China's medtech market is entering a new phase – where faster innovation meets increasing access complexity. Companies that plan early for approval, access, and go-to-market will be best positioned to win in this dynamic market.

2026 marks the beginning of China's 15th Five-Year Plan, which emphasizes technology and innovation across sectors, including medical technology and consumables. Building on Simon-Kucher’s annual industry survey, a few key themes are emerging for China's medtech industry in 2026 and beyond.

The policy environment: Innovation imperatives

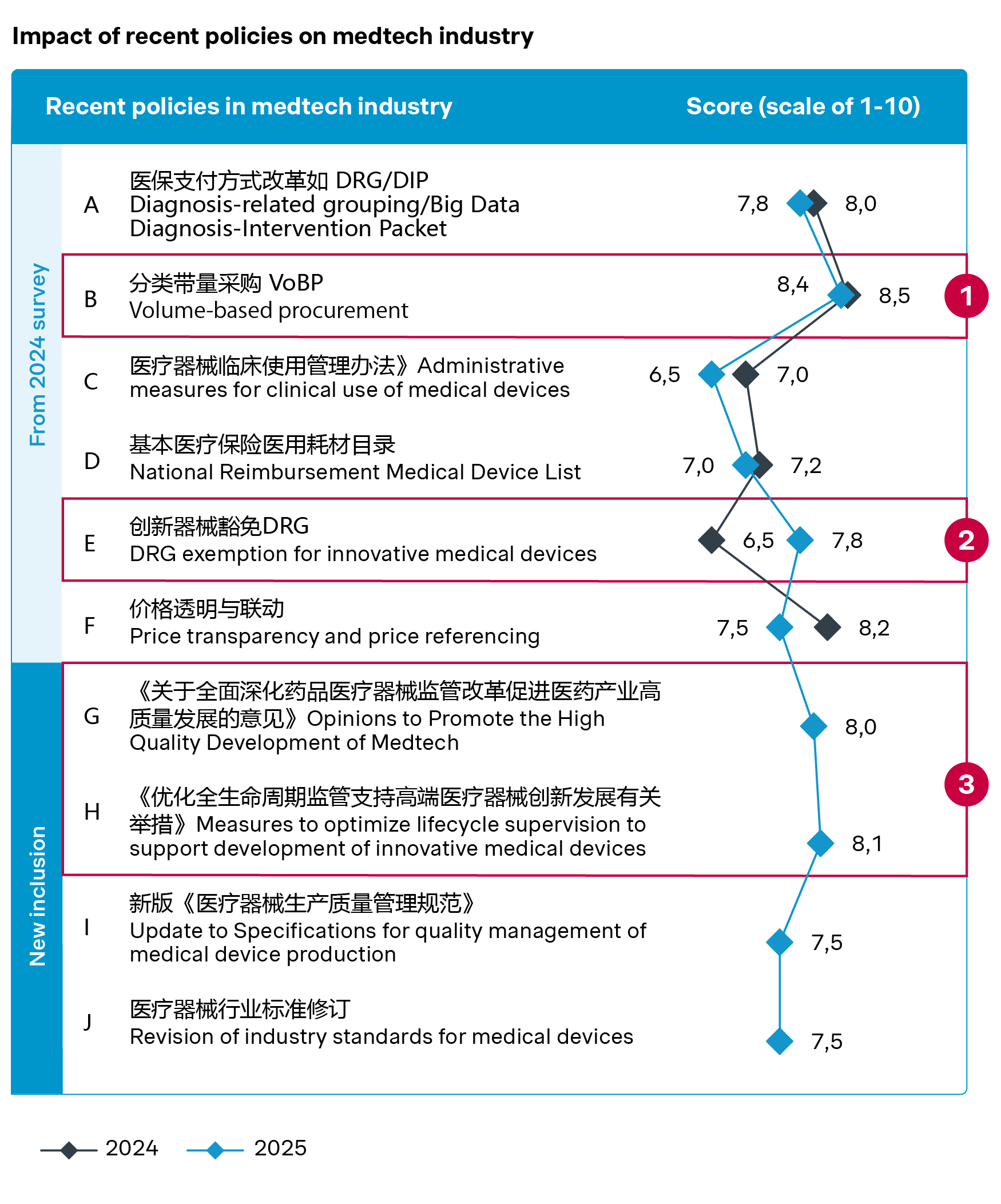

China's medtech policy environment has long been defined by two parallel forces: strong support for innovation and ongoing price pressure on mature product categories. This dynamic is unlikely to change structurally, but there are several notable new developments. This includes the State Council's opinions on promoting the high-quality development of medtech devices and the National Medical Products Administration's measures to optimize lifecycle supervision to support development of innovative medical devices.

| New developments and key takeaways |

| Deepening regulatory reform |

|

| Continued DRG/DIP with regional breakthrough |

|

| Broadening VoBPs |

|

Source: Simon-Kucher insights

These policies are expected to:

- Accelerate regulatory timelines through tailored guidance, priority review for high-end devices like medical robots, and clinical trial exemptions for rare disease devices.

- Strengthen quality requirements across the full product lifecycle, encompassing standard-setting, manufacturing compliance, and e-commerce regulation.

- Encourage “Go Local” and “Go Global” strategies in parallel to drive localization of global majors, and support the upgrading of domestic manufacturers.

Source: Simon-Kucher insights

For mature product categories, cost containment pressures persist as they are driven by new rounds of volume-based procurement (VoBP), the continued rollout of DRG/DIP payment reforms, and increasing price transparency requirements. That said, some of the policies are being refined to ensure a level playing field and avoid over-competition.

VoBP continues to expand at both national and regional levels, with increasing emphasis on sustainable and rational pricing:

- At the national level, the 6th NVBP round included drug-coated balloons and urological interventional devices. It also introduced an “anchor price” for the first time to prevent extreme low bids from distorting bidding process. The “anchor price” is the higher of 65% of the average winning bid within a group or the lowest bid in that group, setting a floor that rises with the group average. Companies bidding at or below 1.5x the anchor price are eligible to win, ensuring that NVBP outcomes reflect collective market expectations rather than isolated outliers.

- At the regional level, VoBP categories have expanded into digital medical devices. Guizhou and Ningxia launched regional VoBP programs for cloud-based medical imaging services that store patients' radiological data on remote servers instead of traditional plastic films. Hospital alliances, especially among top Class 3 hospitals such as Children’s Hospital Zhejiang University School of Medicine, are increasingly exploring device-specific VoBP models. Regional VoBP rules have been refined to accommodate different archetypes beyond traditional price-dominant approaches: winning price alignment with list price allows for price rectification, bidding plus revival secures winning opportunity, and comprehensive assessment ensures quality of awarded tenders.

DRG/DIP payment reforms will see ongoing finetuning, with the 3.0 version of CHE-DRG/DIP currently under development. At the same time, innovative technologies may qualify for exemptions – for example, Beijing has already released two batches of DRG exemption lists covering nine medical devices, including transcatheter aortic valves, atrial appendage clips, and cryo-radiofrequency ablation needles.

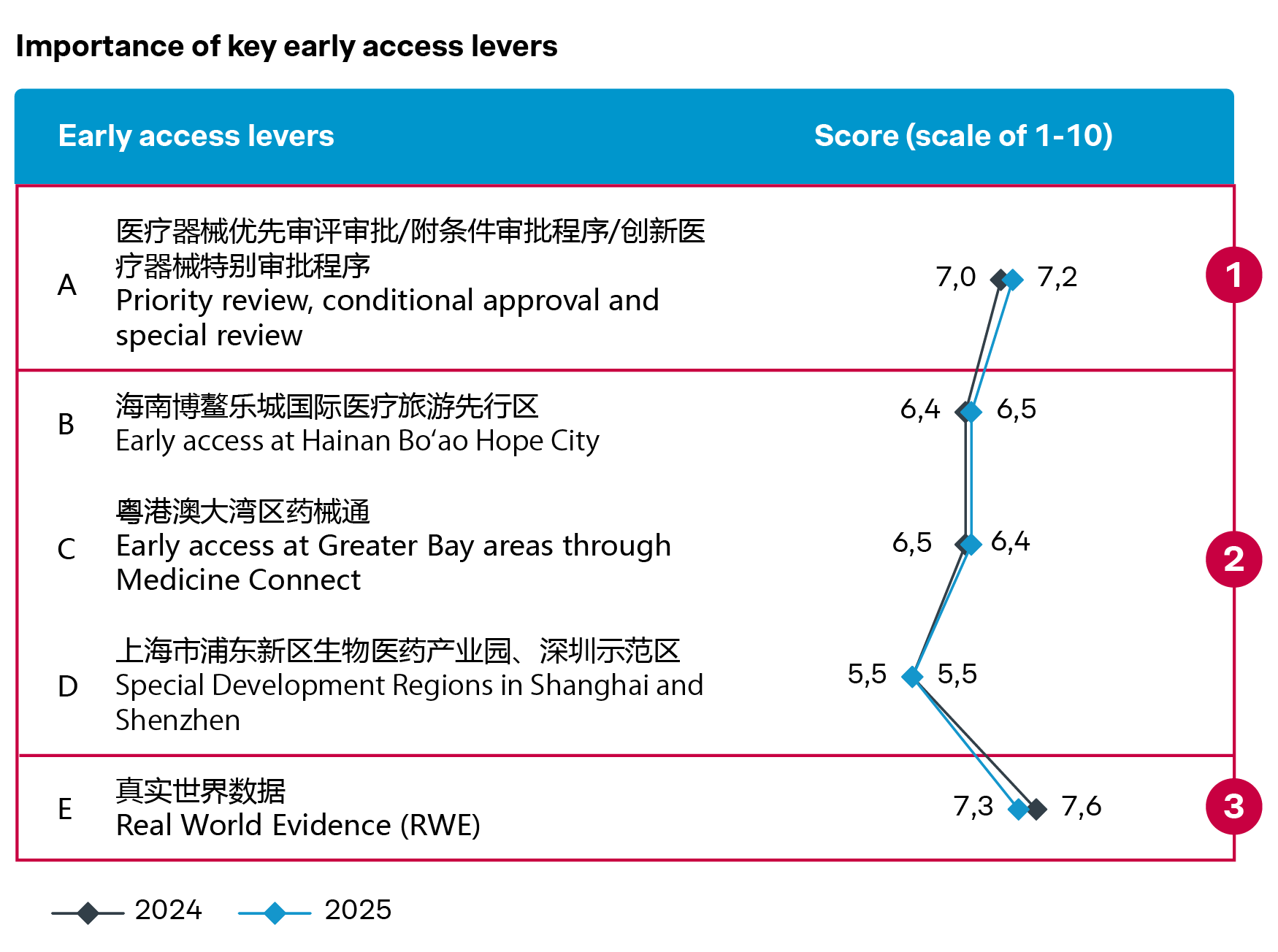

How innovative pathways and RWE are redefining market entry in China

For many leading players, market access in China starts much earlier than formal regulatory approval, through accelerated pathways, early access programs, and increasing acceptance of real-world evidence (RWE).

| New developments and key takeaways |

| Accelerated approval pathway for innovative devices |

|

| EAP in Hainan Bo’ao, GBA, Shanghai and Beijing |

|

| Increased utilization of RWE |

|

Source: Simon-Kucher insights

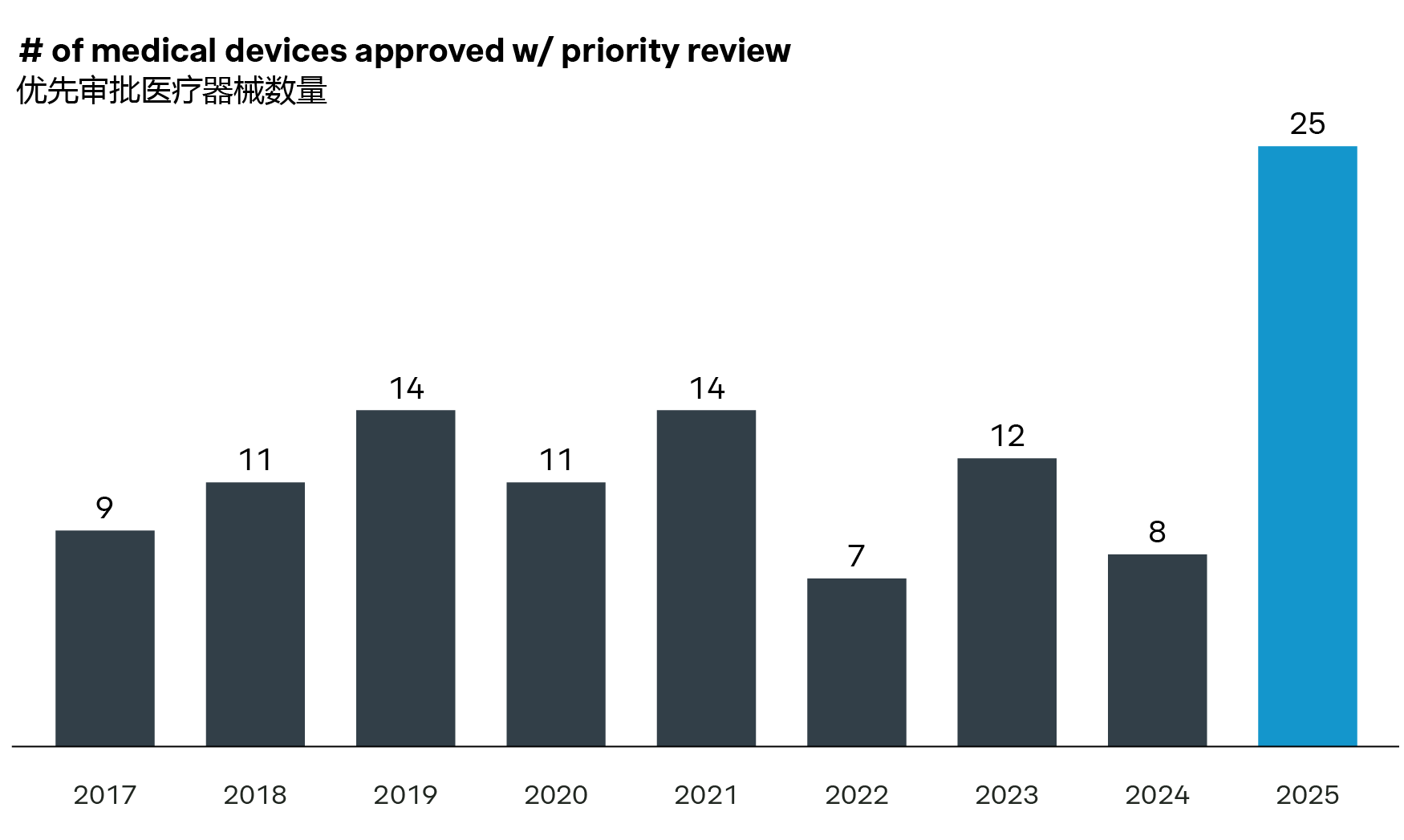

The number of medical devices leveraging special approval pathways and priority review processes reached new highs in 2025. Eight device categories are now eligible for priority review, including brain-computer interface (BCI) devices and ultra-high field MRI device. Notably, Neuracle received the first China approval for its BCI device in March 2026. This solution is an implantable BCI hand motor function compensation system for patients with tetraplegia caused by cervical spinal cord injury, enabling compensatory grasping function of the hand through a pneumatic glove device.

| List of high-end medical devices for priority review | |

8 classes of devices | |

| Product Class | Technical Parameters or Intended Use |

| BNCT |

|

| Ultra-high field MRI device |

|

| Medical electron accelerator |

|

| Implantable BCI medical device |

|

| Endoscopic surgical control system |

|

| TTVr & TTVR |

|

| Implantable glaucoma drainage device for MIGS |

|

| Membrane oxygenator (for ECMO) |

|

Source: Simon-Kucher insights

Many players are pursuing early access programs in Hainan Bo’ao and the Greater Bay Area for innovative devices, or tapping Shanghai and Beijing’s temporary import mechanisms ahead of formal regulatory approvals. These pathways are strategic for building early clinical adoption and market presence – some notable examples are TricValve® Transcatheter Bicaval Valve System and VISUMAX 800 SMILE Pro.

Crucially, real-world evidence is playing a key role across these pathways. Beyond supporting regulatory approval, RWE is also strengthening clinical acceptance and reimbursement down the road. For example, the VENTANA FOLR1 (FOLR1-2.1) RxDx Assay invested in real-world study in conjunction with its early access in Hainan, contributing significantly to its successful commercial launch.

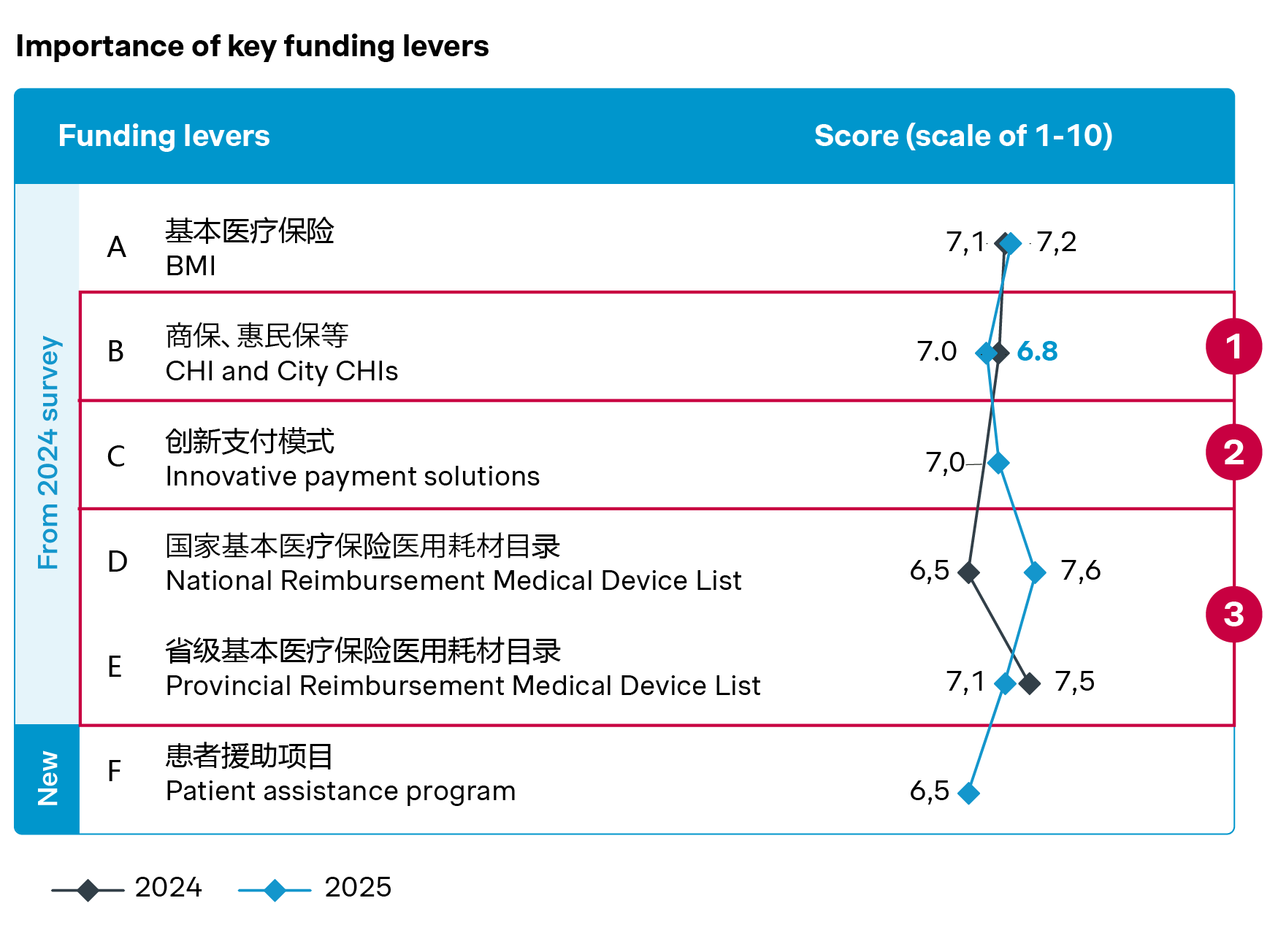

A more diversified funding landscape takes shape

China’s public reimbursement system continues to develop, with provincial reimbursement medical device lists (PRMDL) expanding steadily and laying the groundwork for nationwide rollout. To date, 24 of 32 provinces have published their PRMDLs, most of which distinguish reimbursable medical devices from service bundles. Some provinces have also announced additional inclusions for new products and VoBP winners.

These developments are improving transparency and standardization, but may also introduce more structured price negotiations and evaluation processes moving forward.

| New developments and key takeaways |

| Further rollout of PRMDL and application of BMI coding |

|

| Increased presence of CHI and City CHIs |

|

| Emerging innovative payment solutions |

|

Source: Simon-Kucher insights

At the same time, alternative funding channels are also taking off. Commercial health insurance (CHI) and city-level insurance schemes are increasingly covering innovative and high-cost technologies, offering patients earlier access while reducing their financial burden.

| Therapy | Renatus | Inspace system | Optune |

| Company | Balancemed | Stryker | ZaiLab |

| CHI inclusion | CHI for for pre-existing conditions: “RenHuXinSheng” | 3+ CHI included Inspace system in its innovative medical device list | 70+ City CHIs, including Beijing, Hangzhou, Chongqing, Hunan, etc. |

| Description |

|

|

|

| Key stakeholder |

| ||

| KSFs |

| ||

Source: Simon-Kucher insights

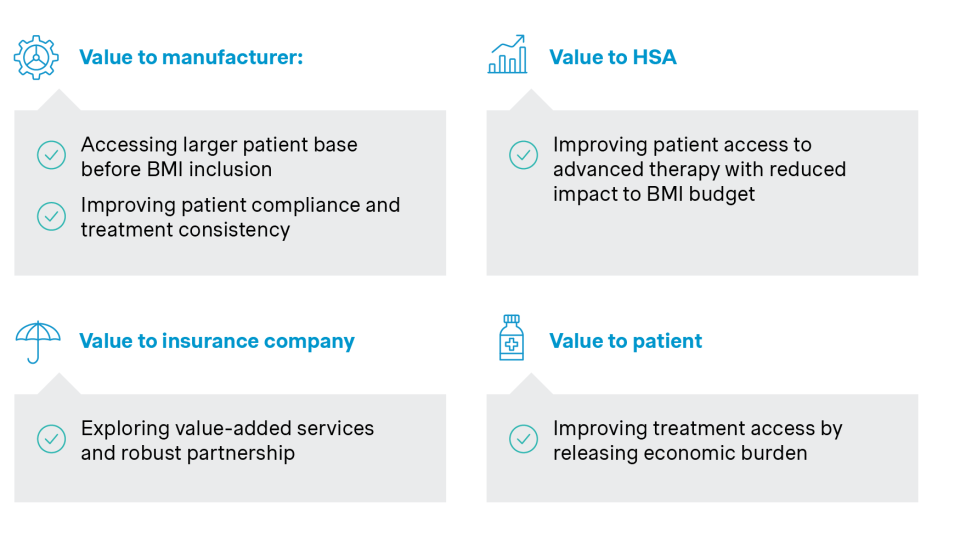

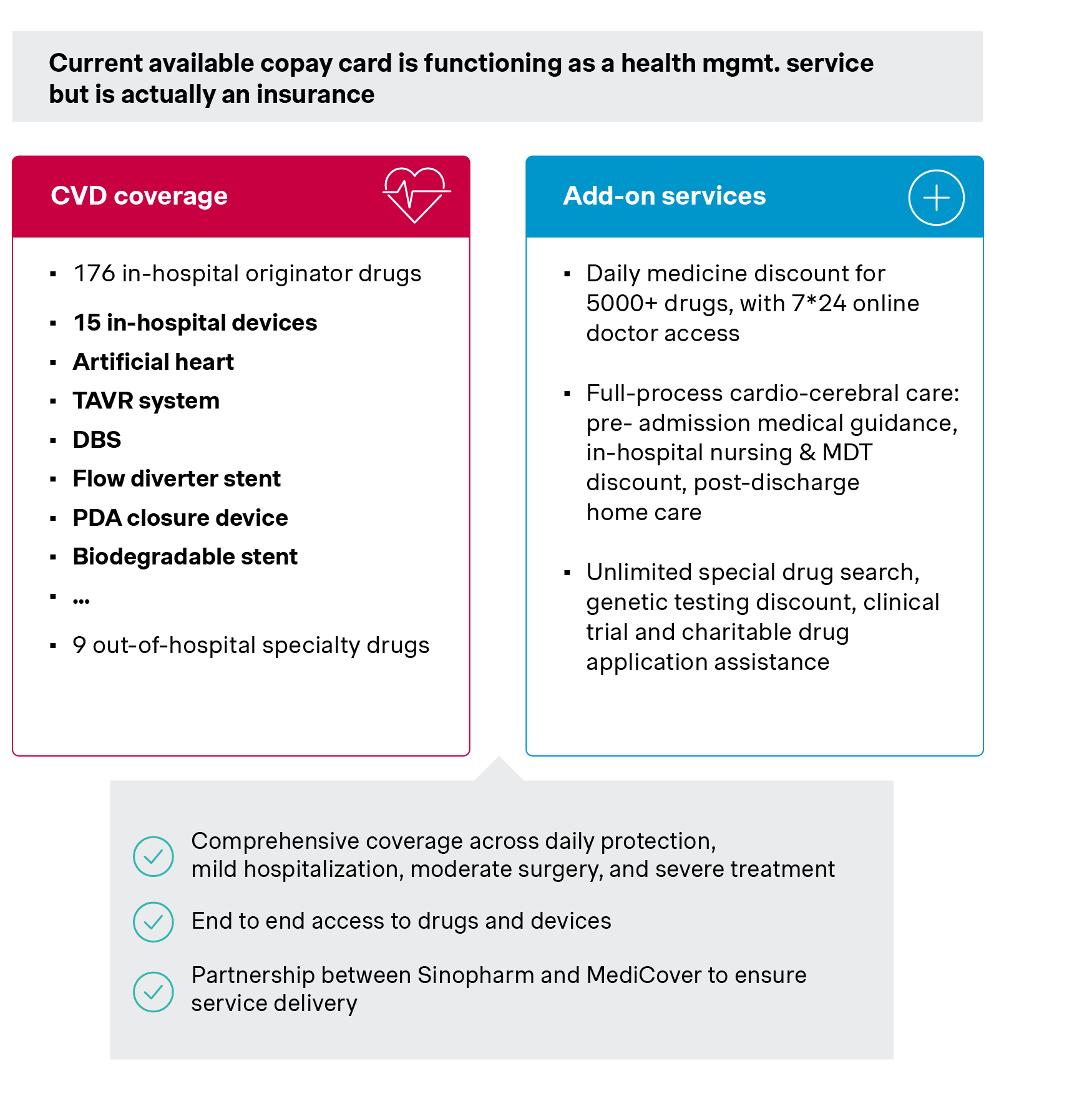

Alongside this, new payment models that integrate devices, services, and financing mechanisms into more holistic offerings are gaining momentum. EVAHEART I (left ventricular assist system) and Evolut PRO (transcatheter aortic valve system), for example, have leveraged copay cards, to improve affordability, enhance patient experience, and support treatment continuity.

| MediCover Copay card | |

| Patient journey step | Included services |

| Daily protection |

|

| Outpatient | |

| Hospitalization – mild | |

| Surgery – moderate | |

| Severe treatment | |

| Long-term nursing | |

Source: Simon-Kucher insights

Taken together, these shifts point toward a more diversified funding landscape – one that requires medtech companies to think beyond traditional reimbursement and engage with a broader ecosystem of payers and partners.

What it takes to compete in China medtech's next chapter

With these developments in the industry policy and access environment, China's medtech market will see more changes ahead. 2026 may prove to be an inflection point, in that companies that are better prepared stand to gain disproportionately. The 15th Five-Year Plan will only accelerate this trajectory, and the winners will be the ones that sharpen the focus on innovation, improve market access readiness, and capture emerging opportunities for reimbursement and go-to-market models.