For a long time, loans for SMEs were hardly considered on banks' growth agendas. But this trend is shifting. Simon-Kucher's project experience shows that these loans can generate five to 10 percent in additional volume and revenue growth. What key requirements need to be met to achieve these results? Together with Swiss fintech company Teylor, we summarize what you should know when transforming your lending business model.

Small and medium-sized enterprises (SMEs) are the backbone of the European economy. The most important pillar of external financing for these companies is still a bank loan – provided companies resort to one, since around one-third of them currently rule out loan financing altogether. However, the reason for this is less about demand and more about the strict requirements in terms of collateral and disclosure, as well as the high level of bureaucracy involved in submitting applications.

For a long time, the SME segment wasn’t on banks’ radar as a growth market primarily due to lower profitability, smaller loan volumes per customer combined with relatively high (unit) costs, such as complex onboarding processes, and more difficult credit decisions.

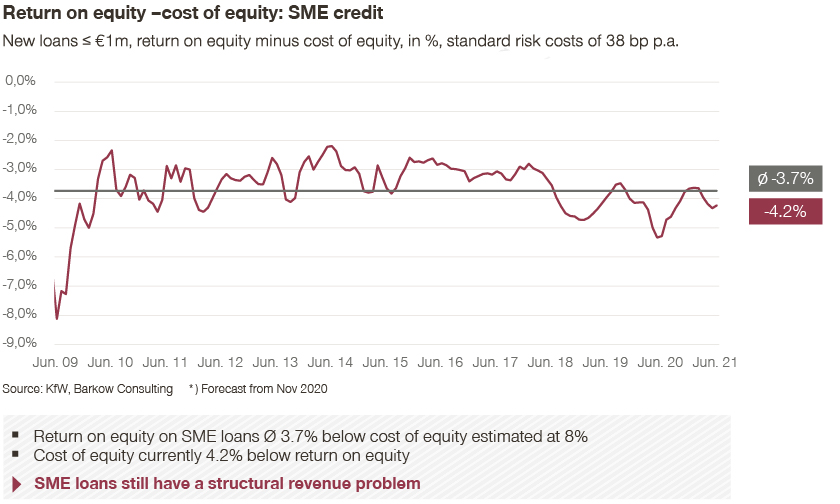

According to a study by Teylor, a Swiss financial technology company, the return on equity of SME loans has averaged 3.7 percent below the cost of equity. Over the past 13 years, the latter has been estimated at 8 percent. As a result, SME loans are only economically attractive to financial institutions if upselling potential for other financial services can be realized by granting loans.

New market players and technologies are currently causing the industry to reassess. In addition to banks, financing is increasingly appearing in the product portfolio of dealers, manufacturers, Neobanks, and digital platforms. Innovative market players are cleverly positioning themselves in the platform economy and using intelligent data analyses and automated credit processes to operate in a segment-specific and cost-saving way. In growth markets, such as India and Kenya, this development is already much more advanced.

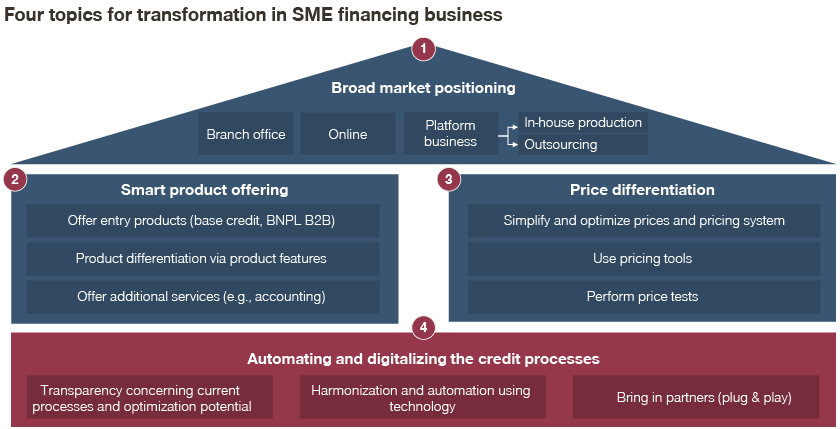

Many traditional lenders sometimes find it difficult to keep up with this dynamic of change. However, in our project experience, making specific adjustments can unlock volume opportunities and achieve revenue growth of five to 10 percent. For the necessary transformation of the lending business model, we recommend considering the following four topics:

1) Broad market positioning and benefits of the platform economy

In addition to the channel mix (branch, company’s own online channels, and platform business), the extent to which loans are produced in-house or brokered to third parties should be planned out strategically.

The key questions companies should ask themselves include “Which customer segments do we want to include in our own loan book?” and “Which part of the loan portfolio do we prefer to outsource?” Platforms can play a key role in this issue and in connecting technological partners to optimize processes.

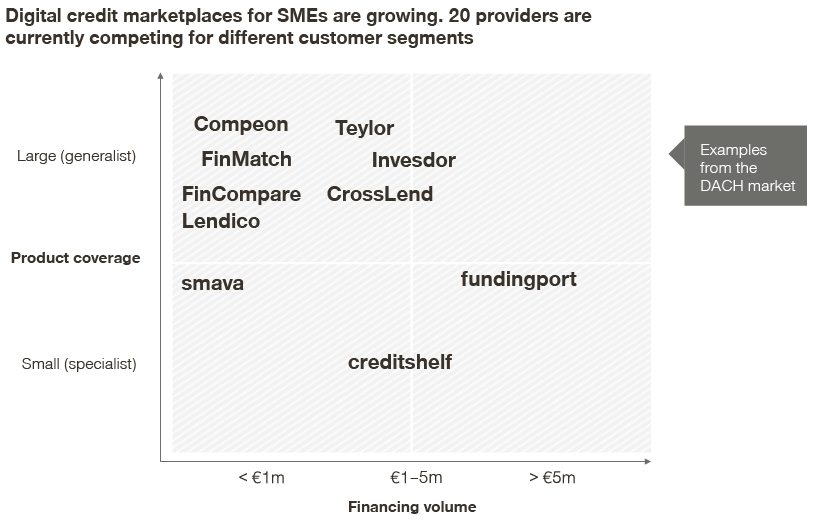

Intermediation via credit platforms has so far only taken place to a limited extent in the SME sector, with an estimated share of three to four percent of the credit volume. German providers such as Teylor, Compeon, Creditshelf, Lendico, FinMatch, and FinCompare are positioning themselves and showing significant growth.

In the next five years, the share of the credit volume could rise to over 10 percent – and as a result, billions could be brokered on platforms. Only those who position themselves broadly and diversify their product offering will be able to make the most of this growth trend and secure valuable market share.

However, there are barriers to entry. SMEs often cite personal contact with the bank advisor and a lack of trust as reasons for not using platforms. This is likely to change in the future. Mortgages are also a business that require a lot of trust and advice. More than one-third of the volume of mortgages are now brokered digitally. We therefore believe that platform logic will also become widespread in SME loans.

In such a dynamic market, there are three main strategic approaches banks can adopt:

- Banks can position themselves as end-to-end platform providers (E2E) to ensure full coverage of the value chain – from the customer front end to underwriting and additional integration of other providers – with the aim of building a digital ecosystem. The effort and high technical requirements here are offset by the desire for relatively independent positioning.

- They can also position themselves as product providers on existing platforms, even without direct customer contact. This potentially easier option enables access to new customer segments at a manageable technical and financial cost. Disadvantages include platform dependency and a lack of opportunities for long-term customer relationships.

- The intermediary positioning puts the focus on sales activity. One example is Interhyp, which was purchased by ING. The platform not only offers loans from ING but also keeps it open to competitors as a sales platform. An example in the SME lending segment is the comparison platform FinCompare, which was acquired by The German Cooperative Financial Group. In this case, the loan request starts at a bank and is checked and evaluated via a partner. A decision is then made as to whether the bank will finance the project itself or offer it via the platform.

2) Development of an intelligent product landscape

In SME financing, a fundamental distinction can be made between unsecured (overdraft facility, business loan) and secured (object financing) loans. In addition, there are alternative financing channels, such as factoring or leasing, which are often also offered by smaller specialized financial service providers.

In less complex unsecured forms of financing, positioning with smart entry-level products is particularly important. These include simple and fast basic loans and the topic of Buy Now Pay Later (BNPL) for B2B. BNPL already represents a major growth market in the B2C area, and its momentum is also increasing in B2B. Companies such as Billie (cooperation with Klarna), Mondu, and topi are already being noticed by investors, entering the market with high market capitalizations.

On top of a well-positioned basic offering, product differentiation via additional product features that can be offered as a bundle or package also play an important role.

Loans with extended flexibility and security options are used to target customers with corresponding needs. For example, flexible credit lines, fixed-interest periods/commitment fees, individual installment plan changes, and unscheduled repayments can be built into the price.

Further differentiation can also be achieved through services such as accounting, creditworthiness and liquidity optimization, taxes, and cybersecurity as well as through cooperation with other providers.

When differentiating their products, banks should always take channel positioning into account. For example, object financing, which requires more advisory services, is better placed in personal sales than via platforms with SME retail products.

3. Pricing optimization and use of intelligent pricing tools

While interest rates for new loans – especially due to increasing refinancing costs – are currently rising sharply again after years of decline, regular price adjustments and margin optimization are gaining importance.

Our project experience shows that many banks have little transparency over the impact of price adjustments. Prices are still adjusted manually in a time-consuming manner, and price tests are only carried out sporadically or not at all.

We typically recommend the following steps:

- Develop a pricing strategy as well as governance

- Conduct price tests to measure price elasticities

- Simplify the pricing system and optimize price levels specifically to each segment

- Use pricing tools for analysis and simulation of price adjustments

A current benchmarking of unsecured loans for volumes smaller than one million euros shows that the price spread for comparable credit ratings on the market is greater than three percent. However, part of this price spread is due to the scope of services and general conditions, such as the speed of credit decisions. This differentiation potential should be used, and pricing processes should be simplified and automated as much as possible.

4. Automating and digitalizing credit processes

In order to reduce costs and speed up processing, processes should be fully transparent and harmonized with each other, and manual activities involved in the processes should be reduced. This can be done either internally or by bringing in partners (e.g., fintechs).

Innovative technologies such as automatic document analysis, credit score appraisals via account access/XS2A, and automated credit decisions can be connected to the processes via an interface so they can be put to quick use (plug & play). For this to be feasible, an open system infrastructure and transparency concerning the current processes are essential.

When it comes to digitalizing credit processes, banks and other financial institutions are faced with two main challenges: The first is managing the technical, economic, and regulatory risks that digitalizing existing systems bring. The second is minimizing the disadvantages posed by both the lengthy process of developing internal digital expertise and relying on external providers in the meantime.

To effectively tackle these challenges, the practical solution is a modular approach. This involves financial institutions implementing software modules so they can digitalize their individual processes or customer journeys, often independently of each other.

For example, a digital business loan application process can be integrated into existing application processes without having to change or disrupt existing IT systems or establish new data silos. Because the financial institution’s existing systems will continue to be used alongside the digital modules, the economic and technical risks of digitalization are minimal.

Implementing technology-agnostic modules also means that the bank’s employees can maintain the system and make adjustments themselves when necessary. This eliminates, or at least reduces, the bank’s reliance on third-party providers.

Example Teylor: From simple applications to whole divisions – Digitalization as a game changer

The company Teylor implemented a digital onboarding and customer relationship management (CRM) module from a leading factoring provider in the DACH region (Germany, Austria, and Switzerland).

Before the module was implemented, corporate customers had to submit written or electronic applications, and the CRM was largely maintained manually. Because the processes weren’t automated, customers had to contend with long waiting times, while the manual maintenance of the system increased the risk of human error during data processing.

Teylor therefore decided to carry out a complete end-to-end digitalization of the onboarding and CRM process. Customers can now submit a digital application on the provider’s website in about 10 minutes. What’s more, they can complete all the application processes in the online form, from submitting the initial application and generating a quote to verifying their identity with video and adding a digital signature. All the data is then fed into the digital and largely automated CRM system.

Teylor’s workflow manager ensures that the separate onboarding and CRM modules interact seamlessly with each other as well as the factoring provider’s existing systems. Because the process is available as a white-label product, the provider’s branding remains unchanged.

By digitalizing the application journey, the loan process, from submitting the application to receiving the payment, was reduced from a total of six to eight weeks to less than two working days on average. Depending on the complexity of the application, the process might take several days or might be finished in just a few hours.

The factoring provider was also able to reduce the cost of the onboarding process and continuous customer management by 50 percent. A reduced error rate and the digital application format have also improved the customer experience.

Moreover, Teylor completely digitalized a separate loans division for one of its customers. The customer, a German bank, offers various financing solutions and has a separate division dedicated to handling agricultural and other finances.

Teylor managed to digitalize all this division’s loan processes, ranging from the application journey and CRM to risk assessments and loan portfolio management. Because Teylor customizes the modules to meet the customer’s requirements, they were able to account for the specific features of agricultural financing. For example, the digital application journey includes parameters for land area and livestock, which are then incorporated into the risk assessment and quote generation process.

The bank’s sales employees can now submit a loan application, present a quote to the customer, and get an immediate digital signature all in a single customer meeting using digital devices. This makes the process easier to scale up and is much more cost effective. By Teylor’s estimate, the bank achieved a positive return on investment within the first few months.

Conclusion: More growth through positioning, pricing, and process optimization

Successfully restructuring your lending business model requires a broad market position. This includes credit platforms, assorting an intelligent range of products covering a wide price range, and implementing automated, digitalized credit processes.

We support customers both with developing a new business model and practically implementing the subsequent transition. We combine conceptual consultation expertise with technical implementation provided by our data and software specialists from Simon-Kucher Engine and Elevate.

Contributions from Teylor CEO & Founder Patrick Stäuble and Teylor Head of Marketing and Communications Lukas J. Hofer