Negative interest rates were once considered an obscure curiosity. Consensus considered them to be – at best – a temporary phenomenon. Fast forward six years and it is clear that negative interest rates (NIR) are here to stay. What strategic options do private banks have to cushion the effects of NIR and how can the industry successfully monetize bank deposits without upsetting its clientele?

Negative interest rates – from curiosity to routine

Introduced in the aftermath of the financial crisis of the 2000s, NIR are still present today in the European financial market – most prominently in EUR and CHF. On Dec 14 2014, the headlines were reserved for the SNB. Its message "National Bank introduces negative interest rate" seemed simple and most observers considered NIR a temporary phenomenon at best. Very few would have expected them to still be present in 2021 – with no end in sight.

Banks need to adjust their offering and pricing structure in a smart way. This becomes even more urgent as pressure on earnings for banks is increasing, with shareholders and investors expecting to subject excess liquidity to a “penalty interest rate”.

However, banks that pass on NIR too drastically onto their clients will be caught in the crossfire of being branded unfair as well as damaging their reputation and losing clients and assets, since NIR remain an evergreen for the media.

Ultimately, NIR are increasingly becoming an expected and accepted reality for an ever-widening client scope. However, banks in general, and private banks especially, need to think about implementing and passing them on in a smart way.

Current situation and handling of NIR at Swiss private banks

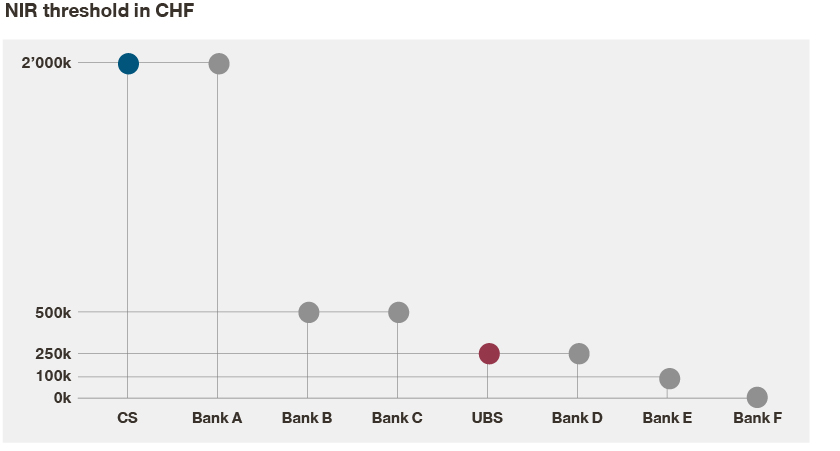

When talking about private banks, Switzerland immediately comes to mind. So how do Swiss private banks handle NIR? Here most wealth managers have quietly implemented NIR and made them a reality for their clients. When looking at the Swiss market, it becomes clear that the NIR cost passed on to clients does not deviate from the official SNB rate (75 bps) among Swiss private banks. However, the threshold for which clients have to pay NIR does vary considerably. At one private bank, clients are charged from the very first Swiss franc, whereas at the upper end only cash in excess of two million is charged. All of this before considering “individual agreements and special client setups”.

Overview of applicable NIR threshold among selected Swiss private/universal banks in CHF thousand

Ultimately, we expect private banks to continuously lower thresholds going forward while simultaneously increasing NIR enforcement for all mandates and clients (as some banks have decided to apply NIR for certain client segments only). Since the introduction of NIR in Switzerland in 2014, thresholds have continuously been lowered – most recently with UBS acting as the market leader, setting a new standard at 250k CHF.

The question remains: How can private banks use pricing solutions to effectively a) cushion and b) still pass on the effects of NIR to their clients in accordance with their strategy? We observe vast differences in how Swiss private banks go about implementing and enforcing NIR – while some manage to subject more than 70 percent of AuM to NIR, others struggle to subject approximately 10-20 percent of AuM to NIR.

Five proven pricing solutions to cushion and pass on effects of NIR

- Differentiate NIR charging based on mandates, product penetration, total revenue contribution, and RoA

Each segment to its own! Tailor your NIR regime around influencing factors such as mandates, product penetration, total revenue contribution, and RoA. Proactively provide transparency to clients about their “status” with you – the higher their product penetration and loyalty with you, the more discounts they can expect on NIR charges. - Implement relative NIR thresholds

Introduce relative thresholds for NIR charging which can also be used to incentivize client behavior (e.g. 10% of invested AuM can be cash which will not be charged). - Be flexible with thresholds & negative interest rates

Experience shows that passing on all NIR costs above threshold to clients is still not possible in some cases. Therefore, it might be worth considering “flexible” thresholds and/or “flexible” negative interest rates to provide the front with more room for maneuver. That way, the RM is able to still pass on some NIR costs to the client. - Offset paid NIR charges with transaction credits

Use paid negative interest rates to deepen your client relationship by offsetting transaction fees corresponding to paid negative interest fees – enabling clients to trade and invest their assets with you. - Pass on NIR costs to RMs

Reward good pricing – tying RM compensation predominantly to NNM is not in line with the bank’s strategy. Better to incentivize RMs to either pass on NIR onto their clients or to bear (some) of the associated costs for the banks themselves.

Ultimately, there is no one-size-fits-all solution. NIR measures need to be adapted and customized to the individual bank, its culture, and most importantly its client base.

Summary and takeaways

Banks, and especially private banks, need to find ways to cushion and use NIR to their advantage by deploying smart pricing solutions aimed at further connecting and deepening the relationship with their clients. To date, most focus on lowering the threshold and increase NIR enforcement in regular intervals. Instead, banks need to recognize the strategic options available to effectively use NIR to their advantage. In today’s environment with shrinking margins, the revenue potential offered by NIR needs to be addressed – either directly by increasing NIR revenue via stricter enforcement or by increasing invested assets. In addition, the topic of potential NIR charging can also be used to initiate client discussions about investing the cash which would also come along with higher revenues for the bank. Experience shows that invested clients are more loyal, significantly reducing the risk of churn.