Developers of disruptive medical technologies face a pioneer’s burden. They’re challenged with monetizing a unique product with no precedent to build upon. The medtech team of the market strategy consultancy Simon-Kucher & Partners shares its perspective on components of monetization strategies for companies offering paradigm-shifting products.

In most industries, the superlatives “breakthrough” and “disruptive” are sizzling marketing claims designed to incite customer interest in a product that is unlike any other; it does something that has never been done before or advances the state of the art in a dramatic way. But when it comes to medical devices and other products used in medicine, these terms induce almost as much fear—on the part of developers and their customers—as excitement.

First, there’s the very conservative nature of medicine, the fact that doctors are trained to adhere to standard practice for the safety of patients and their own careers and they have little time for training in new techniques and workflows.

There’s also the uncertainty around how to get paid for a novel medical innovation, given the complicated incentives and economic pressures across fragmented medical care. Adequate reimbursement is never a given at the outset, and in working towards that goal, it’s crucial for innovators to clearly articulate the value of the radically innovative technology in the language and interest of particular adopters.

There is some potential good news on the reimbursement front—the new Medicare Coverage of Innovative Technology (MCIT) ruling, currently expected to go into effect in December of this year. This could provide some tailwinds for disruptors by automatically granting four years of national coverage to technologies that have earned the FDA’s Breakthrough Technology designation, as long as they fit into a Medicare benefit category. This would help companies launch technologies into the market sooner, and thus collect data as they work to make their case with private reimbursement groups.

Finally, without any precedents, it can be difficult to establish pricing that both rewards companies for their development efforts but is realistic and sustainable.

These challenges are all part of what we call “the pioneer’s burden,” based on the launches of paradigm-shifting innovations we have supported over the past few decades. Most of the products in the medical device industry reflect incremental innovation, and therefore, most companies don’t have a depth of experience in launching disruptive technologies that fundamentally change the standard of care in a particular specialty, in a way that provides a significant clinical, economic, or workflow type of benefit to a patient or clinician.

There are particular challenges for the first and only company in a market. We have observed a number of success factors for commercial teams to look out for as they are preparing for launch. Below, we share some of our key learnings.

1. Reimbursement levels at launch do not reflect the value of innovation

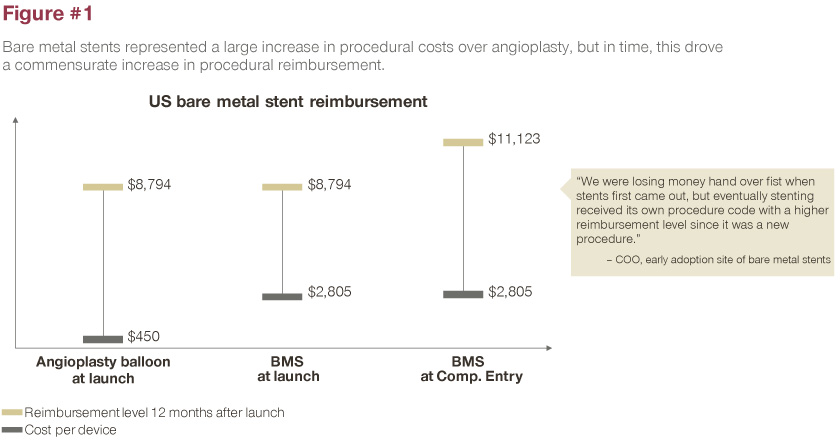

When companies launch innovative products, the funding that is available is not aligned with the value of that innovation. That’s because reimbursement is always backward-looking, taking into consideration what has been available in the past, especially given the length of time needed to establish contract agreements. Companies often start by looking at reimbursement, but that is a mistake, since existing reimbursement doesn’t reflect the value of your innovation or indicate what your pricing should be. When your product is paradigm-shifting, you have to create a new pathway whether through an avenue like NTAP (new technology add-on payment), new coding (for a procedure, product, or drug), or by having procedure reimbursement increase over time to reflect the value of your innovation.

The bare metal stent (BMS) is a case in point. A cardiologist places a stent during coronary angioplasty, also called percutaneous coronary intervention (PCI). When BMS first launched, stents cost about $2800 and were much more expensive than angioplasty, which was closer to $450. Over a 12-month period, new procedure codes were established, DRG (Diagnosis Related Group) payments were raised, and the rest is history, with the meteoric growth of those procedures and the category soon after launch.

With a platform of prescription digital therapeutics, Pear Therapeutics Inc. is another great example. Pear is redefining medicine, with FDA-cleared software offered by prescription only. The company’s first product reSET-O treats opioid use disorder through smartphone-based intervention. Many other apps claim to provide some sort of health benefit, but Pear is in a different category, not only from a regulatory standpoint, but from a clinical viewpoint, meaning that the physician is the gatekeeper for that therapy and determines when it should and should not be used.

No precedent for broad reimbursement exists within this category. The company currently has established agreements with some smaller payors, including the Hartford Financial Services Group and Serve You Rx, to offer reSET and reSET-O (for opioid overuse disorder) within their standard formulary.

Many firms developing digital therapeutics might look to formularies being established by pharmacy benefit managers (CVS Caremark, Express Scripts, and the like) but not all market access is good access. We see that specifically in the digital therapeutics space, where many companies are attempting to gain traction by any means possible, say, a pilot program where they’re not being paid for their product, or a digital formulary that may have little, if any pull-through. Adoption of both pathways is optional—they aren’t automatically included in a customer’s formulary benefit—so that won’t drive pull-through utilization if customers don’t opt into them.

As one of the only companies with a prescription digital therapeutic, it hasn’t been easy. It has taken Pear a significant period of time to establish a new class of product and a new way of getting paid, but we have seen, from a market access standpoint some leading indicators of success as a few PBMs, payors and self-insured plans have started to cover the technology.

Meanwhile, Pear has confronted the challenge of being first by being open to different ways of getting paid. With the launch of Somryst for the treatment of chronic insomnia, they have taken a more direct-to-consumer approach, in parallel with a more payor-focused one. The company publicly details the ability to go online and use telemedicine to get a prescription for their digital therapeutic, while paying cash.

2. How you charge is more important than what you charge

Across industries, we have consistently seen that there is a significant difference in the level of adoption for a new innovation based on the price model utilized. There is an opportunity to differentiate price models on both the frequency of payment (e.g., monthly vs. annual) as well as the metric (e.g., per procedure vs one-time payment).

Abbott Laboratories Inc. has adopted the latter strategy for its MitraClip structural heart business.

Available in the US since 2013 (and in 75 other countries), MitraClip is the world’s first transcatheter mitral valve repair therapy, for patients with primary and secondary mitral regurgitation. It is the only transcatheter edge-to-edge repair (TEER) device approved by the FDA to date. The TEER procedure is now recommended in ACC/AHA guidelines.

Rather than charging for each device, Abbott took on the risk of offering a per-procedure price, for a procedure in which one to three clips (rarely, more than three) are used to accomplish the mitral valve repair. As one can imagine, on a per-clip basis, the cost to the provider would be variable and unpredictable. But Abbott’s stance is to treat the patient, and to allow clinicians to do the right thing, since they don’t have to consider economics when considering an additional clip. That’s markedly different from what has occurred in the drug-eluting stent sector, where a clinician might use one, or as many as five stents in a procedure, where each stent costs, say $1,000 (depending on the stent).

3. Strong price hygiene and clear governance is required for scalable growth

Healthtech companies are often too sales driven, which can get them into issues from a pricing perspective if deal volume is prioritized over price integrity/hygiene. We have seen many scenarios where the CEO is required to step in when procurement teams unwind deals and point out inconsistencies that the sales team cannot justify or explain when they have been engaging in opportunistic behavior. Over time, buyers negotiate with multiple vendors and this can eventually lead to an exit from the market due to eroded prices. Indeed, Johnson & Johnson, which created the stent category within its Cordis business, eventually left the business entirely because of price erosion. Companies need to focus on good price hygiene, i.e., the price can’t vary from one customer to another.

Abbott has also been innovative in offering price transparency within markets, that is, it offers a flat price for all markets within the US, and within Europe, for example. This is unusual in the world of medical devices, where negotiated deals result in one hospital paying a certain amount, and another paying a different amount for the same medical device.

4. Sell on value by looking beyond a narrow view of procedure economics to highlight upstream and/or downstream benefit

Procedure economics and the idea of the customer’s profitability are obvious topics around which to build arguments for adoption of a ground-breaking technology. But since, at the time of launch, reimbursement might not be commensurate with the value of the technology, it can be important for paradigm-shifting innovators to look beyond cost versus reimbursement when they tell their value story.

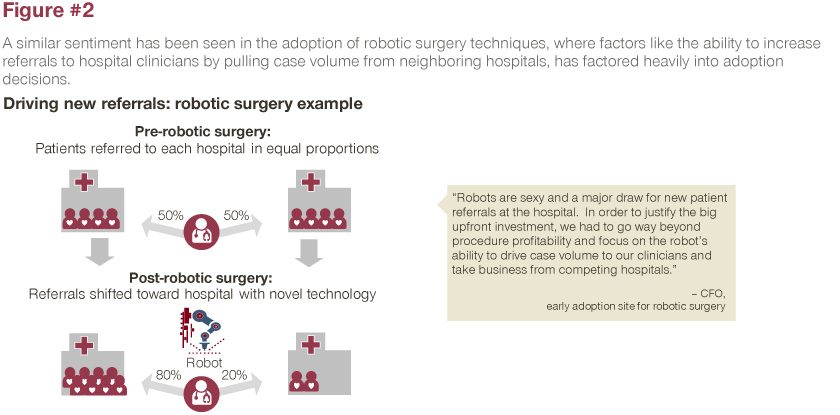

One thing to think about is referrals for clinicians. Do they now offer a procedure for patients that no one else can treat? The potential to pull case volume from other clinicians or hospitals carries significant weight in the purchasing decision-making process. New technologies might lose money initially, but if they can generate enough procedures to offset lost profit, they can claim "loss leader" status.

For example, key-hole CABG [coronary artery bypass graft] surgery unlocked a huge swathe of patients that were too sick or too frail to have a procedure. When minimally invasive CABG first came out, it wasn’t fully profitable at current levels of reimbursement, but it did lead to a referral effect where a facility could now treat patients they couldn’t treat before because of the severity of their disease or their potential complication rates.

That might cause people to seek out that facility, either through referral or by self-referring and even paying cash to get their surgery done there. And these referrals could have a halo effect, increasing not only these specific procedures, but procedures in adjacent areas. Making this case to potential customers is important if the initial reimbursement scenario doesn’t make a great economic case for the product. The halo effect might amplify profitability by bringing more procedures to your facility. Other examples of minimally invasive surgeries that expand the treatment population include transcatheter aortic valve repair and robotic surgeries.

5. Accept Market Share Loss as Competitive Entrants Inevitably Come In, and Do Not Erode Your Value

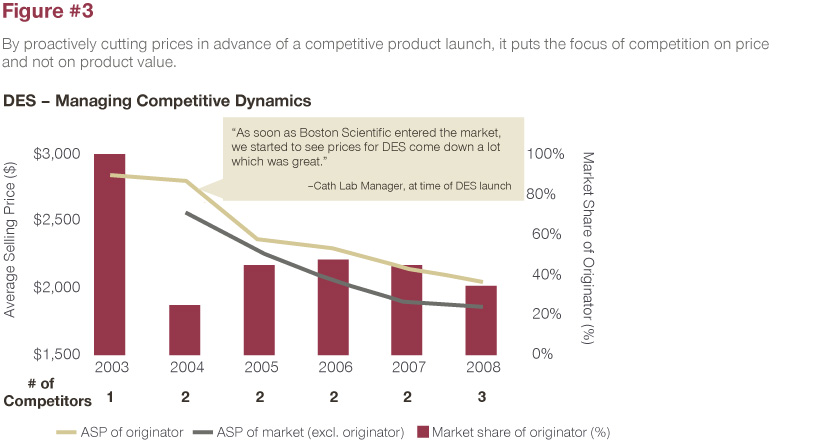

As new competitors enter the field, it should be expected that some level of market share will be lost. However, don’t proactively cut prices before the launch of a competitive product, as it puts the focus of the competition on price rather than product value. We see companies continue to fight for every point of market share to the detriment of the business. If you are in orthopedics, for example, you are never going to own 100% of the business. It is not realistic or possible to hold onto market share. To justify the innovation’s price premium over time, the innovator must continuously develop clinical evidence and a competitive product pipeline.

A prime example of this is in the highly competitive area of drug-eluting stents (DES). DES commanded high prices near $3,000 (ASP) before competitors began to enter the market. Once Boston Scientific Corp. launched its solution in 2004, the DES originator responded with sharp price decreases to combat competitive entry. This placed the focus of competition on price and not on product value, which ultimately eroded the price of the DES market below $2,000 (ASP) within five years. This market continues to see high levels of price erosion to this day.

6. Be Careful How You Treat Customers

As a pioneer in a new space, some degree of monopolistic resentment cannot be avoided, no matter what price level is pursued. It’s important to consider customer perception of the “extremely expensive” price level to minimize backlash upon market entry. In order to further justify a high price, ensure all other key factors are right, including support services, supply chain, inventory policy, and price flexibility.

Although the first company in a new market is “the only game in town,” it behooves the innovator to be careful about how they treat their customers. If you are disciplined about your pricing, about providing extra levels of service, about not being arrogant when you approach companies in sales discussions that will go a long way to generating good will when the next generation product comes out, so you don’t lose market share in a competitive market.

This article was originally published in June 2021 issue of MedTech Strategist and also posted on MyStrategist.com on June 24, 2021. Senior MedTech Strategist writer Mary Stuart contributed to this article.