In November 2022, the new GKV Financial Stabilization Act (GKV-FinStG) came into effect after being passed by the German parliament. The objective of the law is to financially stabilize German statutory health insurance policies (GKV). To achieve this objective, far-reaching changes in the legal framework for pricing and reimbursement of innovative pharmaceuticals have been adopted.

Our industry experts Gabor Kiss, Christoph Engelke, and Alexandra Gottswinter have investigated the legislative changes and analyzed the implications of the GKV-FinStG for pricing and reimbursement of innovative drugs in Germany. In this report, they provide an overview of the most important changes to the AMNOG process and discuss remaining uncertainties. Furthermore, they provide an overview of strategic implications that may arise for pharmaceutical companies when planning and managing pricing and reimbursement.

New federal government: Tackling what has been discussed for years

For many years, there have been ongoing discussions at the policy level about how best to manage and reduce drug spending during times of increasing cost pressure in various advanced healthcare markets across the globe. Germany has been no exception to these discussions: There have been consistent payer demands for regulatory changes, emphasizing the need to lower the budget impact of high-cost drugs.

Consequently, the new social democratic-led government in Germany, formed in December 2021, has announced its objective to reduce expenditure on pharmaceuticals. This has been a high priority for the Federal Ministry of Health, driven by the significant budget pressure within the statutory health insurance system, and intensified by the COVID-19 pandemic. Therefore, the Federal Ministry of Health has developed a concrete plan to reduce pharmaceutical expenditure through the GKV Financial Stabilization Act (GKV-FinStG), which recently passed the legislature and came into effect in November 2022.

An overview of the most important changes

In mid-2022, several draft papers describing potential legislative changes were intensively discussed by political stakeholders. Those changes made it through the legislative process in November 2022, and there is now more clarity on the concrete actions that will be taken to stabilize healthcare and drug spending in Germany.

Seven key legal changes stood out – however, it is still uncertain how some of these changes will be implemented in practice:

Description in detail:

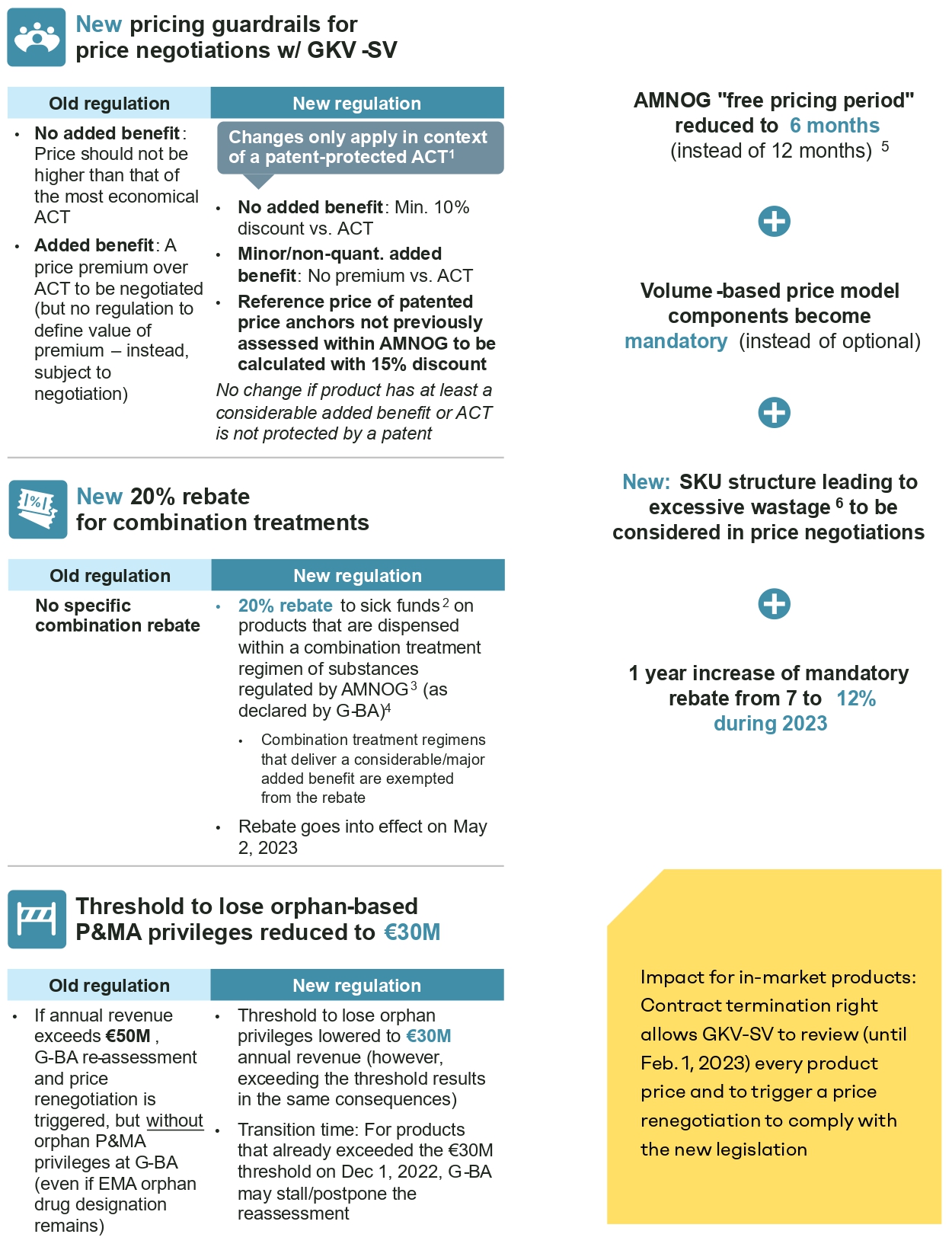

- AMNOG free pricing period reduced from 12 to six months: Since the introduction of AMNOG in 2011, manufacturers have been free to set the reimbursed launch price for 12 months while the benefit assessment and price negotiations (for a price valid as of month 13) are conducted. Based on the new law, the free pricing period is shortened to six months, i.e., the new reimbursement price will be valid as of month 7 retrospectively.

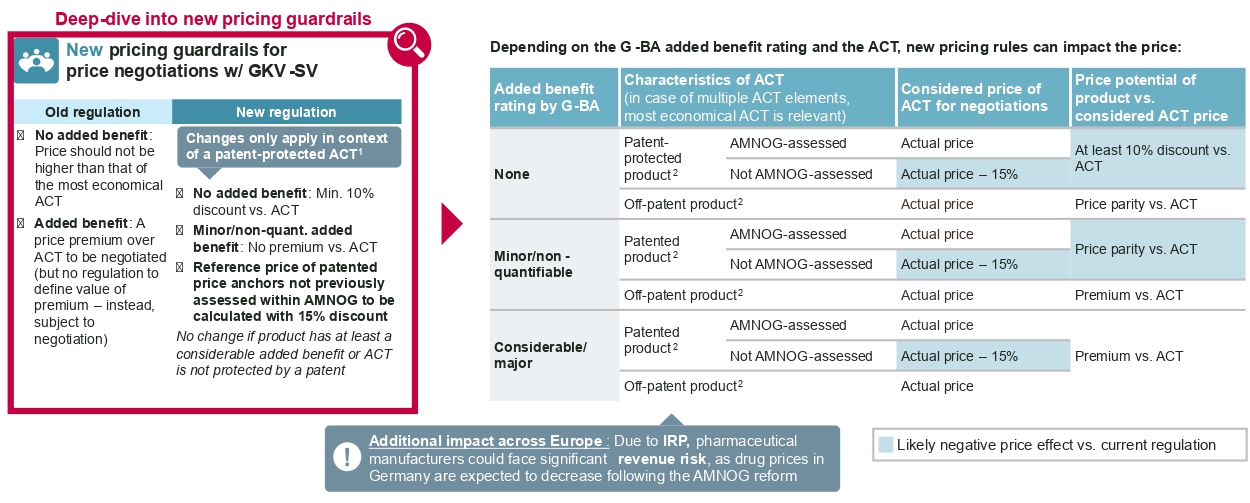

It should be noted that the new negotiated reimbursement price will be published when negotiations are completed typically about one year after launch, according to standard negotiation timelines. Pharma companies will therefore need to pay back some of the revenue earned after the sixth month to individual sick funds, namely the difference between the freely set launch price and the negotiated reimbursement price for every unit reimbursed by sick funds as of month 7 after launch. - Implications of the G-BA added benefit assessment for price negotiations: Historically, the added benefit appraisal by the G-BA translates to a simple and distinct implication for price negotiations with the National Association of Statutory Health Insurance Funds (GKV-SV): If the drug was granted an added benefit, an adequate price premium compared to the appropriate comparator therapy (ACT) should be negotiated. If the G-BA concluded that there is no proven added benefit, the annual therapy cost of the new drug should not exceed the annual therapy cost of the most economical ACT. Under the new law, the reimbursement price is still driven by the level of added benefit, but it is now subject to significantly stricter pricing guardrails in case the most economical ACT is still under patent protection: In this event, the price of drugs without an added benefit should reflect a discount of at least 10 percent compared to the ACT. For drugs that have been granted a nonquantifiable or minor added benefit, the price should not exceed the costs of the ACT. The latter rule is a critical intervention into the AMNOG principles, as an added benefit has historically led to a price premium compared to the ACT. The less restrictive pricing guardrails previously applied to all products now only apply to drugs that were granted either a considerable or major added benefit, or if the most economical ACT is not under patent protection.

An additional new guardrail is applied when referencing price benchmarks that are under patent protection but have not been subject to a price negotiation within AMNOG previously: These price benchmarks in the future need to be referenced in negotiations not based on their actual price, but with a theoretical discount of 15 percent.

- A special rebate for combination treatments introduced: The new law introduces an additional 20-percent rebate for drugs that are used as a combination regimen and that fulfill certain criteria: It will only be applied to combinations with active substances that are categorized as “new substances” (i.e., first launched after 2011) and have explicit market authorization for combination use. Combination treatments that are granted a considerable or major added benefit are exempted from the rebate. The classification of which combination treatments are eligible for this rebate will be defined by the G-BA moving forward. The rebate itself will be operationalized as a payback requested by sick funds based on actual combination use in clinical practice. However, concrete guidelines for the operationalization of the rebate are still under development.

- Inclusion of volume or budget mechanisms in price negotiation and reimbursement contracts made mandatory: Historically, manufacturers and the GKV-SV were able to optionally include volume or budget components in their price and reimbursement agreements. It was common practice to only align on future sales volume projections in reimbursement contracts and to grant a special right of contract termination and renegotiation for the GKV-SV if actual sales volumes exceeded the projections. Typically, there has been no limitation of the reimbursable sales volumes. Moving forward, the new law defines volume or budget agreements (such as a price-volume agreement or budget cap) as mandatory. However, there is still debate around what is considered an appropriate volume or budget agreement mechanism.

- Annual revenue threshold to maintain orphan privileges reduced from EUR 50m to 30m: The German orphan drug status generates significant privileges for the G-BA benefit assessment procedure, most importantly by guaranteeing an added benefit rating. For many orphan drugs, this leads to a significantly more favorable starting position in price negotiations with GKV-SV. However, if an orphan drug has passed a certain annual revenue threshold, the manufacturer is obligated to undergo a reassessment of the added benefit rating and subsequent price renegotiation without any orphan drug privileges. Orphan drugs that fail to show evidence that they fulfill the formal requirements of the G-BA will lose their added benefit rating and will often be subject to significant price cuts in the subsequent price renegotiation. Historically, the respective annual revenue threshold to lose orphan drug privileges has been set at 50m euro (as per previous/rolling 12 calendar months based on pharmacy selling prices without VAT). After initially considering reducing the revenue threshold to EUR 20m, the final law reduces the revenue threshold to EUR 30m. This shift is highly likely to force many orphan drugs into reassessment and price renegotiation.

- Penalty mechanism introduced to price negotiations for pharmaceuticals with excessive wastage due to unfavorable package sizing: Currently, both the G-BA and GKV-SV base their annual therapy cost calculation on the average patient (as defined by the Federal Office of Statistics). Potential wastage that occurs as a result of suboptimal package sizing for the average patient (e.g., due to bodyweight-specific dosing) is already factored into this approach. However, the current estimation does not consideer potential wastage that occurs for patient groups outside of the defined “average patient.” The new law establishes an additional mechanism in the price negotiations, which is supposed to factor in excessive wastage of more than 20 percent for certain patient groups. The concrete mechanism of operationalization has not been specified yet.

- Mandatory rebate increased: The new law includes a temporary increase of the mandatory manufacturer rebate from 7 percent to 12 percent (gross) valid until December 31, 2023.

In order to implement the new pricing mechanism imposed by the law for products already on the market through price renegotiations, the GKV-SV has been granted a special (but optional) right to terminate current contracts and issue price renegotiations until February 1, 2023.

What the GKV-FinStG means for the pharmaceutical industry

The new law entails far-reaching changes in the pricing and reimbursement landscape for innovative pharmaceuticals in Germany. Pharmaceutical companies must deal with the long-term consequences of these reforms in the German pricing and reimbursement landscape – both on a national and an international level.

At the national level, the new pricing guardrails that depend on the added benefit rating can severely impact the price potential in national price negotiations. Drugs with a nonquantifiable or minor added benefit to the G-BA must be closely monitored to determine whether the ACT is protected by a patent at the time of the (re-)negotiation, as a patent can imply a significantly stricter and more challenging price negotiation environment. Drugs with prices determined through patent-protected price benchmarks that did not undergo a price negotiation within AMNOG can also be negatively impacted. Moreover, orphan drugs currently achieving annual revenue between EUR 30m and 50m or that are close to exceeding the EUR 30m threshold may need to strategically recalibrate. They may need to prepare for a new added benefit assessment and subsequent price renegotiations, or – if the EUR 30m threshold is not exceeded yet – assess potential strategies to prevent or optimize such reassessments. Overall, manufacturers need to closely assess their entire portfolio of both in-market and pipeline assets to identify risks and strategic implications for their pricing and reimbursement strategy of every asset. For products on the market, the special contract termination right is valid until February 1, 2023, which implies a significant risk for a potential short-term price renegotiation that requires thorough preparation.

For some products, the new legislation may even lead to a situation where the German price is at risk of dropping significantly below the international price corridor. Thus, it is critical to engage in scenario and financial planning even at the international level. Due to international reference pricing, a reduction of the visible price in Germany can have far-reaching effects on the global price.

Despite the numerous ways that the new legislation will negatively impact drug pricing, there are still uncertainties around the exact operationalization of several cost-saving measures. To highlight a few examples:

- How will a price-volume mechanism be designed? Will it impact the prospective visible price, or impose confidential paybacks? What will be the quantitative impact on revenues?

- How should the pricing guardrails be applied to products that compare against a patient-individual therapy or a combination regimen comprising patent-protected and non-patent-protected drugs?

- How will excessive wastage be considered in negotiation practice?

These questions and many more will be debated in future price negotiations. The analysis of the first products undergoing a price (re-)negotiation and – more importantly – publications of arbitration rulings under the new law will hopefully gradually resolve these ambiguities.