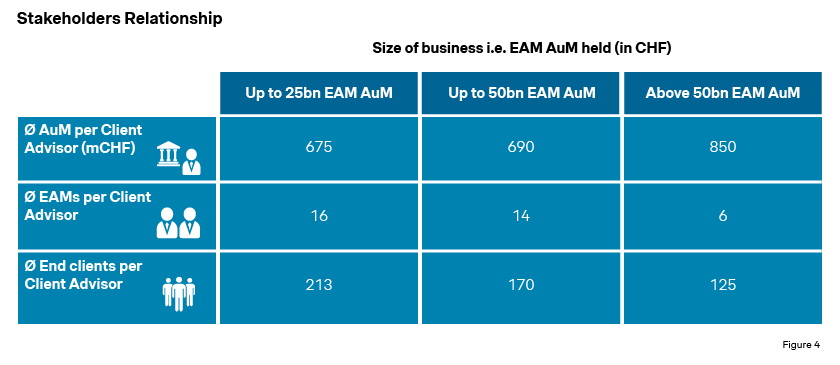

Banks with AuM up to CHF 25 billion have client advisors that manage an average of CHF 675 million. Each client advisor serves an average of 16 EAMs and 213 end clients. Interestingly, as the bank’s business grows, the number of EAMs and end clients served per client advisor decreases while the average AuM generated per client advisor rises. This shift suggests that larger banks are able to cater to larger EAMs.

What does this mean?

The average number of EAMs and end clients per client advisor is expected to change significantly in the future, due to cost-saving opportunities in serving smaller EAM relations more efficiently. Banks are adopting digital self-service solutions for EAMs with low asset volumes, instead of using expensive client advisors. Banks should further explore the scalability of their operations and consider strategies for efficiently serving their EAMs and end clients today and in the future.

Providing the right service level and the appropriate distribution channel

Our study has identified a threshold at which participants start structuring their offerings. Banks with less than CHF 25 billion AuM adopt the all-you-can-eat approach, which implies offering the complete range of products and services to all EAM clients in a bespoke manner. In contrast, banks holding over CHF 25 billion in AuM have a more structured approach. They generally offer access to different service levels according to the individual EAM business case.

The biggest challenge for banks is to provide the right offer to the right EAM and to avoid granting its full range of high-end services to unprofitable relationships. The best practice is to offer a fully digitized service to small and low-profitability clients. Meanwhile, more profitable clients or those with high development potential are offered a more personalized service with the bank’s expert teams.

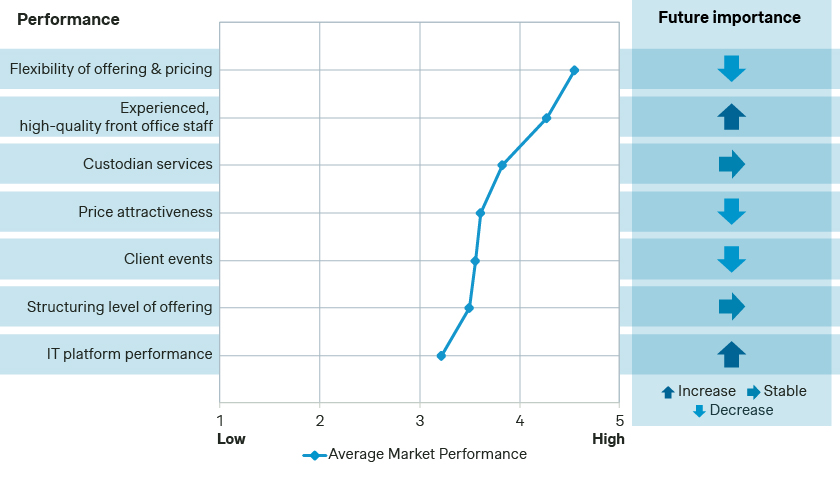

Quality services and a high-performance digital platform are the industry's key value drivers

Custodian services, flexibility on offering and pricing, as well as experienced, high-quality front office staff are key value drivers in the Swiss EAM market today. Participants unanimously believe that user-friendly, high-performance digital platform combined with experienced front office staff will be critical drivers for future success.

EAMs are already increasingly asking for access to ready-to-use IT solutions (e.g., performant data feed and interface with their Portfolio Management System (PMS) and state-of-the-art reporting solutions. Providing a high level of custodian services combined with performant digital platform is critical to retaining the current client base and attracting new clients. While large banks already have high-performing platforms, smaller players that are lagging should strongly invest in that area to narrow the performance gap.

Finally, flexibility remains crucial in the EAM business, particularly due to heavy customization demanded by the B2B nature of the activity. Large banks are likely to encounter limitations in customizing their offering and pricing due to their standardization processes, whereas smaller banks are more likely to offer customization. Banks need to find the right balance between flexibility and standardization. To do this, they will need tools to define which relationships deserve a certain degree of service personalization, and which, on the contrary, should benefit solely from standardized services

A step forward in retrocession free pricing model

In the Swiss EAM market, there is a significant gap between list prices and effective prices paid by EAMs. As pricing negotiation is a common practice in the EAM market, external asset managers typically seek competitive and cost-effective solutions for their clients. Therefore, although the list price serves as a reference point during negotiations, prices are extensively tailored and adjusted to meet the specific requirements of individual cases.

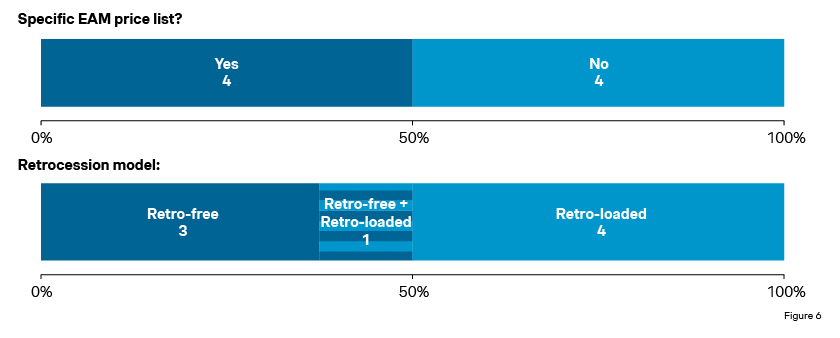

According to our research, half of the study participants do not have a dedicated EAM price list and instead align their pricing with private banking. Additionally, more than one-third of the participants proactively offer retro-free models, while half still incorporate retrocessions in their official pricing models. It is worth noting that a hybrid model that combines both has also been seen.

In order to provide support and guidance to client advisors during the negotiation and pricing process, banks with cutting edge technology use a dedicated tool to evaluate individual business cases and understand the impact of potential discounts.

What does this mean?

There is a growing demand for retro-free pricing models driven by their numerous advantages (see also: Future trends to watch out for in the EAM market - Retro-free model). Banks that have not yet embraced this approach should carefully weigh the pros and cons and evaluate whether aligning themselves with this emerging industry trend is worthwhile.

Additionally, as prices are frequently subject to negotiation, client advisors would benefit from internal pricing guidelines to act as a point of reference. These guidelines serve as a valuable framework for effective client negotiations, guaranteeing that discussions are transparent and aligned with the bank’s objectives. This structured approach not only streamlines client interactions but also fosters consistency throughout the entire price negotiation process.

Ultimately, incorporating simulation tools into the negotiation and pricing process helps client advisors define business cases more effectively and improves pricing negotiations. Simultaneously, it provides management with a comprehensive view of forthcoming revenue opportunities and aligns with the bank’s profitability expectations and targets.

Future trends to watch out for in the EAM market

Alongside the business elements in the current market landscape, banks must also be on the lookout for these future trends.

Retro-free model: The retro-free model is increasingly popular in the Swiss EAM market, as it allows for various advantages, such as greater cost transparency and reduced operational work. This model also ensures a better alignment with industry best practices and market demand, as well as regulatory requirements. While the Swiss regulations currently in force do not prohibit the practice of retrocession in the EAM market, other regions already prevent this practice. Finally, offering a retro-free model not only helps to align the bank with current and future regulatory requirements but also demonstrates a commitment to ethical and responsible business practices.

Regulatory and compliance increasing cost: Regulatory changes aimed at increasing market transparency may influence the EAM business in the future. Besides retrocessions, the business could be confronted with other obligations, such as sustainability-related disclosure requirements. These disclosures, which aim to provide transparency to investors and other stakeholders about the sustainability aspects of financial products and services, are likely to affect the EAM business. These increased regulatory requirements and the need for transparency vis-à-vis the regulator and the various stakeholders will have a growing impact on banks in terms of administrative work. In order to maintain their margins, banks will have to pass on some of these administrative costs to their clients.

Digitalization: The EAM business is expected to continue to be influenced by digital technologies. It is becoming increasingly important to have a user-friendly, high-performance digital platform with increased connectivity capabilities to best serve EAMs and their needs. Digitalization is a key differentiator and the banks that adapt strategically to these technological advances are well equipped for success.

Time to act

The EAM business sector is undergoing profound changes. While our study focuses on the Swiss EAM landscape, carefully investigating the business elements and markets trends, following these insights will be equally beneficial to other regions.

Banks must remain cognizant of upcoming changes in regulations as they drastically influence the business model while imposing stricter transparency and generating additional workloads.

Additionally, the rise of digitalization will further contribute to the market's evolution. Banks that can adapt to swiftly changing market conditions, skillfully navigate market uncertainty, and address evolving client needs will be strategically positioned for success.

And here’s how our team can help. At Simon-Kucher, we are experts in sustainable growth. Our team of specialists has decades of experience in helping clients defend revenue and profit margins, and successfully adapt to changing market conditions.

To learn more about the EAM Market Study, contact us today.