A bank's role as an intermediary between savers who prefer liquid deposits and borrowers who prefer illiquid assets, means they have fragile capital structures. How should US bankers respond to the SVB banking turmoil in the short, medium, and long term?

As we all know by now, the US government has stepped in and taken possession of Silicon Valley Bank (SVB), a state-chartered commercial bank serving tech, life sciences, venture capital and start-up businesses in California. The bank’s failure is the largest since 2008 when Washington Mutual bank customers withdrew $16.7 billion (about 9% of deposits held) during a nine-day bank run. That was before Twitter, same-day fund transfers, and social media trolls.

In the case of SVB, customers initiated $42 billion in withdrawals in just a single day, leaving the bank with a negative cash balance of $1 billion at the close of business on March 9. The day before the bank run, SVB alarmed investors and customers when it abruptly announced in a press release it was trying to raise capital, and had earlier sold securities which resulted in a $1.8 billion loss. According to California bank regulators, SVB had been in sound financial condition prior to the bank run.

Bank failures are highly uncommon in the modern day United States. However, the stunning collapse of the regional bank, and subsequent turmoil in the banking sector have spooked both bank customers and bank leaders.

The following are some lessons and recommendations on how banks can respond in the short, medium, and longer term.

Understand your deposit base and how they behave under stress

In the short term, banks must focus on their customers. In a recent survey, Simon-Kucher found an overwhelming number (59%) of retail bank customers identifying themselves as feeling negative about the economic environment, and sharing that they are fearful, angry, and dissatisfied. High inflation, a slowing economy, rising interest rates, and massive tech layoffs are unsettling American businesses and consumers.

Banks must recognize this and redouble efforts to shore up customer confidence and trust. In turbulent and uncertain times, customers already nervous and anxious, are highly susceptible to rumors of financial disasters.

Bank client communications must be clear, consistent, and transparent. Product and pricing changes in response to rising costs or inflationary pressure, must be communicated in a strategic, orderly, and empathetic fashion to reassure and retain depositors.

Anticipate fund movements through data analytics and modeling

Banks who are not doing so must start to employ data, analytics, and modeling tools to acquire a deeper understanding of their deposit customers. Deposit portfolio managers should have segment-specific intelligence on fund movements, behavior patterns, product usage, credit and debit patterns, and more. A comprehensive flow-of-funds model that tracks fund movements internally in the banking organization between various deposit, lending, and investment accounts, as well as externally involving accounts held outside the institution, can be a critical, strategic tool.

By mapping money movement trends, a bank can acquire a 360-degree view of their small business and retail customers. Over time the bank can anticipate deposit trends, withdrawals, and inflows with greater precision. These observations can help banks ensure investment maturities on the asset side of the balance sheet are in alignment with the deposit portfolio's liabilities.

As interest rates rise, customers are naturally going to move money in search of higher yield. A data-driven approach to map money movements in the deposit portfolio can serve as an early alert system to help the bank detect rising deposit pricing sensitivities and an increase in fund movements.

Orchestrate segment-specific communications

In the medium term, banks should leverage audience segmentation to identify groups based on psychographics, demographics, and behavior dimensions. Combined with data-driven insights derived from fund movements, banks can tailor communications, retention and acquisition efforts for greater impact.

For example, informed by insights on a segment's concerns and motivations, a bank's communications can be personalized to reinforce confidence in the organization's financial strength, resilience, and stability. Similarly, informed by flow-of-funds movements it might be appropriate to tailor communications to focus on the value of the banking relationship to retain a high-value deposit client.

Build a healthy deposit franchise

While the focus in the short and medium term should be on the customer, in the long-term banks must build and maintain a healthy deposit franchise.

This includes managing the bank's duration gap to ensure the timings of deposit outflows and asset inflow are well matched. The efficient use of investment assets is important to help banks avoid a maturity mismatch. So is having a systematic, disciplined approach to managing their deposit portfolios. Some types of deposits carry higher risk than others, and that should be taken into consideration when it comes to acquisition and retention efforts. Banks must also be able to identify the factors influencing and driving deposit fund movements at any given time including changing pricing sensitivities, the inflow-outflow patterns of start-up business clients, the competitive marketplace, and more.

A high performing deposit franchise generates deposits cost effectively, matches deposit portfolio construction to funding needs, and achieves deposit stability. In Simon-Kucher’s global experience working with banks under a wide range of market and competitive conditions, successful long term deposit franchises depend on four capabilities working together:

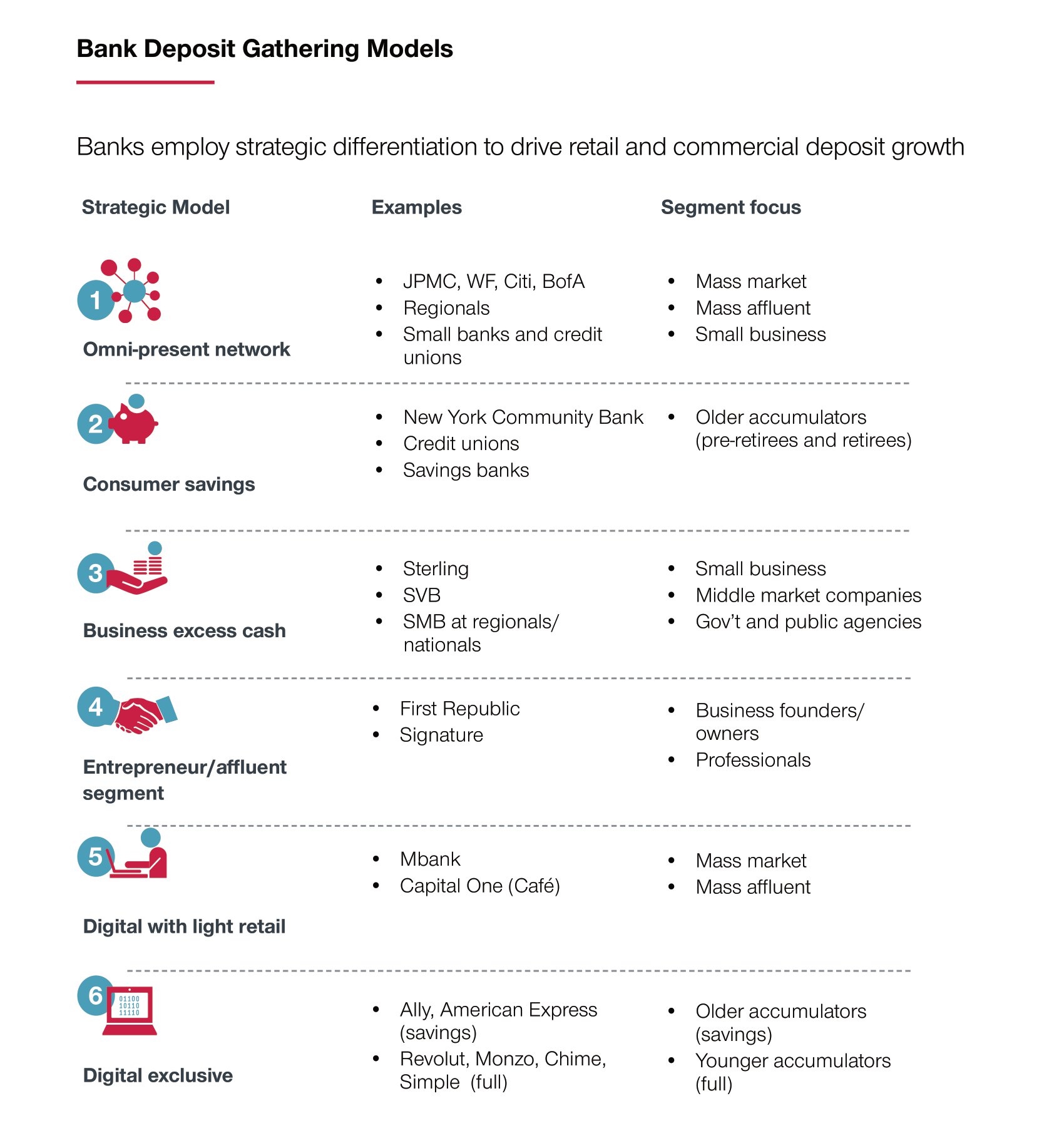

- An effective mix of strategic deposit-gathering models, with defined target segments and aligned business systems. In the current crisis, the most threatened banks are those relying on excess cash from businesses and or entrepreneurs and affluent depositors (chart 1). In retrospect, it’s clear these institutions either require extremely conservative balance sheets to offset their unique vulnerability to dramatic deposit outflows, or a more diversified mix of deposit-gathering models that reduce dependence on volatile deposits.

- Product line-up and innovation that encourages deposit stickiness and reduces deposit expense. The current bank run started with venture-backed companies with large deposits, modest operating needs, and simple deposit accounts. It’s much more difficult for a business to unhook a complex cash management account or for a household to move its checking account. The most forward-thinking banks and fintech firms have found ways to deeply integrate into the lives of their business and consumer customers by developing products to support performance improvement and financial health.

- Precision pricing that balances growth, expense and stability. Most banks have already invested in some type of analytic pricing capability. The current turmoil shows that the need to measure and attach a value to stability has been a lower priority. For example, few institutions have a flow-of-funds model that tracks and projects balance inflows and outflows at the product and customer-level and distinguishes between cross-product and cross-institution migration.

- Marketing and distribution that can build relationships. It is unlikely that relationship power can offset a full-scale bank run and it did not save SVB. But it is clear that full-scale relationships with multiple product ties to a customer are more valuable. Relationship customers accumulate higher balances, stick around longer and drive growth through referrals. Marketing budgets, legacy distribution networks and digital channels all need to be focused on relationship building.

Chart 1

Banks are inherently fragile and vulnerable to a bank run. In their Diamond-Dybvig model, economists Douglas W. Diamond and Philip H. Dybvig show that the bank's role as an intermediary between savers who prefer liquid deposits that can be withdrawn at any time, and borrowers who prefer illiquid assets like mortgage or long-maturity loans, means banks have fragile capital structures, subject to bank runs.

Banks need the full confidence of their customers on the underlying soundness and financial strength of the organization to succeed.