Many bankers are uncertain how to respond to the explosion of merchant and consumer demand for BNPL. In this article, we share insights from a recent study, and offer a thoughtful approach, taking into account: risk, borrower behaviors, interest rate sensitivities, profitability, and the value of financing in the shopping experience.

Shoppers and merchants alike have much to love about Buy Now, Pay Later (BNPL) arrangements. For shoppers, they are easy to get and understand. For merchants, they can increase sales and provide valuable consumer data.

Bankers, on the other hand, have a lot to be concerned about when it comes to these unsecured, merchant-subsidized installment loans. Especially, as they are usually offered free of interest rate charges or fees to shoppers at the point of sale.

Bankers worry that most consumers are approved for these short term loans within seconds, with only a soft credit check. According to bankers, many shoppers don't qualify for credit cards. Consumers can be tempted to splurge and overextend themselves on apparel, electronics, vacations, and other consumer goods. They wonder what could happen during a downturn and BNPL borrowers miss payments en masse?

However, bankers who sit on the sidelines waiting for upstart BNPL lenders to crack open from having assumed too much risk, must recognize that a substantial percentage of BNPL users are experienced, low risk borrowers.

Why Banks cannot ignore the Value of BNPL

BNPL also threatens banks' credit card franchises. From the shopper's perspective, BNPL loans are free as long as they make the required payments and offer more financial flexibility than credit cards.

Merchants, too, see more value in BNPL. They are willing to pay lenders anywhere from 3 to 5 percent or more, in addition to transaction fees in some cases, to extend this type of financing as a payment option to their shoppers. These fees are higher compared to those associated with credit card purchases. Merchants pay them because they benefit from higher conversions at the point of checkout.

BNPL is already too big to ignore. Global BNPL revenues are expected to nearly double to 1.1 billion US dollars by 2025. Meanwhile, tech giants Amazon and Apple made BNPL mainstream when they partnered with Affirm to extend this financing option to their shoppers.

How should Bankers Respond to BNPL?

Understanding the BNPL Consumer

It is important to recognize that BNPL borrowers are not a homogenous group. There is a misperception that BNPL users have credit and liquidity challenges, or that this is a downmarket offering, when this is not always the case.

In July 2021, we conducted a survey of US households with more than $25,000 in annual income. In the survey we oversampled for households with more than $150,000 in annual income, which uncovered the following:

- A majority (66 percent) of respondents who use BNPL have good credit scores of 700 or above

- Most BNPL users (70 percent) are employed and are more likely to be high-income earners compared to non-BNPL users

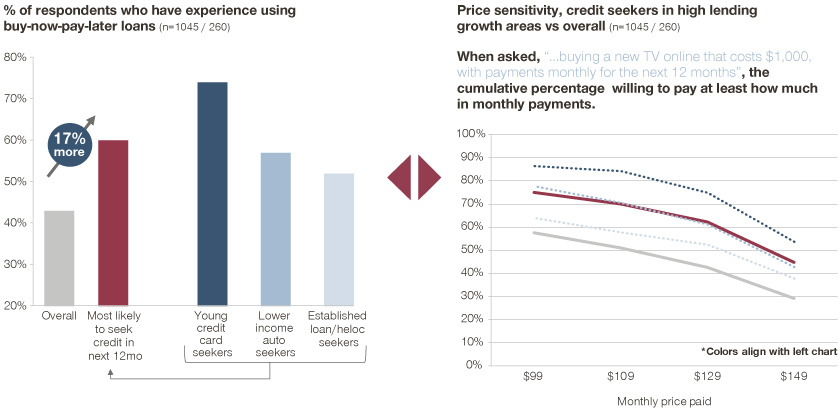

- BNPL users are 17 percent more likely to seek credit in the next 12 months compared to non BNPL users

- When evaluating a BNPL offer, a large portion of users are quite insensitive to interest rates: 58 percent of BNPL users are willing to pay the equivalent of 33 percent annual percentage rate (APR) interest on a purchase

What does this imply?

The Covid-19 pandemic has changed how people shop for loans. Instead of visiting a bank branch to take out a personal loan, younger consumers, in particular, would rather borrow at the point-of-sale. They are not doing this because they have no other choice. They are doing this because BNPL is fast, convenient, and gives them more flexibility and options.

Banks must also recognize BNPL users' different willingness to pay for interest rates. Our research found a high willingness to pay in some users. To accommodate different pricing sensitivities, banks should consider product variations.

For example, a bank can introduce choice to payment terms where a 4-payment option can be extended interest-free to attract price-sensitive consumers. Meanwhile, 6-payment and 10-payment options with interest rate charges or fees can be extended to less price sensitive customers. This way, banks are optimizing their BNPL portfolios and not leaving money on the table.

How to attract BNPL users? What's important and what's unimportant?

What are table stakes?(high priority overall, or high priority but unwilling to pay extra for it) |

|

What are differentiators?(where preferences differ from the general population) |

|

What is unimportant?(things that are low-med priority across questions asked) |

|

Value Creation and Merchant Partnerships

To properly commercialize BNPL, banks should adopt a value-based approach to pricing, packaging and product development.

For some merchants, point-of-sale installment financing can greatly impact conversions, ticket size, and purchasing behaviors. In our survey, more than 40 percent of BNPL users said they would pay $129 per month over 12 months for a $1,000 television. This signifies that shoppers become less price sensitive when offered the option to pay for goods and services in installments. RBC Capital Markets estimates offering a BNPL option increases retail conversion rates by 20 percent to 30 percent, and lifts the average ticket size between 30 percent and 50 percent.

Banks must take a data-driven approach to assess the economic value of their BNPL offerings to merchants. Instead of one-size-fits-all pricing across a diverse merchant customer base and haggling over percentage points, a better approach is an intelligent system of tradeoffs. This will help define a commercial strategy based on the merchants' business type, product mix, and other value parameters.

Buy now, pay later schemes can be highly effective when targeted properly

further validation is seen when looking at sub-segments of the market

Merchants are increasingly looking to lenders to help deliver an integrated shopping experience. Some merchants might be willing to pay a premium for additional services from the bank including affiliate marketing, pre-purchase awareness campaigns, and reward or cash back merchant loyalty programs. Through rapid testing and refining, banks can identify BNPL features and pricing preferences that matter more to certain merchant segments.

To differentiate themselves, banks can consider more competitive pricing and value sharing to offset the merchant's BNPL costs. They can also choose to partner with merchants to co-develop BNPL products.

Banks of all sizes can enter the BNPL space. Banks can leverage third-party technology platform providers, developers, and AI-enabled underwriting engines to deliver fast, accurate BNPL loan approvals.

Banks need Two Critical Elements to Succeed

The first is to develop a BNPL credit approval process that can underwrite purchases for a substantial majority of the merchant's customers. Merchants are unlikely to sign on with a bank that regularly rejects its customers' BNPL applications.

The second critical element is the ability to leverage strong merchant relationships, where the bank is already providing valuable payment processing, lending, cash management, and other business banking services, to access customers for these BNPL loans.

Reach out to our experts to find out more on how you can use BNPL’s to your advantage.