The recent national drug price negotiations in China and subsequent national reimbursement drug list (NRDL) inclusion for select innovative medications have opened the door to new marketing and reimbursement possibilities. The negotiations seem to be ushering in a new era where manufacturers are operating in a larger reimbursed market and Chinese patients are offered cost relief. Simon-Kucher analyzed the negotiation results, and identified insights and key learnings for manufacturers.

Growing reimbursement opportunity for innovative drugs

Marketing high-cost, innovative drugs in the Chinese market has been a long-standing struggle for manufacturers given low patient out-of-pocket (OOP) potential and reimbursement challenges. Innovative drugs are typically launched in China without reimbursement, which means manufacturers typically rely on patients to pay OOP for their product for at least three to five years after launch before achieving reimbursement.

The Ministry of Human Resources and Social Security (MoHRSS), China’s government authority responsible for reimbursement decisions, has only updated the NRDL twice in the last ten years, once in 2009 and again eight years later in February 2017. The 2017 edition of the NRDL contains 2,535 drugs, including 1,297 Western medicines1. The updates were based on votes from national expert committees consisting of clinical, pharmaceutical, HEOR, and pharmacoeconomics experts.

Following the February 2017 update, the MoHRSS conducted price negotiations with the manufacturers of 44 patented or exclusively-supplied drugs which are higher cost but offer high clinical value. In July, the government announced that 36 drugs passed the negotiation and are all listed on NRDL Tier B with a 10-20% patient co-pay. On average, these products took a 44% price cut compared to their previous tender price. Among these 36 drugs, 31 are Western drugs and 5 are TCMs2.

MoHRSS negotiation structure and implications for manufacturers

Manufacturers have historically had low visibility into the process and timeline for selecting products to enter MoHRSS negotiations. The 2017 national drug price negotiations provided increased clarity and transparency into the negotiation process, which is separated into three phases:

- Pre-selection of drugs for negotiation: The drugs that participate in the negotiation are selected by roughly 4,000 individuals nation-wide who are experts in clinical and pharmaceutical medicine, medical insurance, and pharmacoeconomics. Historically, manufacturers have not been able to proactively apply to participate in price negotiations.

- Set negotiation target price: The MoHRSS sets up two independent groups to evaluate the appropriate target price for negotiations: the Pharmacoeconomics Evaluation Group and the Reimbursement Funding Capacity Group. The groups determine one target price following separate evaluations of a given product’s clinical and economic profile. The entire process is highly confidential and manufacturers are not given insight into the government’s negotiation target price.

- Negotiations with manufacturers: There are two possible scenarios that can unfold during the negotiation phase. In one scenario, the price the manufacturer offers exceeds the government’s pre-set negotiation target price by more than 15%, causing the negotiation to cease and fail. In the second scenario, the price offered is ≤15% above the government’s target price, allowing manufacturers to enter into the negotiation. The final negotiated price that the manufacturer and MoHRSS agree upon cannot exceed the government’s original target price.

The confidential nature of the negotiations creates many unknowns: if and when a drug can participate in the negotiation, what negotiation target price the government will set, and whether the negotiation will be successful. "The uncertainty around time to negotiation means that manufacturers must carefully consider whether they will pursue a low list price strategy (to pursue wide adoption) or a higher list price strategy combined with a patient assistance program (PAP)." These strategies could have different effects on product uptake and future price potential in China.

What are Patient Assistance Programs (PAPs)?

Patient assistance programs (PAPs) are funding mechanisms commonly used in China by manufacturers of innovative therapies to maintain a high list price at launch while reducing patient OOP and encouraging uptake. There are mainly two charities that work with manufacturers to provide discounted drugs to patients. Most PAPs in China are designed as a “Buy X, Get Y free” offering.

Manufacturers may want to maintain a high list price for a number of reasons. For example, keeping a high list price is beneficial if the manufacturer is planning an indication expansion into a disease area with a higher willingness to pay. China does not allow indication-based pricing, so if the manufacturer initially launches at a low price and expands into an indication with a higher willingness to pay, they will not capture the higher price potential in the new indication.

The role of PAPs in the negotiations

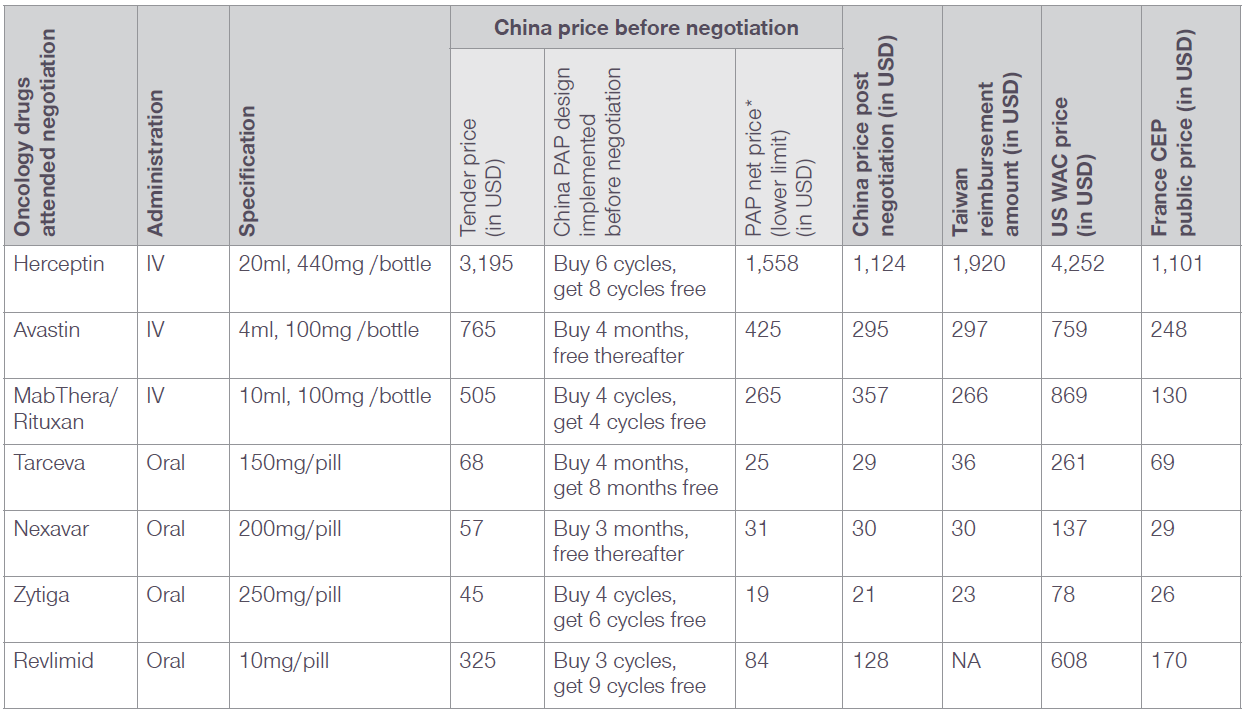

Let’s take a closer look at select oncology products to illustrate the role of PAPs in negotiations. The PAPs offered by the seven oncologics listed in Table 1 provided a 47% discount to patients on average, with discounts ranging from 25% to 56%. The majority of these programs were designed as “Buy X, Get Y Free,” while a few (Avastin and Nexavar) were structured as a “Buy X, Get the rest Free” program.

Table 1: List price, PAP price, and reimbursement price for oncology drugs vs. other list prices

Exchange rates: 1 CNY = 0.1478 USD, 1 EUR = 1.0917 USD, 1 TWD = 0.0328 USD; Simon-Kucher analysis

* For oncology drugs, PFS was used to calculate the length of usage.

The calculation of PAP net price is based on the assumption that patients would take full advantage of the PAP, therefore, the PAP net price represents a lower limit of the possible net prices.

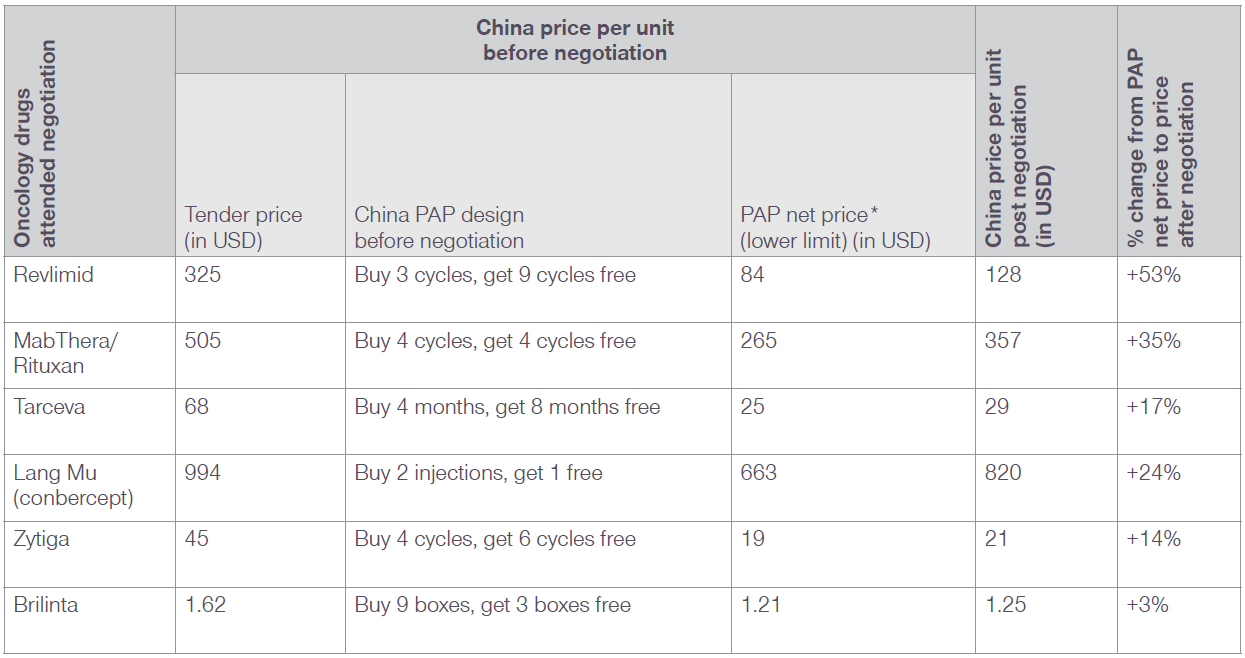

Avastin reduced its price the most during the negotiation, reporting a 31% decline compared to its PAP net price. MabThera/Rituxan, Tarceva, Zytiga, and Revlimid all negotiated prices that were up to 14-53% higher than their PAP net prices, as seen in Table 2. Given the limited 10-20% patient OOP copay for products listed on NRDL Tier B, oncology patients using these therapies are expected to see their OOP cost drop 60-80%.

Table 2: Branded products that negotiated a higher NRDL reimbursement price than the PAP net price

Exchange rates: 1 CNY = 0.1478 USD

* For oncology drugs, PFS was used to calculate the length of usage.

The calculation of PAP net price is based on the assumption that patients would take full advantage of the PAP, therefore, the PAP net price represents a lower limit of the possible net prices.

As shown in Table 2, only 2 other therapies with PAPs in place were able to negotiate a price that was higher than their PAP net price. There were only 7 other therapies with PAPs that were successful in the negotiations, however their negotiated prices were below their PAP net price.

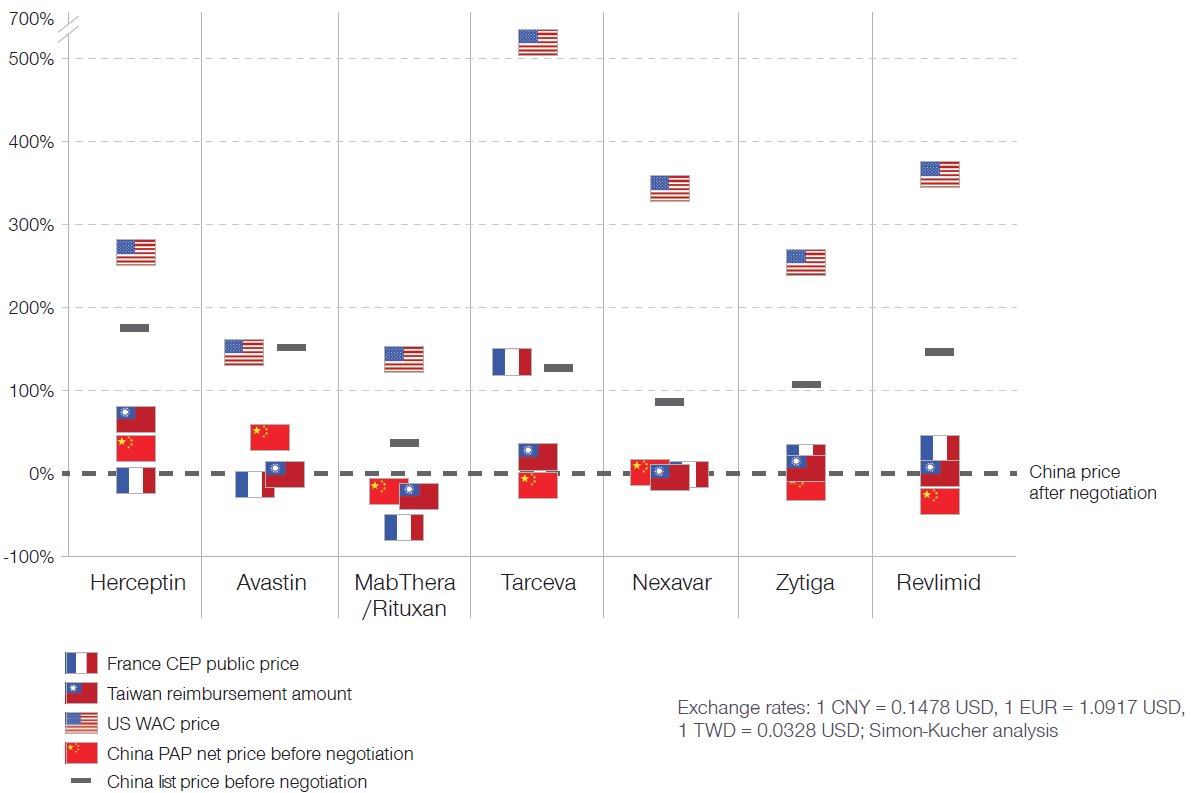

Figure 1: Change in list price post-NRDL negotiation

Exchange rates: 1 CNY = 0.1478 USD, 1 EUR = 1.0917 USD, 1 TWD = 0.0328 USD; Simon-Kucher analysis

Comparing the negotiated price with prices in Taiwan, France and the US, prices for all oncologics with PAPs were all very close to the list price in Taiwan, with the exception of Herceptin (Figure 1). This result is in line with a trend identified by some policy experts that the Chinese government may reference drug prices of surrounding countries/regions when evaluating reimbursement prices for drugs in China.

Selection for reimbursement negotiations

Current trends indicate that innovative drugs are generally not evaluated for addition to the NRDL for at least 3-5 years after launch. Among the negotiation drugs, only Zytiga (launched in China in 2015) achieved reimbursement within 3 years. However, skepticism as to whether this trend will continue generates manufacturer concerns about profitability and uptake in the market at launch for innovative therapies. Manufacturers can neither apply nor petition for listing on the NRDL, but instead government committees determine which products will be reviewed. "Driving volume and stakeholder awareness of an innovative therapy are the primary ways to gain attention which, in turn, could encourage the committees to consider or recommend an innovative therapy for review earlier than less publicized products."

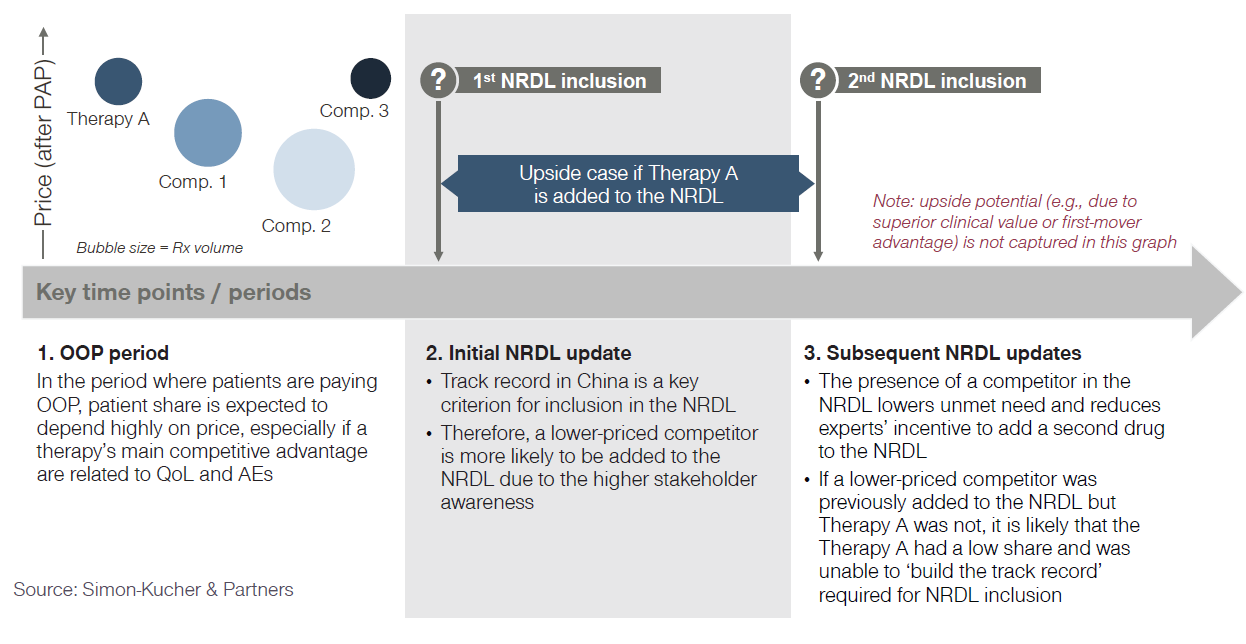

Manufacturers must consider not only their efforts to drive uptake and stakeholder awareness, but also the presence of competitors. The existence of competitor therapies is particularly important during the period when patients are paying OOP, as shown in Figure 2. Lower-priced competitor products with clinical efficacy that is equivalent to the higher-priced Therapy A are likely to have higher uptake and, thereby, higher awareness. Moreover, first movers can potentially take substantial volume with achievable price, meaning the late-comer drugs might be faced with a big hurdle in breaking into the market. This poses a challenge to the manufacturer since primary considerations when selecting products to include in the NRDL are track record and volume. Lower-priced competitors are likely to have a more-established track record and higher volume, barring any differences in efficacy. Therefore, manufacturers should fully develop not only their launch pricing strategy but they should also consider how they will react if competitors also launch in the space. If a manufacturer is prepared to react to changes in the competitive landscape, they may be able to preserve their chance at a listing on the NRDL.

Figure 2: Price-volume dynamics over time (conceptual example)

Evaluating price/volume tradeoff to prepare for negotiation

Inclusion on the NRDL means that a product will either be fully or partially reimbursed at the national level, expanding access to a substantially larger group of patients. Before going into price negotiations with the Chinese government, manufacturers need to have a clear understanding of how prescribing and uptake of their product might change in addition to the lowest price they are willing to accept to sustain a comfortable profit margin.

Price negotiations shut down immediately if the manufacturer offers an initial price that is greater than 15% above the confidential price the government sets, thereby ending the possibility that the product will be listed on the NRDL. There is currently no information or guidance as to whether there can be future negotiations for the same product if the first round of negotiations fail. It is crucial that the manufacturer understands their financial limits as well as what they realistically think will be accepted by the government.

It is also important to consider how the post-negotiation net price might change compared to the PAP net price. Following the 2017 negotiation, the negotiated prices of some drugs were higher than the pre-negotiation net price. Understanding which price (list price or PAP net price) the government used when setting their negotiation target price will be important for the manufacturer in evaluating pricing thresholds and setting a preliminary estimate of a “walkaway price.”

Pursue reimbursement through negotiation at the local level

The historical unpredictability of NRDL reviews, uncertainty around the length of time that drugs are on the market before reimbursement, and the inability of manufacturers to apply for NRDL inclusion prompt manufacturer concerns about uptake in the market at launch. While NRDL updates are the most attractive reimbursement option, there are several alternatives that manufacturers can consider, such as directly pursuing reimbursement through inclusion on the provincial reimbursement drug list (pRDL) in target provinces.

Prior to negotiating for national reimbursement, manufacturers can evaluate opportunities to get their innovative therapy listed on the pRDL. Depending on local policies, manufacturers can pursue a pRDL listing through the normal inclusion process or through negotiations. This would help the manufacturer drive awareness, achieve higher reimbursement, and access more patients. Manufacturers can strategically choose which provinces they would try to achieve a pRDL listing in to achieve optimal patient and provider awareness as well as uptake. This heightened provincial awareness and uptake could drive greater knowledge of the therapy at the national level as well.

"The Chinese government has been working to provide better and more affordable healthcare services to Chinese patients for over a decade, and the 2017 NRDL negotiation is only part of this effort to expand access to healthcare and innovative therapies." The opportunities for Western manufacturers to be involved in the Chinese market are growing, and the increased clarity around reimbursement negotiations from the 2017 NRDL update will enable manufacturers to be better-prepared when launching therapies in the Chinese market and entering reimbursement negotiations.

Potential for China launches to change pricing dynamics in Asia

Due to data requirements, launches in China have historically occurred after launches in other major markets such as Korea, Taiwan and Australia as well as the US and Europe. These products were also infrequently added to the NRDL. However, with recent changes to the CFDA approval and a robust domestic market of innovative drug development, it is likely that first-launches in China and more frequent NRDL inclusions will be a reality. Since NRDL negotiations are public, neighboring countries which do not currently price reference China may in fact look to negotiations in China as part of their domestic reimbursement approval process. "In addition, manufacturers must balance the potential volume tradeoff in China: negotiating lower prices in China with reimbursement to unlock higher volumes may offset higher prices and smaller volumes across Asia." Additionally, the decision to seek reimbursement in China may have higher stakes. Manufacturers must carefully consider two questions. First, can they afford to not offer a meaningful price cut to be on the NRDL and continue competing against NRDL-added competitors as a self-pay drug with a PAP? If they enter negotiations and an agreement cannot be made, when would the manufacturer have the chance to negotiate again?

Special thanks to Dr. Fangting Yu for providing additional insights and expertise throughout the development of this article, and also thanks to Madhurima Das, Adrien Gaussen, Kendra Jin and Jayme Leong for helping with data collection and analysis.