Telcos know their base matters, but few are fully capitalizing on it. Part 3 of our 4-part Global Telecom Study 2026 series breaks down what drives base value – from customer segmentation to ARPU acceleration – across 35 markets and 18,000 consumers.

Most telco operators focus disproportionately on customer acquisition. But the bigger commercial opportunity lies in the customers they already have, and operators who actively manage their existing base have a measurable customer lifetime value (CLTV) advantage.

Within the IBRO framework (inflow, base and renewal, and outflow), the base management approach comes down to three questions:

- Who are the focus segments in our base?

- How do we keep customers happy and engaged?

- How do we leverage those insights to drive CLTV?

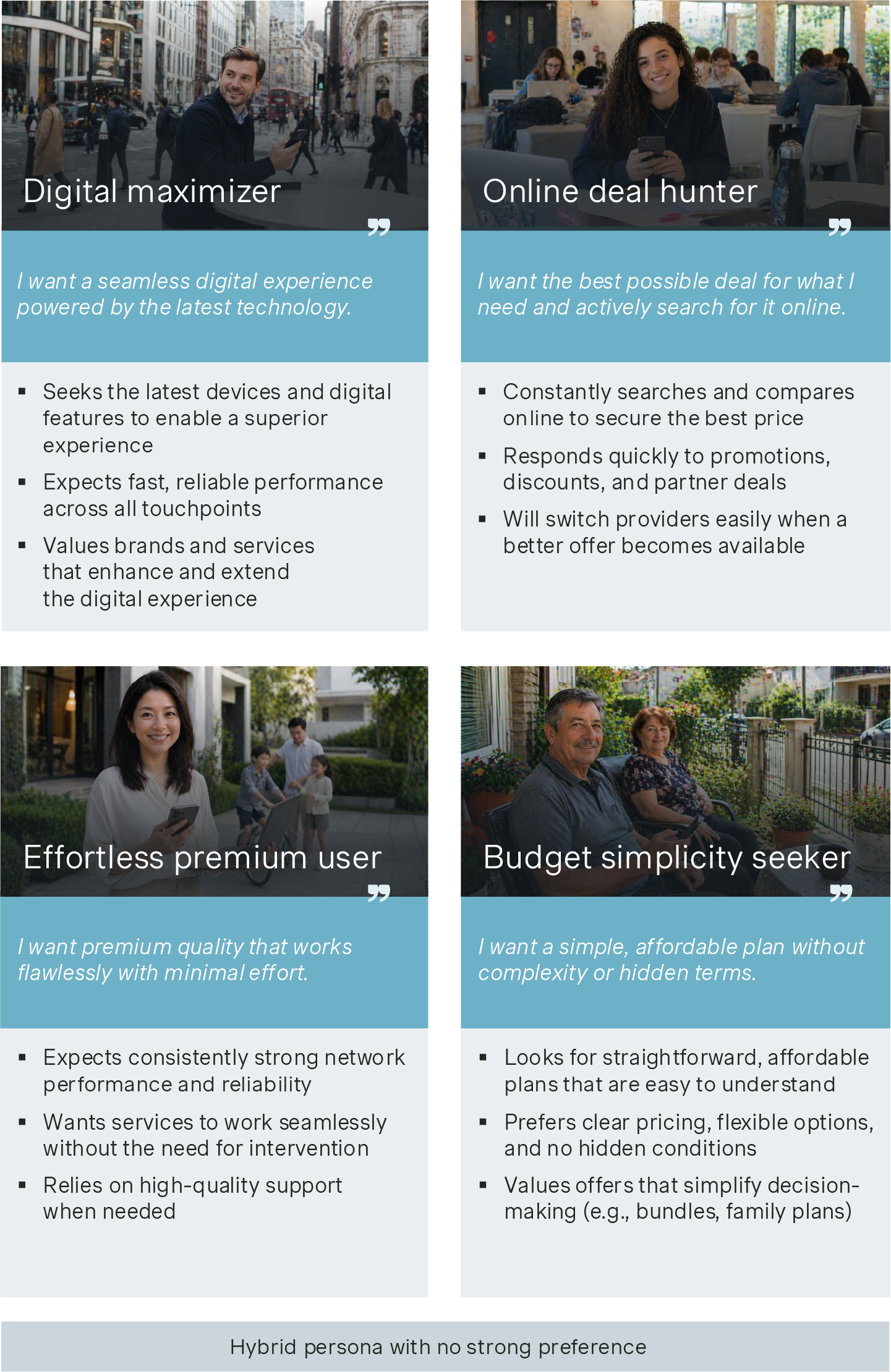

Four customer segments. Very different commercial profiles.

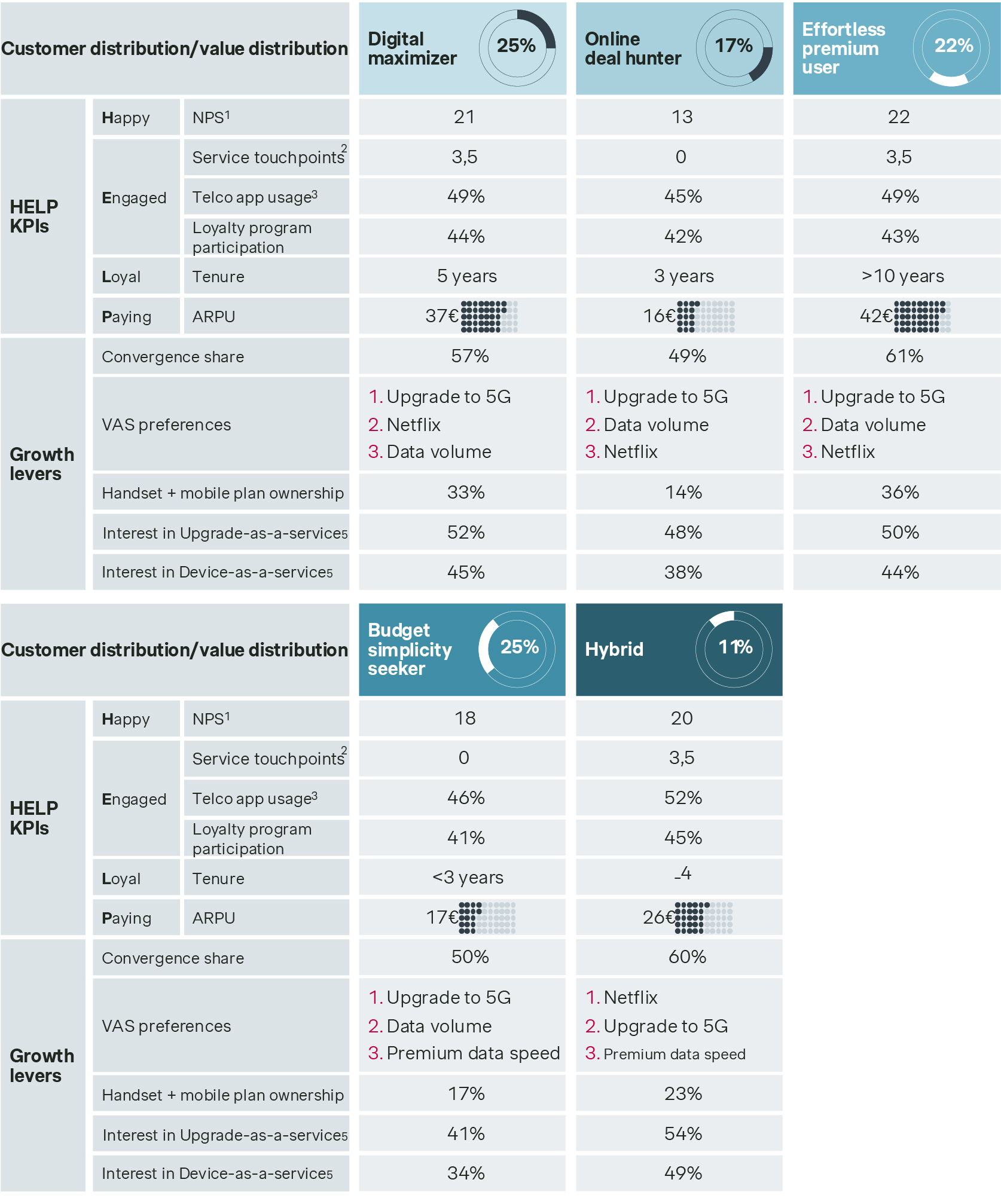

Globally, four segments steer the customer base and reflect distinct behavioral patterns: digital maximizers (25%), online deal hunters (17%), effortless premium users (22%), budget simplicity seekers (25%). An additional 11% are hybrids.

The differences in commercial value across these customer segments are quite significant. Where effortless premium users indexed at 100% ARPU over 10 years of tenure, online deal hunters average just 38% of that ARPU and three years of tenure. That gap is exactly why segment identification matters: keeping customers happy and engaged costs money, and that investment is not equally justified across the base. Telcos typically underinvest in customer experience and often fail to differentiate service levels by customer value or potential (for example, by offering a single service hotline for all subscribers). Knowing which segments are worth the effort, and where the return simply doesn’t stack up, is what separates base management from base spending.

HELP Index: Where telco customer satisfaction meets base value

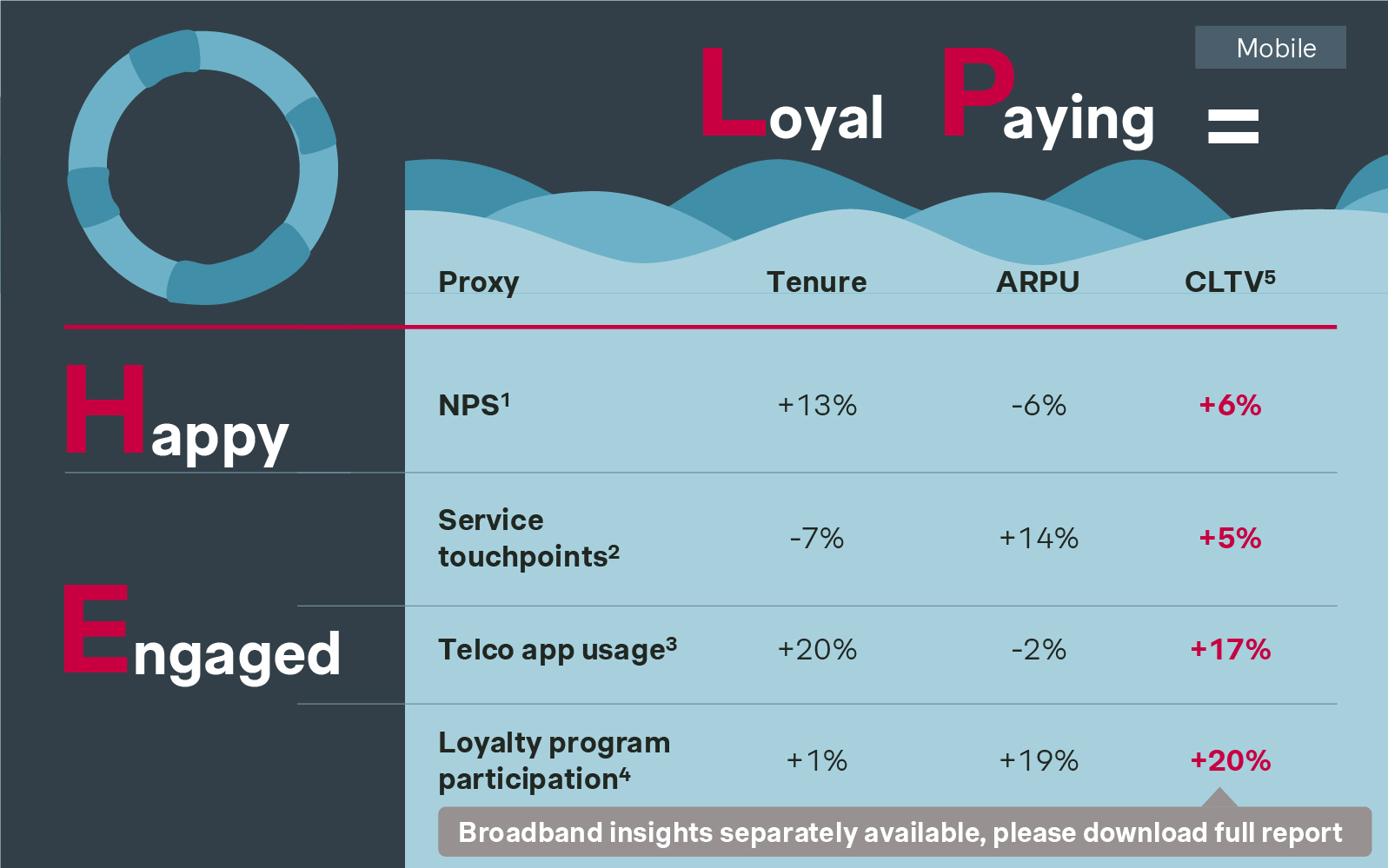

The HELP Index (Happy, Engaged, Loyal, Paying) measures the four dimensions that drive customer lifetime value. Our latest study confirms the 'Happy' and 'Engaged' pillars can move mobile CLTV by up to 20%.

Telcos broadly underperform on customer satisfaction - a vulnerability and an opportunity in equal measure. The Net Promoter Score (NPS), a proxy for customer happiness, drives a +6% CLTV uplift – not through higher spending but through longer retention: happy customers stay longer and that loyalty compensates for a –6% ARPU decline. But NPS varies across markets – highest in Southeast Asia, MENA, and Sub-Saharan Africa, while Europe and Japan fall below the global average of 17.

Service touchpoints (engagement proxy) yield +5% CLTV through consistent engagement. Telco app usage delivers +17%. App users stay significantly longer despite slightly lower ARPU (-2%). The strongest effect comes from loyalty program participation: +20% CLTV driven by a +19% ARPU lift – with strong growth potential still ahead, as only 46% of premium customers are currently enrolled in loyalty programs.

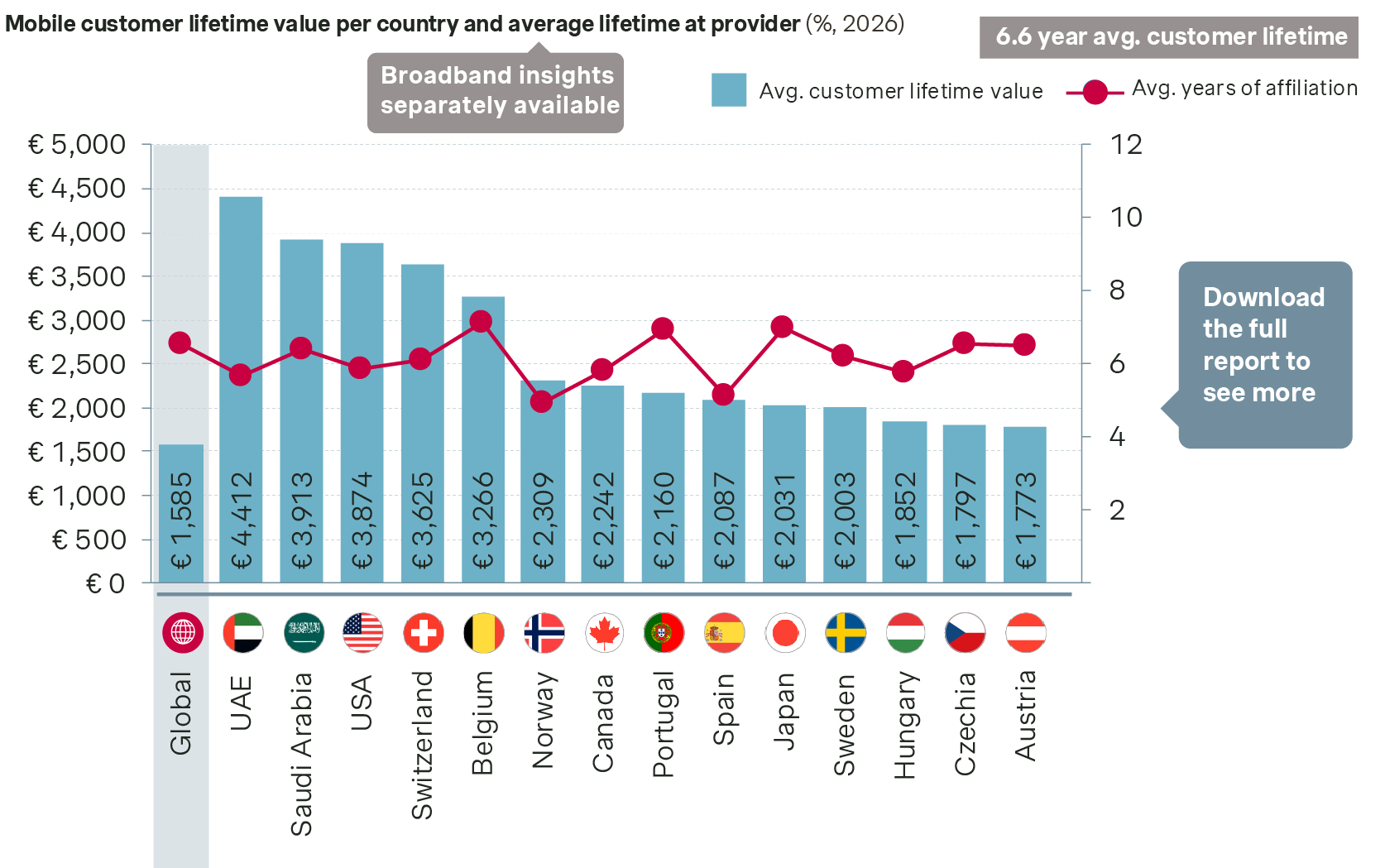

These engagement drivers translate directly into CLTV outcomes, and the gap between top and bottom markets shows the scale of the opportunity. Average customer tenure is 6.6 years globally. The range in lifetime value across the 35 markets is wide: UAE tops at €4,412 while India is at €390. Europe lands mid-pack, with the UK at €1,721, Germany at €1,621.

When it comes to the two contract types, prepaid consistently outperforms postpaid on customer satisfaction. In prepaid, STC (Saudi Arabia) and MTN (Nigeria) score 32 on the HELP Index. Among top postpaid operators – Vodafone (Portugal), Jazztel (Spain), and Verizon (the US) – the score is between 23–24.

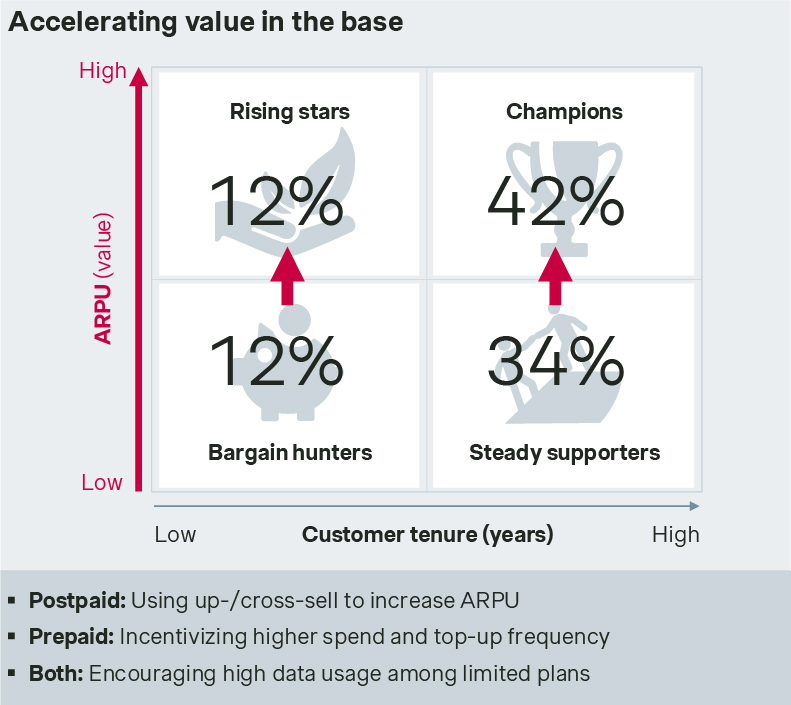

CLTV matrix: How ARPU and tenure define customer base value

Driving CLTV comes down to two levers: accelerating value in the base by moving ARPU up and loyalizing the base by extending tenure. Our CLTV matrix maps these across four customer quadrants, revealing significant commercial implications. In this blog, we focus on growing ARPU across the base.

Champions – high ARPU, high tenure – represent 42% of the base and the highest return on retention investment. Steady supporters account for 34%, loyal but slightly undermonetized. Rising stars (12%) have the spending behavior but shorter tenure. Bargain hunters, low on both dimensions, make up the remaining 12%.

ARPU growth looks different by contract type: postpaid through up- and cross-sell, prepaid through higher spend and top-up frequency. Across both, converting heavy data users on limited plans into higher tiers adds further uplift.

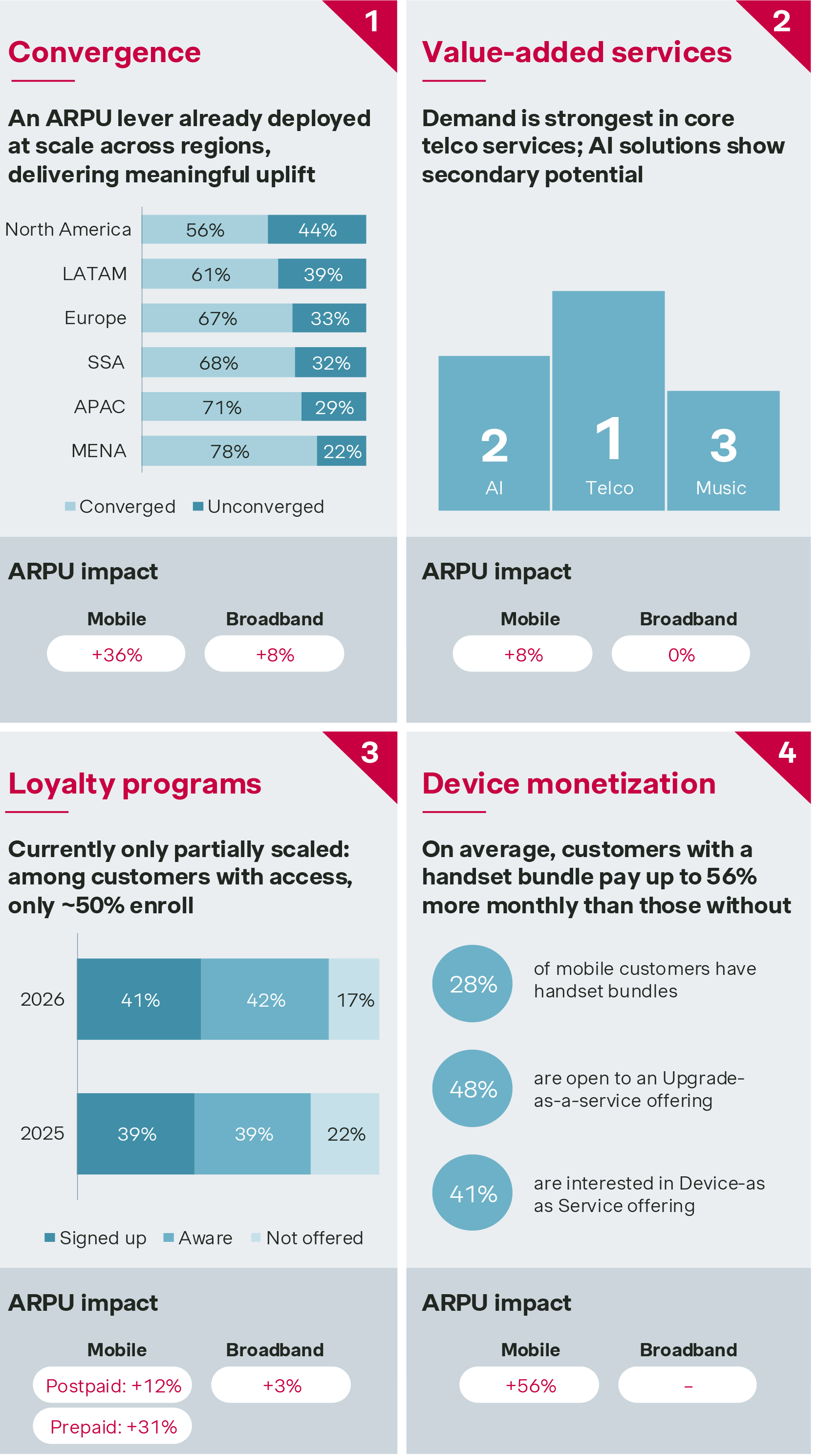

Accelerate ARPU growth with four levers already in your base

The existing base holds more revenue potential than most operators have unlocked. Our study identifies four levers that consistently drive ARPU growth across mobile and broadband, delivering measurable uplift of up to 56%. Most operators are familiar with these levers, but few have fully activated them.

- Convergence delivers a +36% mobile and +7.5% broadband ARPU uplift over unconverged customers and already operates at scale, though adoption varies widely – MENA at 78%, North America at 56%.

Opportunity: Roughly half of customers globally remain unconverged. At over 30% ARPU upside in mobile, that is a significant revenue opportunity still on the table.

- Value-added services correlate with higher ARPU as customers with VAS pay more, translating to +8% mobile ARPU uplift. Core telco services (5G upgrades and data volume) rank first in customer preference, followed by AI services and music streaming.

Opportunity: Demand is clearly there. Continued up- and cross-sell of these core VAS is an undermonetized ARPU growth lever.

- Loyalty programs exist but haven’t reached their potential. They deliver +12% ARPU for postpaid and +31% for prepaid – yet only around 50% of eligible customers have currently joined these programs.

Opportunity: The ARPU impact is notable and marked higher on prepaid. Beyond ARPU, loyalty programs drive engagement, bringing customers back to the platform more frequently to top up. Scaling enrolment is both a revenue and an engagement lever.

- Handset monetization is the highest-impact lever. While only 28% of mobile customers have a handset bundle, those who do pay up to 56% more monthly.

Opportunity: Appetite far exceeds penetration – 48% are open to Upgrade-as-a-Service and 41% to Device-as-a-Service. For telco operators, as-a-service models are the clearest path to closing this gap.

The telco customer base is not a monolith – and the operators who treat it that way will find the most headroom. The tools are already there: customer segmentation, the HELP Index, and ARPU acceleration levers. The question is how actively they are being used.

Beyond this, the industry needs to shift from a product-first to a customer-first view. Like any other mature industry, this will provide first movers with significant upsides and lay the foundation for continuous, sustainable growth.

The final instalment of this four-part series will focus on outflow: how to lock in high-value customers.

Click here to read blog 1: brand

Click here to read blog 2: inflow

Click here to read blog 4: outflow

Interested in our 2026 Global Telecommunications Study results in more detail?

Form placeholder. This will only show within the editor