In a hyper-competitive market, the traditional instinct is to chase volume which is becoming structurally dangerous. In part 2 of our 4-part series, we examine why the real challenge is no longer attracting more customers, but attracting those that operators can retain, monetize, and grow profitably over time. Results from our Global Telecom Study 2026 – 35 markets, 18,000 consumers – show where the challenge is most acute and what operators should do.

For years, telco acquisition strategy has been a volume game. Net additions and market share make growth visible and reward the teams chasing it. But a growing customer base built on the wrong customers erodes revenue, inflates churn costs, and creates a retention problem that compounds over time, resulting into a “washing machine”.

In a market defined by declining global ARPU (-2.6%), near-identical product features across operators, and budget players gaining structural momentum, who you acquire is now as important as how many.

That shift - from scale to value – is what the inflow dimension of the IBRO (inflow, base and renewal, and outflow) framework addresses.

Who is switching and why it matters

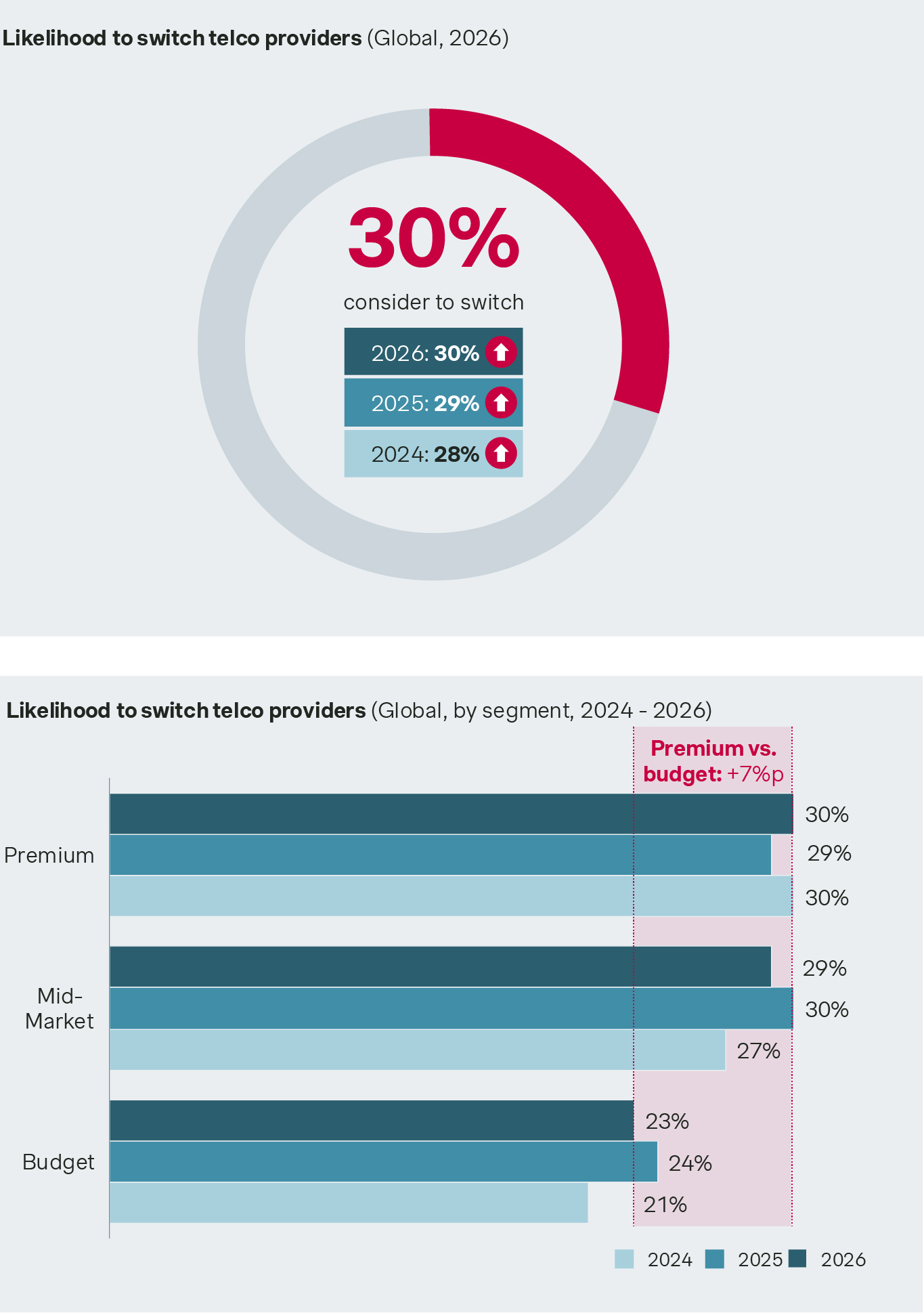

Customer loyalty is eroding, and the risk is concentrated where it hurts most. Approximately 30% of customers globally report they are actively considering switching their operator - up from 28% in 2024 and 29% in 2025.

The driver is "fear of missing out", increasingly triggered by aggressive budget offers. Customers who had no active intention to switch are being unsettled by the visibility of cheaper alternatives. They are leaving, or beginning to consider it, because the value equation no longer feels justified.

Switch intent is highest in the premium segment at 30%, precisely where ARPU concentration is greatest. Premium customers are the most valuable to lose as well as the most expensive to replace.

At 23%, budget customers are the least likely to switch, held primarily by price. But that is still nearly one in four customers open to leaving – many of whom joined for price and then found the trade-off unsatisfactory due to the quality gap. This creates a more nuanced customer inflow dynamic. Some customers are switching for price, others for unmet expectations – and only the latter represent a genuine inflow opportunity for tier 1 and 2 operators.

How MVNO growth is changing the customer inflow mix

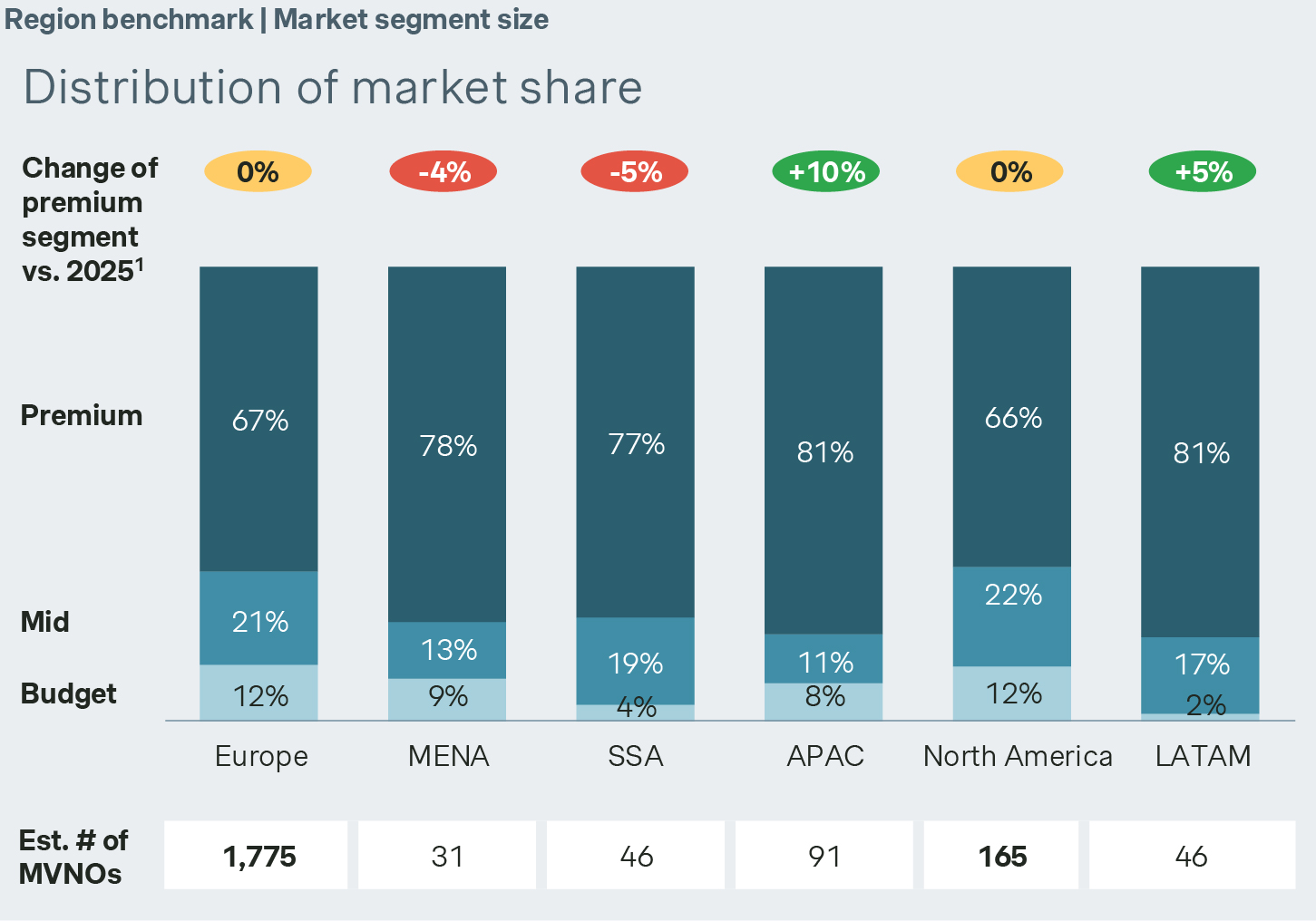

MVNO intensity is the most visible structural force putting direct pressure on the premium segment. The two regions with the deepest MVNO markets – Europe with 1,775 operators and North America with 165 – carry the lowest premium segment shares globally, at 67% and 66% respectively. APAC and Latin America, where MVNO ecosystems remain less developed, are still expanding their premium base, growing by +10% and +5% respectively since 2025.

Where MVNO presence is high, premium segments are smaller and the budget mix is larger. This is the direct consequence of what aggressive low-cost competition does to customer distribution over time.

For acquisition, this changes the mix of available customers. A larger share is now structurally more price-sensitive, regardless of how operators position themselves.

Price power is local but increasingly under pressure in many markets

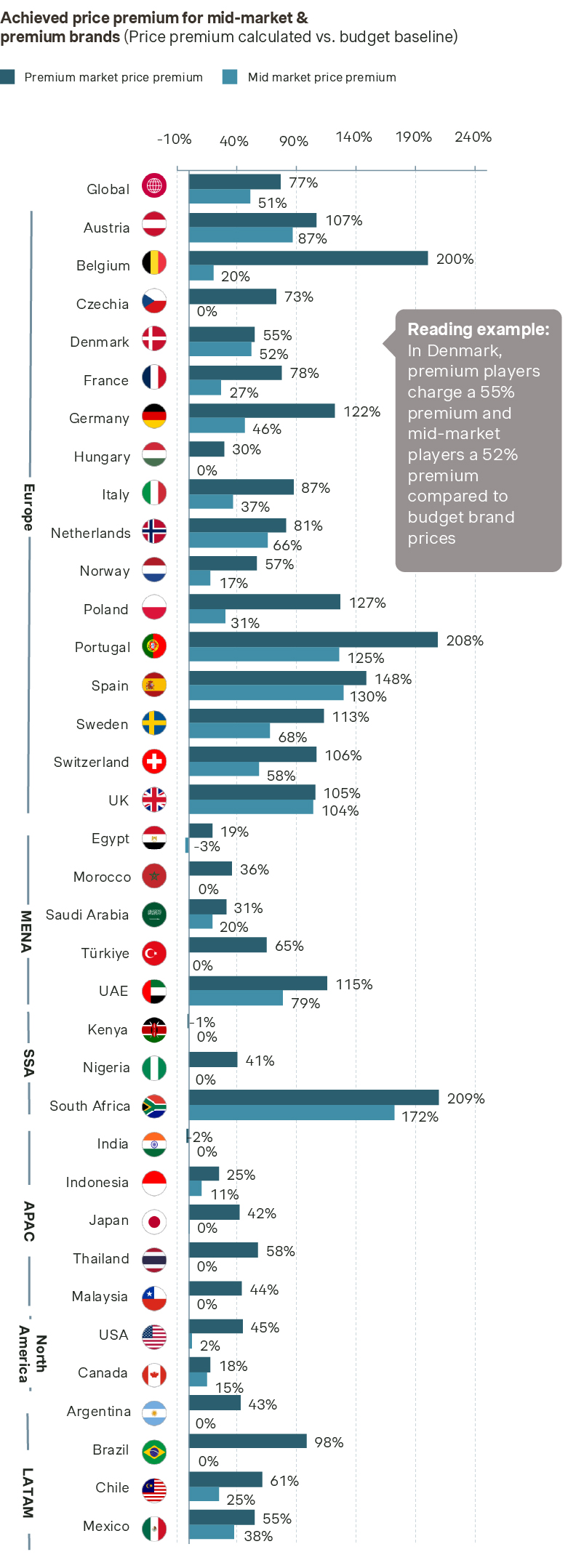

Price benchmarking across 35 markets makes the telco customer acquisition challenge more explicit. South Africa and Portugal have premium brands that command price premiums above 200% versus budget. Switzerland, Belgium, Spain, Germany, and the UK show premiums exceeding 100%. These are markets where premium positioning has historically translated into strong pricing power.

That advantage is now exactly what places them under pressure on the acquisition side. As budget competition intensifies, operators in high-premium markets face a difficult choice: defend the price point and risk losing inflow or adjust price and erode the margin that justified the premium positioning in the first place.

The pressure looks different where that advantage didn’t exist. In markets such as Brazil and India, mid-market premiums are effectively zero, indicating limited perceived differentiation between mid-market and budget offerings.

This shows willingness to pay is determined by market conditions. Across most markets, the price gap between premium and mid-market is narrow. Where that gap collapses, the biggest competitive threat comes from budget providers. When customers cannot perceive a clear step-up in value, they default to price. And in a market where MVNO competition is intensifying, that is a losing position no premium operator can defend on pricing alone.

Getting on the customer radar – with the right customers

The available customer pool is changing, and a growing share of it will cost more to acquire and retain.

Poor acquisition decisions show up in churn costs, in ARPU erosion, and in the retention spend required to hold a base that should never have been built that way.

In this environment, telco brand visibility must be accompanied by relevance. This is where inflow connects back to brand outlined in our first blog. Brand defines the space an operator can credibly occupy, whereas inflow determines whether that space is filled with the right customers.

Click here to read blog 1: brand

Click here to read blog 3: base

Click here to read blog 4: outflow

Interested in our 2026 Global Telecommunications Study results in more detail?

Form placeholder. This will only show within the editor