In recent years, pharmaceutical funding trends in Spain have evolved due to increasing budget impact concerns aggravated by COVID-19. Experts Ana Mozetic, Laura Sánchez-Calero, Iván Bouza, and Elena Aldareguia analyzed funding decisions made by the Ministry of Health between 2019 and 2021 to help manufacturers understand what to expect.

In recent years, the budgetary impact caused by pharmaceutical expenditure has led to an evolution of trends in the funding of drugs in Spain.

This P&R brief focuses on the funding resolutions made at the national level for both innovative drugs accessing the market and available drugs extending their therapeutic indication. It analyzes the conditions granted together with the positive funding resolution (e.g., access restrictions, cost-containment measures, managed entry agreements in place).

Current trends

Decreasing positive funding decisions and extended times to reach a price agreement

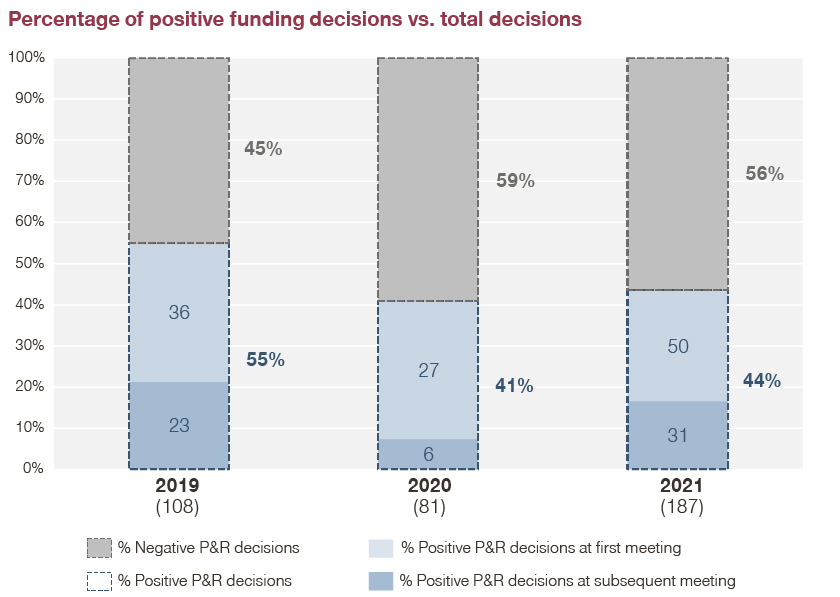

Of the total number of funding resolutions made between January 2019 and December 2021 (376), only 46 percent (174) received positive funding resolutions, while 54 percent (202) were rejected.

Within the analyzed period, the percentage of positive resolutions slightly decreased and fewer positive decisions were made in the first Drug Pricing Committee (CIPM) review of the specific request (funding of a new drug/new indication).

This means that we see a slight increase in the number of decisions taking place at subsequent reviews of the funding request by the CIPM. In this regard, the number of positive decisions at the first CIPM meeting went down from 66 percent in 2019 to 57 percent in 2021.

Recurring use of cost-containment measures:

Among the positive decisions published during the last three years, 76 percent entailed some type of budget impact control measure: Monthly/annual sales monitoring with potential risk of negotiated price review or restriction on funding beyond the indication approved by the European Medicines Agency (e.g., to specific subpopulations, by treatment line).

Preference for financial vs. outcome-based agreements:

Between January 2019 and December 2021, several positive funding resolutions were accompanied by managed entry agreements, 25 percent (15) of the total positive decisions in 2019, 6 percent (2) in 2020 and 21 percent (17) in 2022.

1. Financial agreements

Over the last three years, the following types of financial agreements have been negotiated between the Ministry of Health and pharmaceutical companies:

- Maximum cost per patient: 6 percent (11) of the funding decisions entailed this type of agreement, which is usually preferred if dose requirements are unclear or when there is uncertainty around clinical outcomes and treatment duration

- Sales cap: Even if only 5 percent (9) of the funding decisions established an annual sales cap, its use has slightly increased in 2021 (6) compared to 2019 (3)

- Price-volume agreements (PVA): They only account for 1 percent (2) of the total decisions made over the last three years and they all correspond to 2021

2. Outcome-based agreements

All outcome-based agreements put in place during this period were articulated as payment by results. These aim to mitigate uncertainties around drugs’ clinical outcomes and to ensure that only patients benefiting from the treatment imply a cost for the system:

- Payment by results: 8 percent (14) of the funding decisions led to this type of agreement, but its use is being reduced over time apparently due to the administrative burden these entail

In addition, out of the total (174) positive funding decisions, 14 new drugs (8 percent) and three new indications (3 percent) were included in Valtermed – a system to determine and monitor the added therapeutic value of new drugs in real clinical practice, through a predefined, specific, pharmaco-clinical protocol for each product. Many of the included products are subjected to payment by results schemes, which allows the Ministry of Health to link the funding of these drugs to their real-world performance.

However, there are also several drugs included in Valtermed with other types of managed entry agreements (MEAs) or even none, with the sole objective of ensuring an appropriate clinical use of drugs by tracking real-world evidence that further supports reimbursement and access conditions granted.

Lastly, less than a handful of positive decisions were accompanied by an agreement related to free / lower price doses.

So, where are the funding decisions heading to?

The increasing pharmaceutical budget impact is one of the Spanish Ministry of Health’s main concerns, and several measures have been put in place with the aim to manage and control it.

Most recently, published decisions made by the Drug Pricing Committee reflect a decreasing number of negotiations resulting in a positive funding resolution. In addition, for those who achieve it, the process typically involves a higher number of negotiation rounds with the Ministry of Health.

Moreover, cost-containment measures have been included in almost every favorable funding resolution, and, in many cases, managed entry agreements are still a needed negotiation tool to ensure the drug reaches the market. The choice between the different MEA options is driven by two key factors: The type of uncertainty (e.g., clinical, budgetary) generated by the drug and the expected agreement implementation requirements.

Therefore, although new drugs manage to achieve public funding, the process is becoming increasingly long and complex. This is delaying access to market for drugs that are already available in other European countries.

What actions can manufacturers take to influence a positive outcome in negotiations?

However, there are still some proactive actions that can positively impact the negotiation outcome:

- Plan an early engagement with key stakeholders and physician advocacy groups to develop a robust product value proposition

- Prepare a solid negotiation strategy with clear objectives and expected outcomes, and train the relevant teams accordingly

- Ensure the Price and Reimbursement Dossier is in line with the defined negotiation strategy and that it clearly conveys the value of the product in the targeted population

- Model in advance and be prepared to suggest solutions that mitigate uncertainties around clinical outcomes and budget impacts (e.g., financial or outcome-based solutions)

Taking a sneak peek into 2022 funding decisions to date, it looks like these trends are here to stay. Stay tuned for future updates on funding negotiations trends in Spain!