Bankers are frustrated with the return on digital sales investment as they are met with several key challenges in digital selling. We walk through the behavioral underpinnings of what makes a digital sales experience work and look at the impact of applying these insights in a real-world setting.

Imagine your bank spends a year or more developing a new product. Then you invest millions in a digital marketing campaign. And the results are frustrating. Enrollments and balances remain below target. Revenue and income are not keeping up with initial projections.

This scenario reflects a common complaint about digital sales. A recent Simon-Kucher & Partners survey of more than 350 bankers worldwide revealed that over half feel their digital sales investments have not met expectations. Even COVID-19 barriers to in-person transactions have not changed the picture. Our latest consumer research shows that many bank customers still prefer a branch within reach, regardless of how they actually transact, and are only willing to accept what they consider to be best-in-class digital experiences.

Using behavioral science to enhance banking sales processes

Simon-Kucher has been working with banks to ensure that digital sales investment generates real returns. We have found that digital actually heightens customer expectations and the difference between digital competence and mediocrity is a deep understanding of how customers process and respond to experiences and information. The ideal experience is frictionless: customers never encounter behavioral barriers and every touchpoint incorporates incentives and nudges to motivate progressively deeper engagement. In digital acquisition and onboarding, we have helped clients achieve three to fourfold improvements in product uptake by employing behavioral science to remove friction from the sales process.

We typically begin with a digital diagnostic to ensure that customer targeting, value proposition and pricing, and sales processes are aligned. That’s not always the case, but let’s say that a bank has already identified an attractive and addressable target customer and developed a relevant and differentiated value proposition with competitive price points. Then the challenge is to architect and build an effective digital sales process to take advantage of this strong foundation. So what could go wrong?

Three key challenges in digital selling

It turns out that digital selling requires a successful balancing act on three dimensions. The first is digital intelligence versus human intelligence. A digital system does an incredible job delivering consistency but it also has a much harder time showing empathetic understanding of what a customer really wants. That’s where a really good sales professional excels. However, delivering consistently great sales experiences across hundreds or thousands of sales people is difficult. The first challenge is building digital system that is both consistent and adaptable.

The second challenge is deciphering and addressing how people really make decisions. Digital systems can easily store, recall, and display almost any combination of facts, figures, and images we think will be necessary to help a customer decide which product to purchase. This would be perfect if we were only selling to other computers. But we are selling to humans who have two distinct decision-making approaches. What the behavioral scientist Daniel Kahneman, who won a Nobel Prize for his insights, called System One is instinctive, emotional, and fast. System Two is slower, deliberative, and logical. Our digital sales processes almost always lean toward System Two. The economist Richard Thaler won a Nobel Prize for showing that addressing System One can change the financial decisions people make. A classic example is that too many choices paralyze the customer. You had better rigorously control choice and address the concerns of System One if you want to sell more.

The third balancing act is between people and situations. Let’s say you have a customer who perfectly fits your target – the right education and income level, age, and saving and investing habits. If you encounter that customer just after they have suffered a large investment loss, they might have an entirely different attitude toward risk than the same customer who has just benefited from a large investment gain. The digital sales process should weigh both the needs of the customer and the circumstances under which they come to you.

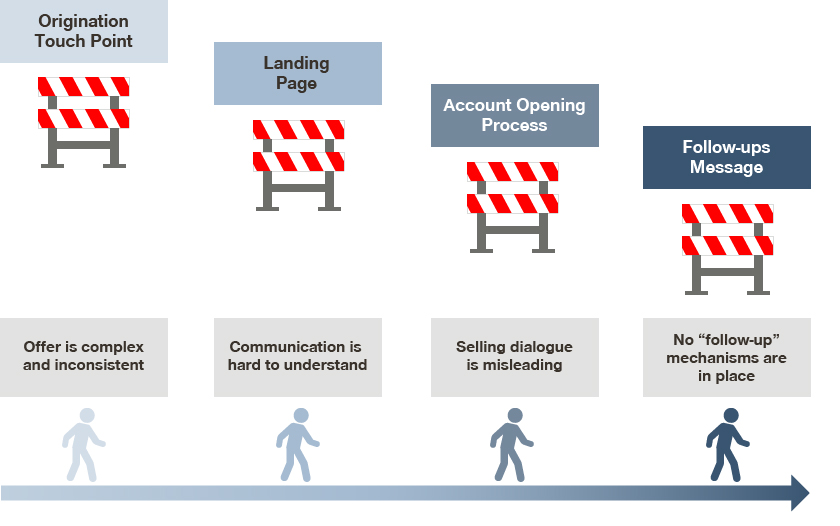

Evaluating the customer experience at every step

We have built a process to apply all of these principles to digital acquisition and onboarding, beginning with an audit that assesses your starting position and opportunities for improvement. We evaluate the customer experience at every step of the marketing and sales funnel, from initial encounter to application or enrollment to post-sales engagement, for the potential to remove sources of friction – anything that would distract, slow down, or disengage a customer along the sales journey.

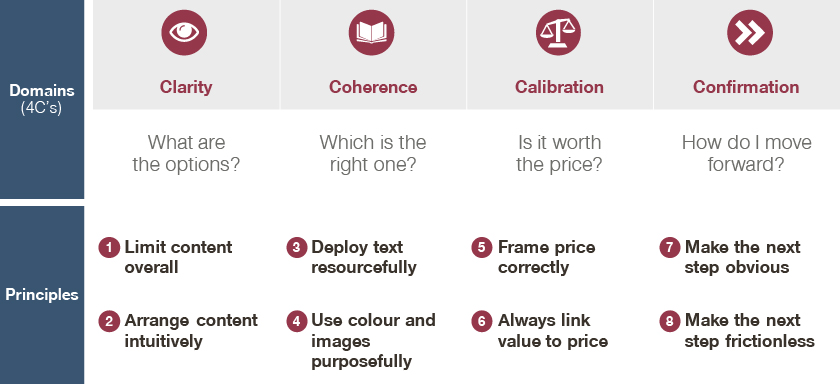

We use a framework called the 4Cs because each step needs to pass these tests in order to propel the customer forward:

- Clarity – does the digital experience clearly explain the choices to the customer through high-value content intuitively presented with minimum “noise”?

- Coherence – does the experience point the customer in the right direction through effective storytelling and purposefully aligned visuals?

- Calibration – does it demonstrate the value is worth the price, with supportive framing and judicious reference points?

- Confirmation – does it reinforce the customer’s decision to move forward, with a clear and easy next step?

We use the findings from this exercise to identify opportunities to deploy “behavioral nudges” that accelerate customer progress through the funnel. In a recent banking engagement, we were able to kick-start a previously sluggish acquisition campaign by focusing on three areas:

- Improving landing page effectiveness through visualization – converting numbers to pictures, framing (“we have it, they don’t”), simple interactive tools, and an action cue prompting a next step

- Eliminating “journey fatigue” in the account opening process with look-aheads, express lanes, and removal of unnecessary detours

- Redirecting potential drop-outs through encouragement and alternative paths

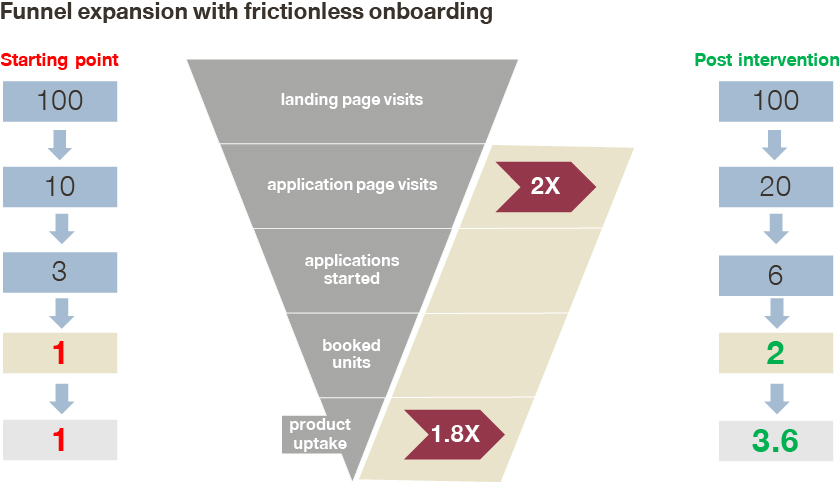

The payoff from this intervention was substantial. Application starts from the landing page doubled. The number of products sold per application start also doubled, yielding a fourfold total sales effectiveness improvement. Most importantly, the timeframe for the turnaround was measured in months, not years.

Successful digital acquisition supported by frictionless onboarding may seem like a banker’s dream, but it is achievable and within reach.