E-Mobility and electric vehicles (EV) are hot topics right now. In this series, you learn more about up-to-date market developments, exciting news, and the resulting implications for your business. This time, we’re focusing on the insightful results of a recent Simon-Kucher study.

When will electric vehicles conquer the mass market? Which consumers’ preferences have to be met regarding features and capabilities in order for that to happen? How will this affect the automotive market? And how will charging infrastructure develop? To learn more about the opinions and requirements from the consumer side, Simon-Kucher conducted a representative study among BEV owners and considerers in May 2021. Within, we surveyed EV drivers, people envisaging buying an electric vehicle during the next one to two years (we call them early adopters), and people thinking about buying an EV in two to three years (the early majority).

From niche to mass market: customer expectations of e-mobility

The insights from this study are more relevant than ever, since 2020 was the year in which e-mobility finally entered the phase of exponential growth. Given the CO2 targets of major OEMs, we expect electric vehicles to account for 20 to 25 percent of the total fleet by 2030. Will there be a certain type of electric car that leads this development? A clear picture emerges among our study participants: a quarter prefer a compact car, a fifth an SUV. Therefore, many current models are already in customers' sweet spots. As range increases, EV use becomes more similar to internal combustion vehicles. In our survey, kilometers driven per day with the former were only 15 percent lower than with the latter. However, to be attractive to the early majority, ranges still need to increase by roughly 40 percent to a range between 500 and 600 kilometers. We are expecting this to become reality between 2022 and 2025.

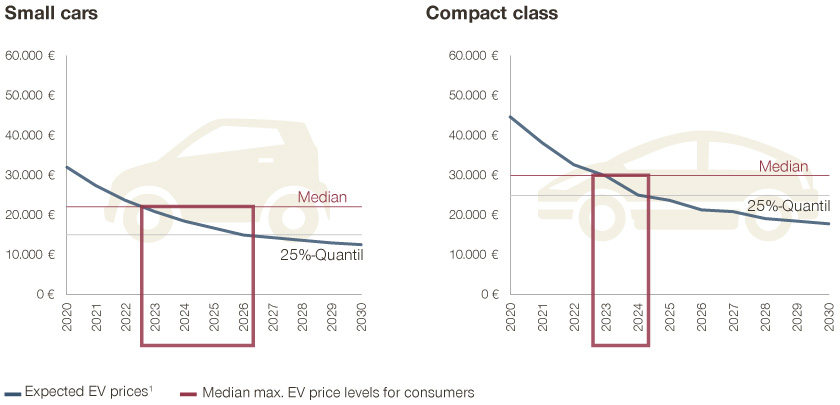

Looking at the technological development, customers’ preferences plus their willingness to pay and combing these insights with the expected cost development of EV, electric cars will become attractive to the masses very soon! In the small car segment, price points of 15,000 to 22,000 Euros achieve broad appeal, this will be within reach in 2023 to 2026 (even without subsidies). In the compact class segment, price points of 25,000 to 30,000 Euros meet customer expectations, and the market will be able to offer exactly this even earlier, in 2023 to 2024. Therefore, the shift from internal combustion to EV is accelerating and will come sooner than expected. OEMs could reduce leasing offers for internal combustion vehicles in the near future.

Requirements of e-mobility for future automotive sales

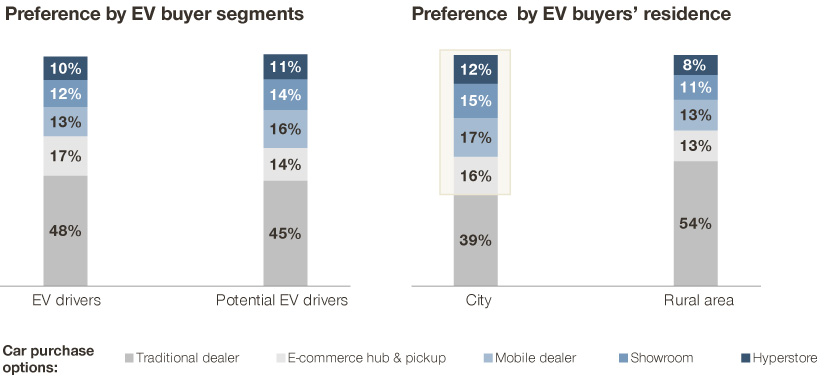

Does this increasing popularity of electric cars change the way cars in general are being sold? To a degree: Traditional dealers will remain relevant in the future – but interest in new buying experiences is growing, especially in urban environments. Combining their purchase of an EV with the addition of a charging contract is attractive for many buyers, especially among consumers who prefer an integrated online customer journey. OEMs therefore need to complement existing dealer structures with new buying experiences, digital distribution models, and collaborative product offerings.

New charging options as e-mobility drivers

With more and more electric vehicles in urban environments (where single-family homes with electricity outlets in garages are the exception rather than the rule), home charging will become less relevant in the coming years. Up to 60 percent of charging operations will happen in public, for example at work, at filling stations, and shopping centers.

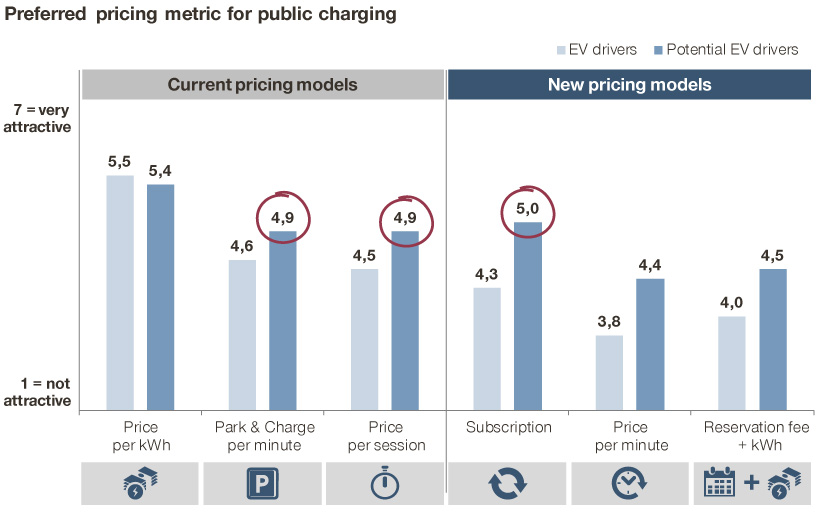

This creates exciting opportunities for charging point operators: Since the next generation of EV drivers is still interested in contract-based pricing models for public charging (as opposed to pay as you use price models), they don’t have to undertake a paradigm shift compared to the “classic” refueling process without prior registration. Together with e-mobility software migration, this allows service providers to offer differentiated pricing models the same way as before. At the same time, more and more options for new, innovative pricing models beyond per kWh billing are emerging. Charging per minute or per charging session or even offering subscriptions are increasingly attractive for many prospective EV drivers. They are also open to station-based price differentiation and dynamic pricing for public charging.

However, with these opportunities for new pricing models, there are also risks involved: On the one hand, consumers’ willingness to pay for public high power charging (HPC) is lower among the next generation of EV drivers than it is currently. Plus, new, government-subsidized competitors are entering the HPC market. And what’s more, future payment systems might make hardware upgrades necessary and additional costs for retrofitting are to be expected. These factors combined will put pressure on the market price as well as charging operators’ business models. A successful pricing model therefore participates in these price increases today and hedges against future price pressure.

Conclusion: The e-mobility revolution is almost there

As you can see, a large portion of drivers using electric cars is no longer a vision of the distant future. In just two to five years, customers’ requirements, their willingness to pay and prices for EV will match up. Hand in hand with this development, charging infrastructure and even automotive sales will need to adapt. By adopting innovative price models and expanding into online sales channels, companies in both areas can prepare for this future.